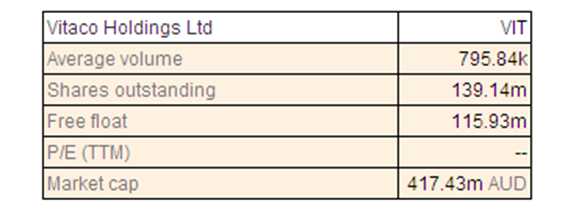

Vitaco Holdings Ltd

VIT Details

Solid growth potential: Vitaco Holdings Ltd (ASX: VIT) stock listed on September 17

th, delivered over 21.01% since than till date (as of November 18, 2015). The group raised over $231.6 million worth of capital via a totally underwritten initial public offering priced at $2.10. The group distributed its product portfolio under two main divisions. Vitamins and Supplements and Sports and Active Nutrition is segmented as one division which comprises brands like Nutra-Life, Healtheries and Wagner. Health Foods is segmented as another division which consists of brands like Abundant Earth, Aussie Bodies, Balance, Bodytrim, Musashi and Healtheries. Vitaco Holdings built a solid base in Australia and New Zealand markets with major clients like Coles, Woolworths, Chemist Warehouse and Progressive Enterprises and Foodstuffs. Vitaco reported a revenue growth of 8.6% during fiscal year of 2015 on a year over year basis while EBITDA improved by 9.1% yoy during the same period. Moreover, the group estimates a better growth ahead and accordingly anticipates its revenues to improve by 22.6% yoy to $211.3 million during the fiscal year of 2016, boosted by domestic markets business growth. VIT forecasts its EBITDA to grow by 15% yoy to $23.7 million in FY16. Meanwhile, Vitaco shares rallied over 7.06% in the last four weeks. The stock has the potential to become a player like Blackmores depending on its ability to penetrate the China and Brazil markets apart from contribution from its core Australia and New Zealand business. There is also a boost coming in from the growth close to about 10% in the vitamins and supplements category in Australia over the last five years. We believe that VIT stock has the potential to deliver outstanding performance in the coming months and accordingly, give a “BUY” recommendation on VIT at the current stock price of $2.85

VIT Daily Chart (Source: Thomson Reuters)

Blackmores Ltd

.png)

BKL Dividend Details

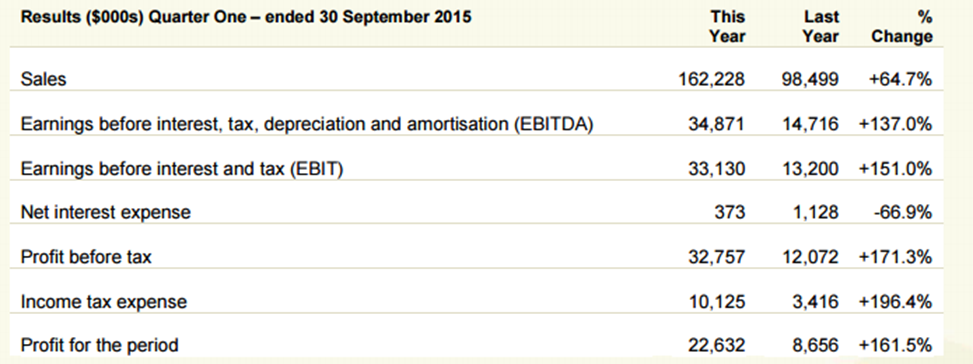

Solid first quarter performance driven by China contribution: Blackmores Limited (ASX: BKL) reported a solid first quarter of 2016 performance, with sales surging by 65% yoy to 162.2 million and net profit after tax increasing by 161% yoy to $22.6 million. The group’s revenues from Chinese consumers (via direct sales and Australian pharmacy partners) contributed over $55 million (estimations) during the first quarter which is over 34% of the overall BKL’s sales. Moreover, the overall Asia sales contributed over 50% of Group sales, reaching $80 million during the quarter. Meanwhile, BKL also delivered a decent organic sales growth of 18% yoy during the period. The group joined hands with Bega Cheese to develop and manufacture a range of nutritional foods like high quality infant formula. BKL also entered into a Joint venture arrangement with Kalbe sometime back to launch into Indonesia.

