G8 Education

G8 Education Ltd (ASX: GEM) first quarter of 2015 revenues grew 66% on a year over year basis to $310.9 million driven by both organic as well as acquisitions growth. Twenty one new centers were added in the first half, with 17 centers in pipeline to be settled. After these settlements, G8 Education’s licensed places would reach 35,125 places in Australia. The company now has 457 centers in Australia and 18 centers in Singapore.

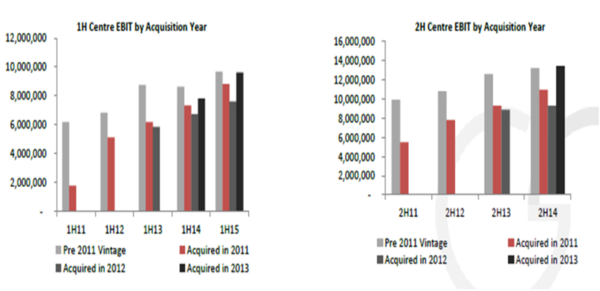

The group’s EBIT surged 93% yoy to $58.1 million during the period. The group witnessed an organic growth of 20.4% yoy coming from the acquisitions in 2011, while 2012 acquisitions contributed 12.9% to the 1H15 EBIT growth. Meanwhile, 2013 acquisitions generated an outstanding 23% growth for the 1H15 EBIT increase. The group’s overall NPAT rose 73% yoy to $28.2 million, while the Basic earnings per share increased to 7.84 cents in 1H15, from 5.21 cents in 1H14. G8 Education also declared a fully franked annual dividend of 24 cents, paid every quarter.

EBIT growth for the period coming from acquisitions (Source: Company Reports)

G8 Education’s stock had been under pressure since it touched its all-time high levels in the September 2014. The shares delivered a negative year to date returns of 25.4% and fell over 35% in the last one year. Investors have been worrying on the firm’s funding capacity for its further acquisitions while maintaining such attractive dividends.

Moreover, the group’s continues efforts to acquire Affinity Education wherein the Affinity Education management commented GEM as “opportunistic”, has also raised concerns on the group’s heavy reliance on acquisitions to generate growth. Recently, G8 Education again made an offer to Affinity Education. The group proposed one G8 Education share for every 4.25 Affinity shares, which results Affinity Education valuation 80 cents (increasing from its earlier offer 70 cents). Meanwhile, the Affinity Education management did not take any decision yet, with the offer open till September 28, 2015.

On the other hand, we view the sharp sell-off in the stock to offer a buying opportunity to investors, as the government’s federal budget allotted around $3.5 billion to childcare to improve the overall sector’s access and reach, and is indirectly encouraging parents to work. As a result, the growing number of children might also increase the group’s price per child revenue in future and subsequently the top line, if more parents go to work. G8 Education is also improving its synergies through acquisitions, which is evident in this half year’s EBIT growth. With a strong dividend yield of 7.35% and the stock rising over 3.3% in the last four weeks , we estimate that the stock has potential to reach higher levels, from the current price of $3.14.

Slater & Gordon

Slater & Gordon Limited (ASX: SGH) stock plunged around 45% in the last three months, as Australian regulators launched an investigation on the group’s errors in financial reporting. Also, rumors have been swirling on the company’s aggressive accounting practices and probable manipulation of its share prices by hedge funds. British regulators have also started investigating its $1.3 billion professional services division acquisition from Quindell, further hurting the sentiment.

On the other hand, Slater & Gordon is making all efforts to clarify the concerns surrounding the company. The group recently clarified that Ernst and Young assisted SGH during professional services division acquisition and confirmed that it is not subject to any ASIC examination for its accounting practices. Quindell also appointed PWC to review its accounting policies during December 2014, and its financial statements for 2013 and 2014 were audited by KPMG. PWC reported that Quindell’s accounting practices used for recognizing revenues and deferring costs related to acquisitions of its product areas were under acceptable practices, despite being on the aggressive side.

Investors should also note that Slater & Gordon’s first half of 2015 performance is quite strong with revenues growing 37.6% yoy to $245.3 million, and normalized EBITDA margin improving to 23.9% in 1H15, against 23.1% in 1H14. Accordingly, the group’s normalized net profit after tax rose 46.5% to $35.9 million versus $24.5 million in first half of 2014, and the basic earnings per share improved by 42.3% yoy to 17.5 cents. The group’s Australia division’s revenue rose by 9.2% to $127.7 million, driven by personal injury law segment’s improvement in Victoria. UK division’s revenues soared 91.5% yoy to $117.6 million, contributed by the Walker Smith Way and Leo Abse & Cohen acquisitions.

