Mirvac Group

MGR Details

Mirvac sells a 50% interest in 664 Collins street: Mirvac Group (ASX: MGR) entered into an agreement with an investment vehicle sponsored by Morgan Stanley Real Estate Investing (MSREI), for the sale of a 50% interest in its office development at 664 Collins Street in Melbourne. The total consideration for the 50% interest of the completed development is $138 million, based on a capitalization rate of 4.97%, and MSREI will fund 50% of the total development costs throughout the construction period, while Mirvac will provide development management, ongoing property and investment management services for the asset.

On track to achieve FY 17 targets: Mirvac Group reported a strong sales activity in the residential business during their third quarter driven by new project launches and continued sales at existing strongly performing projects. MGR is on track to achieve a Residential ROIC in FY17 of more than 15%, as compared to over 5% in FY13. Further, for the retail segment, the group reported that they are on track to achieve FY17 targets, that includes to increase sales productivity to $10,000/sqm, occupancy to >99%, Leasing spreads of >2% as well as an EBIT growth of more than 25% as compared to FY16. Moreover, MGR is well-placed to deliver a strong set of results in FY17, including operating earnings growth of 11 per cent and distribution growth of 5 per cent, which is at the top end of their previous guidance.

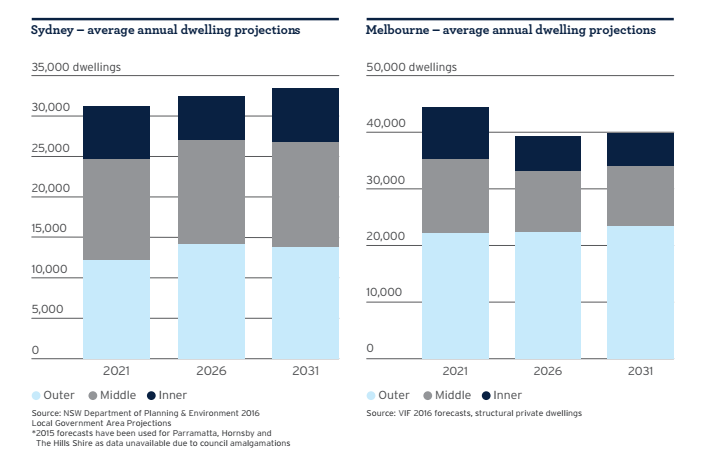

Building balanced portfolio: The group is expecting dwelling completions by 2031 boosted by outer and middle ring housing and accordingly positioning themselves to benefit from the growth of major cities. The group forecasts to deliver more than 15% growth in lot settlements in FY17 and projects 95% of Residential EBIT for FY17 as well as 65% for FY18. The group completed over 2,150 lot settlements to 30 April 17 and the default rate tracking is below 2%.

Market opportunity (Source: Company reports)

Stock performance: The group has solid embedded margins across MPC and a solid apartment pipeline with more than 50% of pipeline lots while maintaining more than 25% of the margins. MGR will be paying AUD 0.055 as dividend on August 31st, 2017. MGR stock has fallen 4.05% (Source: ASX) in the last three months as on July 3, 2017 placing them at a reasonable P/E. The stock has a strong dividend yield of 4.88%. Based on the foregoing, we give a “Hold” recommendation on the stock at the current price of $2.10

MGR Daily chart; Source: (Thomson Reuters)

Lendlease Group

.JPG)

LLC Details

Diverse international pipeline: Lendlease Group (ASX: LLC) is building a diverse portfolio across major countries. InAmericas, the group is having a $3.7 billion and a development pipeline and a Construction backlog revenue of $6.9billion. LLC has $0.1 billion of Investments in America. Some of the major current projects in Americas are Clippership Wharf, Boston; Riverline, Chicago; 281 Fifth Avenue, New York New projects/opportunities after half year of 2017. New projects in Americas are Van Ness, San Francisco; US Telco Infrastructure Portfolio. As per the Europe portfolio, the group built an $8.7 billion worth of Development pipeline and built a $1.1 billion of Construction backlog revenue. LLC has $1.4 billion Funds under management and $0.1billion worth of Investments. Major current projects in Europe are Elephant Park, London; International Quarter London; Deptford, London. New projects in Europe are Haringey, London; Milano Santa Giulia, Milan. With regards to Asia portfolio, the group has $5.7 billion worth of Development pipeline and has $0.9 billion of Construction backlog revenue. LLC has $5.4 billion of Funds under management and has $0.3 billion worth of Investments in the region. Major projects in Asia are Paya Lebar Quarter, Singapore; Tun Razak Exchange, Kuala Lumpur

