Fortescue Metals Group Ltd

.png)

FMG Dividend Details

Cost Control efforts to offset pricing pressure: Fortescue Metals Group Limited (ASX: FMG) recently launched USD 750 million debt repayment offer for 2019 at 8.25% and 2022 at 6.875% Senior Unsecured Notes through a tender. The company lately updated about completion of the offer as well. With this offer, FMG intends to further decrease its interest costs and reach its initial gearing target of 40%.

.png)

USD 750 million debt tender (Source: Company Reports)

Moreover, the group is also lowering its production costs from seven consecutive quarters to September 2015 quarter. Accordingly, the group was able to deliver solid operating cash flows during the quarter and hence repurchased over USD 384 million of debt on market (for an average price of 80 cents in the dollar getting a pre-tax gain of $68 million) and even enhanced its cash balances to US$2.6 billion. FMG reported that its shipments reached 41.9mt with cash production costs (C1) of US$16.90 per wet metric tonne during the September 2015 quarter. The group achieved a price realization of 91% to US$50/dmt against the average 62% Platts price of US$55/dmt. We also note that BC Iron Ltd announced about the exploration results for Mulla 2 and Mulla 3 (JV with FMG) confirming the presence of iron mineralization with good continuity. The completion of sale of Cheritons find project by Riedel Resources for $700,000 in cash may help it decipher its position to contribute to future JV funding for the Charteris Creek project, which is a JV with FMG’s subsidiary (FMG Resources Pty Ltd).

.png)

Cost enhancements (Source: Company Reports)

Stock Outlook: Fortescue Metals Group stock plunged by 36.22% during this year to date (as of December 08, 2015) impacted by the volatile commodity prices. On the other hand, Fortescue Metals gave a better guidance of 165mt shipments and C1 cost of US$18/wmt during fiscal year of 2016. The group targets to achieve a production cost of US$15/wmt at an exchange rate of 0.72 by FY16.

FMG estimates a sustainable capex of US$330 million or US$2/wmt excluding vessel funding during FY16. Meanwhile, FMG’s Iron Bridge Stage 1 plant trials are ongoing with prospect developments subject to effective finishing of Stage 1 and joint venture approval. FMG’s efforts in reducing costs, maintaining production throughput and reducing debt seem commendable which will help deal with lower prices on earnings. Given the above, we recommend a HOLD for the stock at the current price of $1.82

FMG Daily Chart (Source: Thomson Reuters)

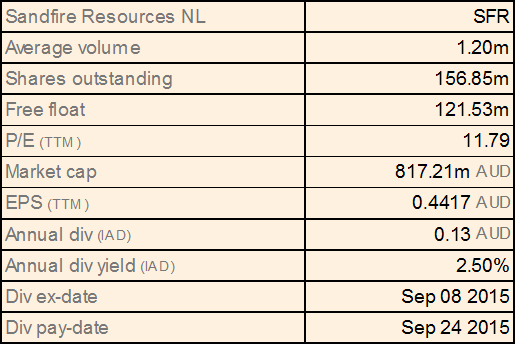

Sandfire Resources NL

SFR Dividend Details

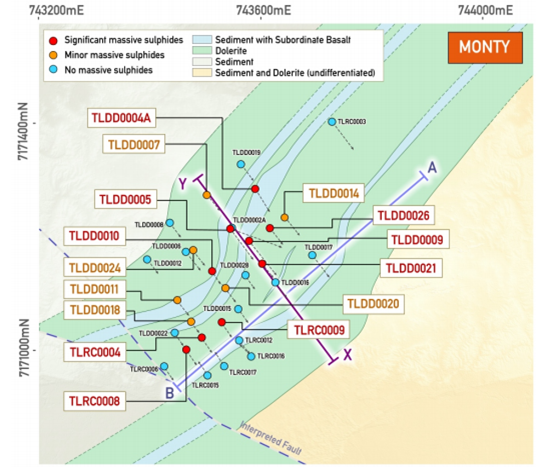

Ongoing performance pressure: Sandfire Resources NL (ASX: SFR) stock delivered returns of about 12.04% during this year to date (as at December 08, 2015). The group reported positive results from its continuous drilling efforts at the Monty copper-gold discovery at DeGrussa Copper-Gold Mine on the Springfield Project, which is a part of its farm-in with Talisman Mining.

Production Overview (Source: Company Reports)

The group would continue to test host horizons along Monty while the Drill sites would start the initial phase of drilling at Homer prospect in December quarter of 2015. On the other hand, the group’s Copper production decreased to 16,638 tonnes during September Quarter as compared to 18,637 tonnes in June quarter while the average ore grade also declined to 4.7% Cu from 5.05% Cu in earlier quarter.