Slater & Gordon’s also completed its integration of its Walker Smith Way acquisition, a Consumer law focused on personal injury firm in North Wales and North West England in April 2015, which is expected to contribute an annual revenue of over £10.3m. Leo Abse & Cohen acquisition is estimated to deliver an annual revenue of £8.4m, as well as improve the company’s UK practice into specialist in hearing loss claims.

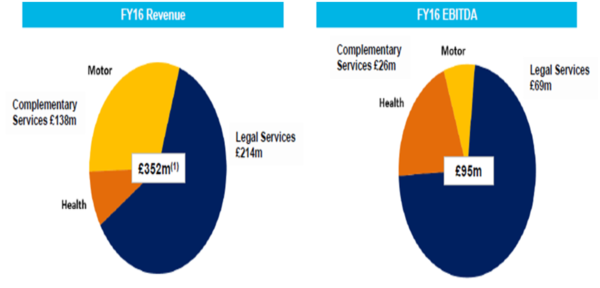

Slater & Gordon outlook (Source: Company Reports)

Meanwhile, the group forecasts a revenue of $520 million during the fiscal year of 2015 boosted by organic growth, with Normalized EBITDA margin to be in the range of 23% to 24%. The Cash flow from operations as a % NPAT is estimated to be more than 70%. Quindell’s professional services division (PSD) is also estimated to generate an EBITDA of £95 million during the fiscal year 2016. Having such a solid outlook, we believe SGH has the capabilities to fight back its recent allegations. With the stock trading at an attractive P/E of 10.3x, Investors need to view the recent sharp selloff as a buying opportunity and consider adding SGH in their portfolio at the current price of $3.20.

Ozforex Group

Ozforex Group Ltd (ASX: OFX) shares surged 12.12% in just last five days, as the group delivered better than expected results and even introduced a three year accelerate strategy to boost its growth going forward. The group wants to double its revenues in the next three years through this strategy.

The group even surprised the investors by posting a 31.9% yoy increase in net operating income to $25.5 million in the first quarter of fiscal year 2016. The transactions rose 22% on a year over year basis to 193,000 during the period, with the active clients reaching 148,000 by the end of the quarter. Moreover, the group’s gross revenues was more than $10 million in the month of July, breaking its historical records. Ozforex is estimating its EBITDA to be in the range of $38.5 million to $40.5 million for the current fiscal year. Although the group took twelve years to reach $100 million of revenues, it aims to achieve >$200 million by 2019, through its accelerated strategy. Accordingly, OFX estimates to incur further costs of $20 million for FY17 and FY18.

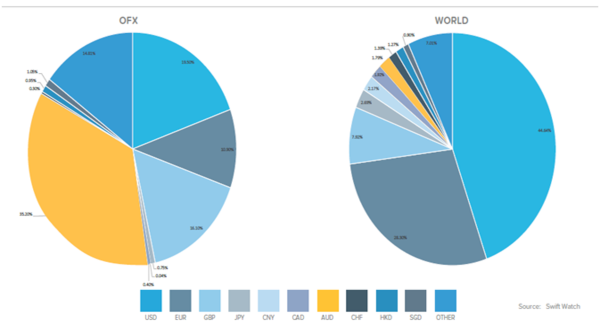

Growth opportunities by region (Source: Company Reports)

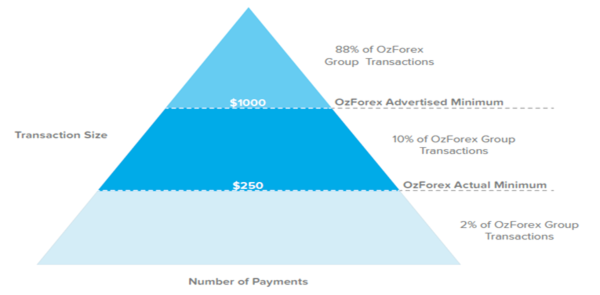

Investors should note that OzForex offers competitive prices for users who wants to send and get foreign currency for transactions above $1,000. The group derives 88% of its transactions in this category. The group is also focusing on smaller value payments in the future as just 10% of the group’s transactions are in $250 to $1000 range. The stock was under pressure since starting of this year, touching a low of $2 in July, impacted by its growth concerns. However, we believe that the group is quite competitive as compared to its peers in this niche market and its recent accelerated strategy have answered pretty much most of the concerns.

Potential to grow lower value payments (Source: Company Reports)

Based on the foregoing, we reiterate our “BUY” recommendation on the stock at the current price of $2.58.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

AU

AU

Please wait processing your request...

Please wait processing your request...