.png)

International portfolio Source: Company reports)

Strong momentum in 2H17: Lendlease Group has planned to focus on establishing scale integrated model in each region. The group’s rising capital allocation across International Operations is expected to drive future international earnings growth as they have several urbanization projects in the last few years in target gateway cities – London, Milan, Chicago, New York, Boston, San Francisco, Kuala Lumpur and Singapore. The company continues to grow platform by using an enterprise wide approach across International Operations, risk management framework and the disciplined origination and execution excellence. Moreover, LLC is rebalancing towards Investments segment that includes new sectors, residential for rent, telco infrastructure. Additionally, LLC has reached the contractual close on Lifestyle Quarter at Tun Razak Exchange. LLC is entering into US Telco Infrastructure through the acquisition of telco tower portfolio. The company is the preferred bidder on Haringey urbanization project, London, which is over GBP2.0 billion development end value. The construction contracts awarded to LLC includes Design & construction of Javits Convention Centre, New York, ~USD1.5 billion (50% JV), Google Headquarters, London and the Australian Engineering Business appointed recommended contractor on three projects ~$500m. LLC stock has risen 14.04% (source: ASX) in the last six months as on July 3, 2017 and we believe this positive momentum in the stock would continue in the coming months. The stock has a dividend yield of 3.78% and is trading at a reasonable P/E. We give a “Hold” recommendation on the stock at the current price of $16.27

.png)

Development: Project summary, International Operations (source: Company Reports)

LLC Daily chart; Source: (Thomson Reuters)

Stockland Corporation Ltd

.JPG)

SGP Details

Positive outlook: Stockland Corporation Ltd (ASX: SGP) had announced that Andrew Stevens would join the Stockland Board from 1st July 2017. On the other side, SGP has maintained FY17 guidance for growth in Funds from Operations (FFO) per security of 6-7%, assuming no material change in market conditions. The company remains on track to achieve FY17 Distribution per Security (DPS) of 25.5 cents, based on the higher of Total Trust Income (TTI) or 75 – 85% of FFO, up 4.1% on FY16. SGP’s Residential business has achieved 1,891 net deposits in the third quarter and 5,984 net deposits in the financial year to date, as compared to a total of 4,844 net deposits up to the corresponding point in time last year. SGP’s Residential business is on track to meet its full year target of more than 6,000 settlements. Moreover, SGP has continued to invest in the portfolio as well as remixed the centers to deliver good growth of 2.7% in specialty sales per square meter across their comparable shopping Centre portfolio. Overall comparable annual sales across all retail categories lost over 0.2%. But, the group believes that they are on track to achieve Retail FFO growth in line with the guidance of 3 - 4% for the full year, driven primarily by specialty stores. Further, SGP’s Retirement Living business achieved 244 net reservations in the quarter. The result was in line with internal forecasts, which allowed for the timing of new development stage releases and the withholding of units at Oak Grange in Melbourne and Castle Ridge in Sydney, pending proposed redevelopment activities.

.png)

Five-year indicative asset mix (source: Company Reports)

Stock performance: SGP stock lost over 7% in the last three months (as on June 30th, 2017; Source: ASX) as the group’s third quarter of 2017 retail sales growth was relatively flat. Easter shifts from 3Q16 to fourth quarter of this year is one of the reason that impacted this. Moreover, Variable results from their Queensland centers, including disruption from Cyclone Debbie also hurt the retail portfolio. On the other hand, the Specialty sales productivity for comparable Centre retailers enhanced, with MAT/MLA1 rising by 2.7%, boosted by active remixing strategies. Moreover, the group’s retail developments are ongoing and in line with feasibilities. The group’s Green Hills, NSW, stage one opened April 2017, and is expected to finish by mid-2018. Bundaberg, Kensington, finished with new format Coles supermarket. The stock has a solid dividend yield of 5.82% and is trading at a reasonable P/E. We believe investors need to leverage the recent fall of the stock while we give a “hold” recommendation on the stock at the current price of $4.30

.jpg)

SGP Daily chart; Source: (Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...