Monty prospects (Source: Company Reports)

The group also decreased its gold production to 7,885 oz during the September quarter. Moreover, SFR reported a mechanical failure of the drill rig at Coppermine Creek. To refurbish thickener tanks and the concentrate filter, the group shut operations for eight days in September. Recently, SFR has increased its stake in Tintina Resources to 57% from 36%. The company also announced the update with regards to its DeGrussa solar project with commencement of the installation of the first photovoltaic solar panels underway and site construction activities advancing well as per the Q1 CY2016 completion target. SFR stock corrected over 13.17% in the last four weeks (as at December 08, 2015).

We believe that the group’s performance would continue to get impacted by the lower production and ongoing commodity prices volatility. We give an “Expensive” recommendation on the stock at the current price, and would review the stock at a later date.

SFR Daily Chart (Source: Thomson Reuters)

Dick Smith Holdings Ltd

.png)

DSH Dividend Details

1Q16 trading update and significant downgrade to FY16 profit: Dick Smith Holdings Ltd (ASX: DSH) plunged about 84.05% this year to date and about 19.28% in the last five days (as at December 08, 2015). Bitten by the recent price crash at the back of a weak trading update with the disappointing October performance, DSH has initiated review of its inventory. Though updates for the same are most likely to be provided in February 2016 along with the half year results (or earlier, as appropriate), however, the company still aims to drive sales, maintain flexibility on gross margin to lower the inventory and better its net debt position.

Connected Home by DSH (Source: Company Reports)

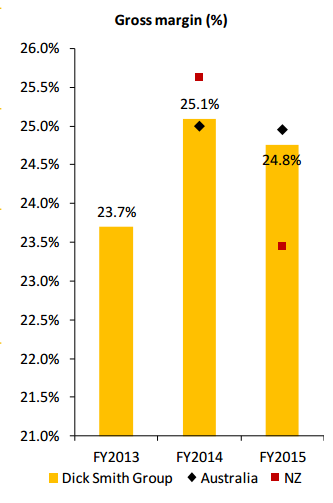

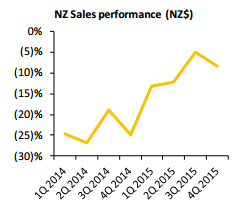

Further, DSH indicated that a non-cash impairment of $60 million (pre-tax) is required, and was not even hesitant in mentioning that it may require further impairment depending on the Christmas trading. As per the 1Q16 update, DSH reported robust sales growth with total sales up 6.9% and 1.3% like for like sales growth indicating an improvement over 4Q15. New Zealand depicted best quarterly growth. However, increased promotional activities coupled with unfavorable product mix led to lower margins.

Gross Margin (Source: Company Reports)

The company also mentioned about immense drop in trading in the month of October owing to the reduction in foot traffic impacted by some internal marketing decisions (such as cutting back on discounts on few brands). LFL sales plunged 5% in October with low margins attained. DSH is trying to bring changes in the way it operates in order to get the thrust back during the Christmas period. This particularly deals with efforts to enhance marketing and promotional activity for managing the like for like declines. At the same time, efforts on the inventory review may help manage cashflows. The company has announced about the downgrade in the FY16 NPAT which was said to be of the order of $5-8 million below the earlier guidance of $45-48 million. This does seem to be a point of concern as it draws attention to sustainability of the earnings reversal. However, DSH stated about stabilization of working capital in FY16. Further, Private label category is expected to drive penetration to more than 15% of sales by FY17. Omni-channel is also expected to drive 10% of sales online by FY17.

NZ Sales Performance (Source: Company Reports)

Efforts to combat the pressure: DSH has recently kicked off a 70% off everything clearance sale to manage inventory. Only time will tell whether this step from DSH will lead its competitors to follow the suit to safeguard their sales and market share, and eventually resulting in industry discounting during the Christmas time. The discount may boost consumer confidence but may also impact the profit margins across the industry.

Stock Performance: After the material drop in price on November 30, 2015, the stock surged 25% on December 01, 2015 and has been fluctuating with each passing day. DSH has been removed from the S&P/ASX 200 Index and S&P/ASX All Australian 200 Index as per the S&P Dow Jones Indices announced for the December 2015 quarterly rebalance. The stock is now trading at a very low P/E ratio of about 2x.

However, the dividend yield owing to the price crash seems abnormally high at the moment. Given the entire scenario, we believe that it would be better to wait and watch until more information is revealed about the FY16 profit. We therefore give a Hold recommendation for the stock at the current price.

.png)

DSH Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

AU

AU

Please wait processing your request...

Please wait processing your request...