Perpetual Ltd

.JPG)

PPT Details

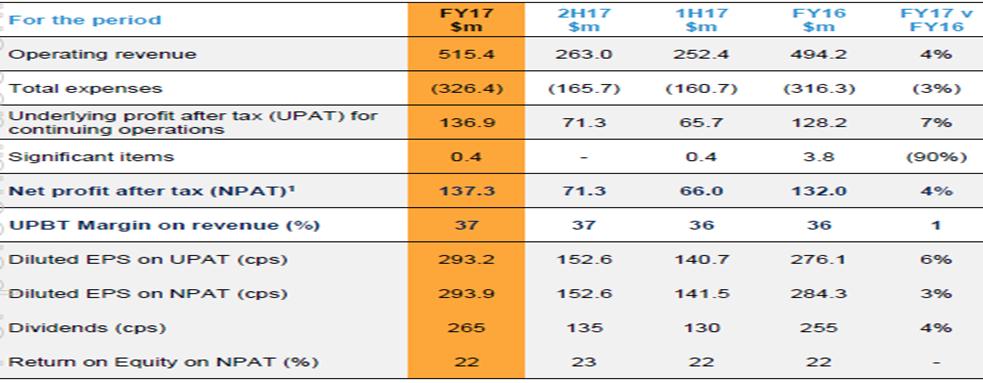

Continual new client growth: Perpetual Ltd’s (ASX: PPT) stock moved on volatility and slumped 4.9% on September 06, 2017, as the group traded ex-dividend. For FY17, PPT had reported 4% yoy (year on year) growth in statutory net profit after tax (NPAT) and revenue at $137.3 million, and $515.4 million respectively. Profit before tax for Perpetual Investments declined by 1% yoy to $116.5 million, largely driven by lower performance fees and partially offset by higher average funds under management due to higher equity markets. Despite challenging market conditions for active value investors, 88% of its funds are in the first or second quartile over five years, 100% over seven years and 83% over ten years. Perpetual Private’s profit before tax surged 18% yoy to $40.5 million, as a result of new client growth in target segments and higher non-market related revenue. Importantly, Perpetual Private’s targeted client segmentation strategy has delivered eight consecutive halves of net new client growth. Profit before tax from Perpetual Corporate Trust’s was up 8% yoy to $36.7 million, driven by growth in Managed Funds Services, underpinned by strong commercial property and infrastructure markets.

Group financial performance; (Source: Company reports)

Over the past twelve months, the stock has moved up by 17.7% as on September 05, 2017, and currently trading at higher levels. We give an “Expensive” recommendation on the stock at the current price of $ 52.59

Insurance Australia Group Ltd

.JPG)

IAG Details

Growth in gross written premium: Another financial stock that traded ex-dividend on September 06, 2017 is Insurance Australia Group Ltd (ASX: IAG), which slipped 3.9%. This financial sector stock had reported 6.8% yoy growth in insurance profit at $1.3 billion and 60 basis points (bps) increase in margin at 14.9% for FY17 against FY16. This improvement was driven by higher than expected prior period reserve releases, partially offset by a natural peril claim cost increase which resulted in an allowance overrun of over $140 million. Gross written premium (GWP) grew by 3.9% to $11.8 billion, with like-for-like growth more than 4%, driven mainly by higher rates on short tail motor in response to claims inflation as well as continued momentum in IAG’s Australian commercial rates. However, IAG’s underlying insurance margin, its preferred business performance measure, fell 2.1 percentage points to 11.9%, which included the adverse impact of higher claim costs in its short tail motor businesses in Australia and New Zealand, and elevated large losses in its commercial classes.

.png)

Financial summary; (Source: Company reports)

On guidance front, IAG expects to report an improved underlying operating performance in FY18 with low single digit GWP growth on account of ongoing rate initiatives to help address short tail claim pressures, and further positive rate momentum in commercial classes, both in Australia and New Zealand. Accordingly, the company anticipates margin of 12.5-14.5% for FY18. The stock has moved up 14.8% over the past twelve months while it is down 3.6% in last one month as on September 05, 2017. Given the modest performance and improving outlook, we maintain a “Hold” recommendation at the current price of $ 6.20

Macquarie Group Ltd

.JPG)

MQG Details

Mixed quarterly update: Macquarie Group (ASX: MQG) was down 2.3% on September 06, 2017, at the back of sector driven weakness and impact from US banks that led the Wall Street sell-off overnight. For Q1FY18, Macquarie Asset Management’s (MAM) assets under management declined 4% qoq (quarter on quarter) to $A460.8 billion at 30 June 2017, largely due to net asset realisations in Macquarie Infrastructure and Real Assets (MIRA), partially offset by favourable market and foreign exchange movements. MIRA’s equity under management was also down 4% to $A74.2 billion from $A77.2 billion at 31 March 2017. On the other hand, Corporate and Asset Finance’s (CAF) asset and loan portfolio of $A36.2 billion was in line with 31 March 2017. During the quarter, there were portfolio additions of $A0.9 billion in corporate and real estate lending across new primary financings and secondary market acquisitions. In addition, $A0.8 billion of motor vehicle and equipment leases and loans were securitised. Banking and Financial Services (BFS) deposits stood at $A47.3 billion at 30 June 2017 (6% up from 31 March 2017). Further, the Australian mortgage portfolio of $A29.4 billion increased 2% while funds on platform increased 10% to $A79.1 billion from 31 March 2017, largely due to the final migration of full service broking accounts to the Vision platform. Given the intensifying competition in the sector and margin pressure due to prolonged interest rates, we give an “Expensive” recommendation on the stock at the current price of $ 84.00

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...