Godfreys Group Ltd

GFYDetails

Improved sales and portfolio rebalance: For the first half financial year 2017, Godfreys Group Ltd (ASX: GFY) recorded sales of $92.4 million indicating an increase of 2.8% from the same period a year ago. In the same context, comparable stores sales dipped 7% while operating gross margins narrowed by 3.5 percentage points. Meanwhile, underlying EBITDA stood at $6.3 million as compared to $8.7 million in same period year-ago. Led by a $24 million non-cash impairment, GFY recorded a net loss after tax of $21.4 million.

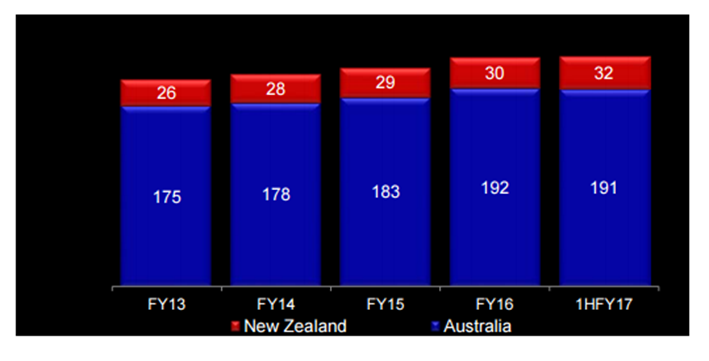

Retail Store Network (Source: Company Reports)

Along with the earnings announcement, Godfreys declared an unfranked dividend of 2.5 cents per share supported by strong cash flow from operations of $7 million. In October 2016, GFY strategized to move to a majority franchise model and has already converted four stores in the first half with a further 14 store conversions planned for the second half. GFY has maintained its FY17 underlying EBITDA at $14-$15m range. We rate GFY a "Speculative Buy" at the current price of $ 0.90

GFY Daily Chart (Source: Thomson Reuters)

Insurance Australia Group Ltd

IAG Details

Bringing stability in financials: Insurance Australia Group Ltd (ASX: IAG) reported a first half 2017 insurance profit of $571 million as compared to $610 million in the year-ago period. Driven by building an increasingly customer focused organisation, insurance margin stood at 13.5% compared to 14.9% earlier. For the first half, Gross written premium (GWP) came in marginally above expectations at $5.8 billion, a 4.7% increase from year-ago. This is mainly due to rate increases in order to counter higher claim costs in short tail personal lines in Australia and New Zealand, and improved commercial pricing.

.png)

GWP Growth and Insurance Margin (Source: Company Reports)

With a cash return on equity of 14.8%, the company maintained interim fully franked dividend of 13 cents per share. Looking ahead, IAG raised its FY17 GWP guidance to low single-digit growth, as compared to its previous relatively flat growth prediction. The stock has gained almost 8.5% in the past three months (as of February 24, 2017). We maintain our “HOLD" recommendation at the current share price of $ 6.04

.png)

IAG Daily Chart (Source: Thomson Reuters)

Amaysim Australia Ltd

.JPG)

AYS Details

Solid result but decline in ARPU: Amaysim Australia Ltd.’s (ASX: AYS) stock slipped 3.2% post the company released its half year results that entailed a 564% growth in statutory EBITDA while underlying EBITDA surged 38% driven by growth in mobile and disciplined cost management. There has been 34% 1H17 mobile subscriber growth over prior corresponding period (pcp) closing subscribers of 1.03m. Revenues from ordinary activities rose 16.5% on pcp to $136.6 million. However, this solid result was impacted by the 15.1% slip in average revenue per user (ARPU) to $22.37, owing to initiatives to grow subscribers and reduce churn. On the other hand, the management expects ARPU to stabilise at current levels in the second-half and grow gradually thereafter.

.png)

Broadband Investment to drive earnings (Source: Company Reports)

AYS also intends to launch the broadband in next 90 days. The company has also declared for 2017 interim dividend per share of 4.0 cents, which is up 33% over pcp and represents a dividend payout ratio of 72%. We give a “Buy” recommendation at the current price of $ 1.79

.png)

AYS Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...