Challenger Ltd

|

Challenger Ltd |

CGF:ASX |

|

Average volume |

3.06m |

|

Shares outstanding |

570.62m |

|

Free float |

544.13m |

|

P/E (TTM) |

16.66 |

|

Market cap |

4.70bn AUD |

|

EPS (TTM) |

0.494 AUD |

|

Annual div (IAD) |

0.30 AUD |

|

Annual div yield (IAD) |

3.65% |

|

Div ex-date |

Aug 31 2015 |

|

Div pay-date |

Sep 30 2015 |

CGF Dividend Details

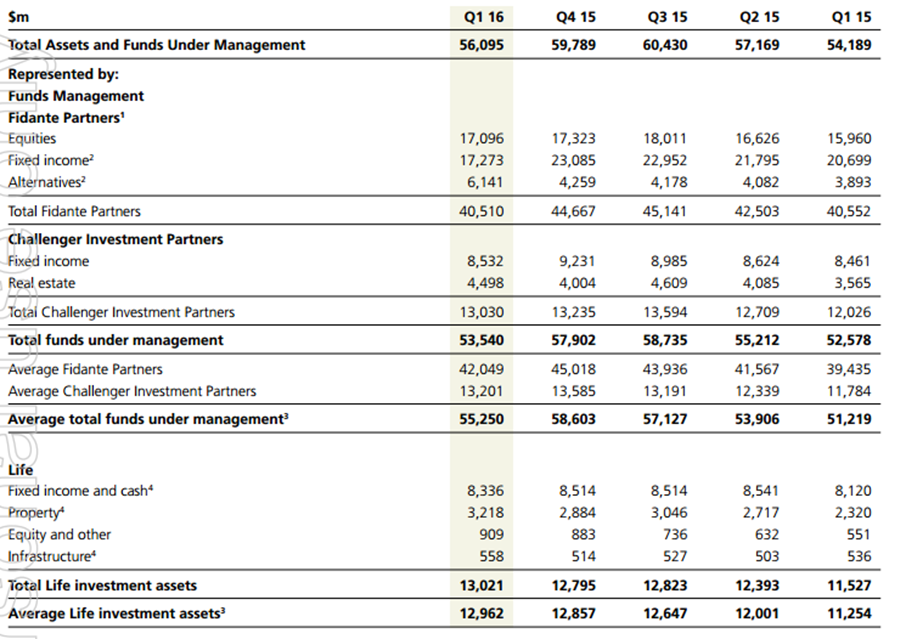

Positive regulatory reforms and rising ageing population to boost growth: Challenger Ltd (ASX: CGF) is well positioned to leverage the rising ageing population in Australia, with almost 700 people turning 65 every day. Moreover, the government (in response to the Financial System Inquiry) reported that they would enhance outcomes for retirees and the sustainability of Australia’s superannuation system, opening more opportunity to CGF. On the other hand, Challenger’s assets and funds under management decreased by 6% to $56.1 billion as at Sep 30, 2015, impacted by sale of Kapstream capital business and Dexion capital acquisition which offset solid organic flows to the group. However, the group’s total life annuity sales improved by 12% to $884 million during the first quarter of 2016 against prior corresponding period (pcp). Overall retail annuity sales rose 2% year on year (yoy) to $707 million. Life’s investment assets rose by $0.2 billion to $13 billion during the period driven by net book growth. The group also gave a life’s cash operating earnings guidance in the range of $585 million to $595 million in the fiscal year of 2016. CGF also reported about signing of new distribution agreements under its partnership with AAS, a major provider of superannuation administration services.

Assets and FUM highlights (Source: Company Reports)

The shares of Challenger delivered a year to date return of 25% (as of October 30, 2015) and rallied over 15.3% in the last four weeks alone driven by rising ageing populations and favorable regulatory reforms by government. Challenger is trading at a valuation with a P/E of 15x and has a decent dividend yield of 3.7%. Based on the foregoing, we give a “BUY” recommendation to the stock at the current price of $8.09

CGF Daily Chart (Source: Thomson Reuters)

FlexiGroup Limited

|

FlexiGroup Ltd |

FXL:ASX |

|

Average volume |

1.83m |

|

Shares outstanding |

372.34m |

|

Free float |

214.36m |

|

P/E (TTM) |

11.59 |

|

Market cap |

1.14bn AUD |

|

EPS (TTM) |

0.2641 AUD |

|

Annual div (IAD) |

0.173 AUD |

|

Annual div yield (IAD) |

5.66% |

|

Div ex-date |

Sep 09 2015 |

|

Div pay-date |

Oct 16 2015 |

FXL Dividend Details

Diversification efforts via acquisitions: FlexiGroup Limited (ASX: FXL) recently acquired Fisher & Paykel Finance, who is a provider of non-bank consumer credit in New Zealand having around 430,000 active card holders. As at June 30 2015, Fisher & Paykel Finance has receivables of NZ$662 million as well as has new business volumes of NZ$617 million. With this acquisition, FlexiGroup would be able to further diversify in Australia and New Zealand with the combined group comprising over $2 billion in receivables. The group would partly fund the acquisition via fully underwritten accelerated non renounceable entitlement offer worth of $150 million.