First quarter performance (Source: Company Reports)

Blackmores Limited delivered outstanding performance this year, by surging over 386.08% during this year to date (as of November 18, 2015) and delivered over 144.99% increase in the last six months. The stock continues to maintain its positive momentum and generated over 26.70% increase in the last four weeks. Blackmores would continue to derive contributions from Asia especially from China, while the group is also focusing on operational effectiveness. However, the stock is trading at a very high P/E of about 65x while the annual dividend yield is only about 1.19%. Accordingly, we give an “Expensive” recommendation at the current stock price of $174.77

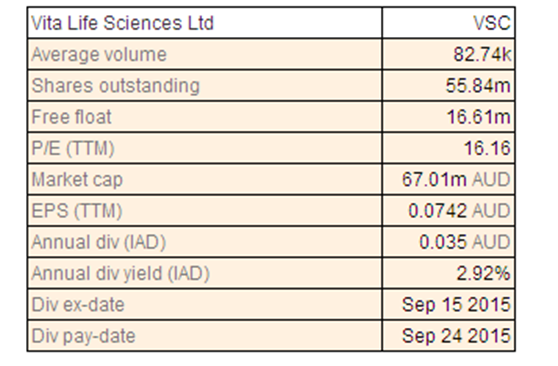

Vita Life Sciences Ltd

VSC Dividend Details

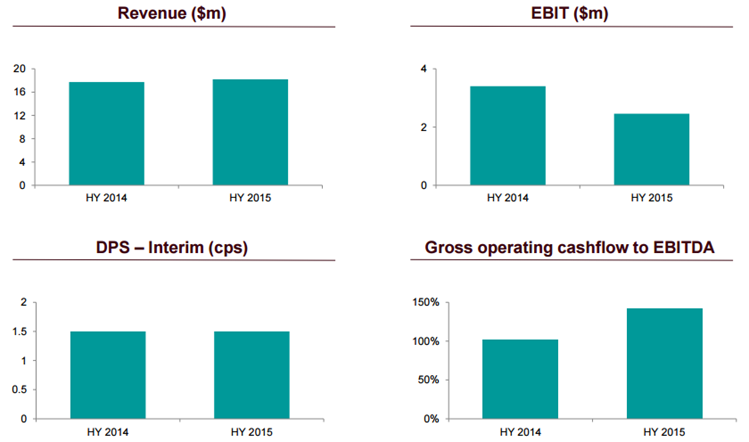

Growing Singapore and Australia contribution: Vita Life Sciences Limited (ASX: VSC) reported a revenue increase of 9.6% yoy to $7.2 million (against half year 2014) in Australia for fiscal year of 2015, driven by Herbs of Gold brand performance coupled with VitaScience brand rollout in pharmacy channels. Australia’s Operational EBIT enhanced by 17.4% yoy as Vita focused on high quality products and improved fixed cost base. Vita’s Singapore division delivered solid revenue surge of 22.2% yoy to $3.2 million as Herbs of Gold products were launched in Singaporean market, while the group also reorganized its staff to form a strong sales team. Vita estimates a sales of over $38 million for full year of 2015 and issued an EBIT guidance of around $5.5 million.

Vita Life Sciences performance (Source: Company Reports)

On the other hand, the group’s stock fell over 18.49% year to date (as of November 18, 2015) as VSC reported that its new businesses would be affected by product regulation in China, while Thailand business pressure is also ongoing. But, VSC is launching cross border ecommerce platforms in China which could open solid market opportunity to the group. Vita Life Sciences shares surged over 30.77% (as of November 18, 2015) in the last four weeks. VSC is trading at a P/E of about 16x.

Accordingly, we believe that the stock is overvalued at the current price.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

AU

AU

Please wait processing your request...

Please wait processing your request...