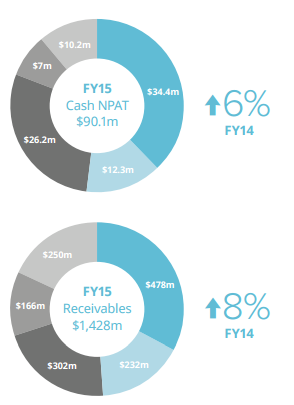

Cash NPAT and Receivables (Source: Company Reports)

Latest updates include signing of a five year agreement between Rent.com.au limited (rental property web portal) and Certegy Ezi-Pay Pty Ltd (division of FXL) that extends the relationship between the two companies indicating a strong outlook for the commercial potential of Rent’s RentBond product to the Australian rental market. Meanwhile, FlexiGroup reported a Cash NPAT growth of 6% yoy to $90.1 million in fiscal year of 2015 while the Statutory NPAT surged by 44% yoy to $82.7 million. The group’s net promoter score of +14 coupled with recurring business value across its businesses indicates its customer focus of technology improvements. FlexiGroup’s Telecom Rentals acquisition has expanded its penetration as well as helped in becoming a leading technology leasing business in New Zealand. NZ receivables contribution rose to 11.6% from 5% during the period, offering a solid scale to its present high-growth New Zealand business. The group also reiterated its Cash NPAT guidance range of $92 million to $94 million (excluding Fisher & Paykel Finance acquisition) during FY16. The shares of FlexiGroup surged over 33.57% (as of October 30, 2015) in the last four weeks alone partly driven by acquisition and decent FY15 results. But the stock is still trading at cheaper valuations with a P/E of 11.3x and has a dividend yield of 5.8%. We remain bullish on the stock and reiterate our “BUY” recommendation on the stock at the current price of $2.85

FXL Daily Chart (Source: Thomson Reuters)

IMF Bentham Ltd

|

IMF Bentham Ltd |

IMF:ASX |

|

Average volume |

717.80k |

|

Shares outstanding |

169.46m |

|

Free float |

152.71m |

|

P/E (TTM) |

37.71 |

|

Market cap |

244.02m AUD |

|

EPS (TTM) |

0.0382 AUD |

|

Annual div (IAD) |

0.10 AUD |

|

Annual div yield (IAD) |

6.94% |

|

Div ex-date |

Sep 23 2015 |

|

Div pay-date |

Oct 09 2015 |

IMF Dividend Details

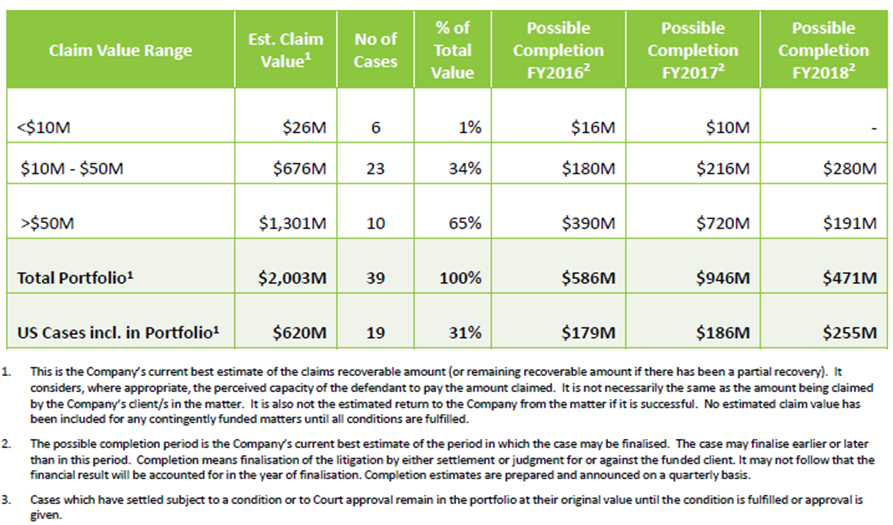

Solid outlook, International expansion: IMF Bentham Ltd (ASX: IMF) net income from cases fell by 42% yoy to $14.6 million in fiscal year of 2015, due to four losses, namely, Bank Fees case in Australia (impact of $5.5 million), the National Potato case in South Africa (impact of $8.4 million), Desalination case in Australia (impact of $0.7 million) and a loss in the US (impact of $1.0 million). However, investors need to note that IMF has only lost 10 cases since listing in 2001 which is just 6% of 175 cases. IMF Bentham’s witnessed a strong growth in US cases, which increased to 31% of the investment portfolio from starting of 2011. The group delivered a strong growth in US cases, which increased to 31% of the investment portfolio from starting of 2011. IMF intends to leverage the rapidly changing third party litigation funding in both the US and the UK/Netherlands over the past five years and has also been accepted as a funding alternative in these countries. Funding three cases in Hong Kong would drive potential growth in Asia. Meanwhile, the group is constantly enhancing investment portfolio which is above $2 billion of the claim size. IMF would undertake funding of more new cases and estimates over 37 new cases in fiscal year of 2016 with committed funds of $86 million. The firm expects 61 new cases with committed funds of $123 million in FY18. Shares of IMF surged over 8.27% in the last four weeks alone (as of October 30, 2015) and we continue to be bullish on the stock. IMF also has a solid dividend yield of over 6.9%. We remain bullish on the stock and re-iterate our “BUY” recommendation at the current price of $1.45.

Claim value range and completion targets (Source: Company Reports)

IMF Daily Chart (Source: Thomson Reuters)

AU

AU

Please wait processing your request...

Please wait processing your request...