Qantas Airways Limited

.PNG)

QAN Details

Transformation program to decrease costs: Qantas Airways Limited (ASX: QAN) is re-balancing its capacity from the resource sector towards east coast business and premium leisure markets. Qantas is partnering with global technology company ViaSat to tap into the potential of the National Broadband Network and to introduce an industry leading wifi service across its domestic fleet. The company has resorted to fare cuts, to boost the number of passengers and accordingly Qantas Group domestic fares are on an average 20 to 25 per cent lower than ten years ago in real terms. Some of its international fares are more than 50 per cent cheaper and 70 per cent of Jetstar passengers travel for less than $150 dollars. The group is also undertaking $2 billion transformation program to save costs via restructuring by the end of financial year 2017. On the other hand, QAN had witnessed a decline in international air freight demand in the first half of 2016. The group’s Revenue per Available Seat Kilometer (RASK) fell in the month of April on the back of falling yield performance in domestic and international businesses Domestic (including Qantas Domestic and Jetstar Domestic) capacity in the month was 0.5% lower, due to tough markets conditions and impact of the group’s efforts to cut its domestic capacity in the fourth quarter of financial year 2016.

.PNG)

Qantas April performance (Source: Company Reports)

Despite the group’s share buy-back completion of $500 million, the company’s stock fell over 29.31% (as of June 15, 2016) in the last three months impacted by its weak performance. The group has returned over $1 billion in surplus capital to shareholders over the last one year. We believe that QAN stock may continue to face some pressure in the coming months and we maintain our “Expensive” recommendation on the stock at the current price of $2.85

QAN Daily Chart (Source: Thomson Reuters)

Virgin Australia Holdings Ltd

.PNG)

VAH Details

Strategic Alliance with HNA Aviation: Virgin Australia Holdings Ltd (ASX: VAH) formed a strategic commercial alliance with HNA Aviation Group Co. to leverage its rapidly growing Chinese travel market. HNA will make an equity investment for this in the group in the form of A$159 million placement of shares at an issue price of A$0.30 per share which is a premium of 7.1 per cent to the last close on 30 May 2016. After the placement, HNA will have a shareholding of over 13% in the Virgin Australia Group which HNA will increase to 19.99% after the capital restructuring. Meanwhile, VAH has undertaken a major transformation program over the past five years including capital restructuring to evolve from a low cost carrier to a diversified airline group by optimizing the balance sheet. As per the latest news, Virgin announced the outcomes of its capital structure review while proposing fully underwritten A$852 million equity raising, in the form of a 1 for 1 non-renounceable pro-rata entitlement offer to shareholders at a price of A$0.21 per share (Offer). Air New Zealand made the financial investment in VAH and would provide a new unsecured term loan facility. Other major shareholders including Etihad Airways, Singapore Airlines and Virgin Group are providing debt to the company for a debt refinancing as a part of transformation program. However, in March 2016, Air New Zealand announced that it is considering to sell its 25.99% stake in Virgin Australia and had hired First NZ Capital and Credit Suisse as the advisor for the various options. AIZ has now agreed to participate in Virgin rights issue. The company has witnessed weaker operating cash flows in the first half 2016 and its working capital movement is impacted by the increased receivables from corporate travel agents. Statutory Loss after Tax fell over $30.5 million to $58.8 million in the third quarter of FY15, due to restructuring charges. VAH is now targeting net free cash flow savings rising to A$300 million per annum by end of FY19.

.PNG)

Virgin’s third quarter performance (Source: Company Reports)

Nonetheless, Virgin Australia expects a weaker group capacity in the fourth quarter and accordingly cut group capacity by 5.1% on the back of challenging consumer demand. Virgin's share price dropped over 39.53% (as of June 15, 2016) in the last three months impacted by weak performance and Credit Suisse indication of a possible requirement for A$1 billion equity raising by the group which is double the previous expectations, for controlling debt to reasonable levels.

Based on the foregoing, we give an “Expensive” recommendation on the stock at the current price of $0.255

VAH Daily Chart (Source: Thomson Reuters)

Air New Zealand Ltd

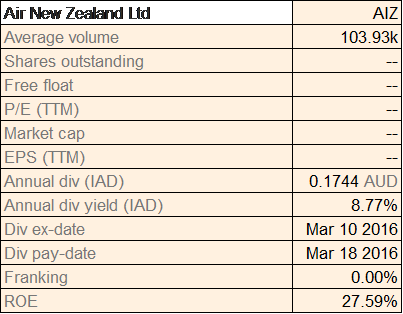

AIZ Details

Approach to enhance efficiency: Air New Zealand Ltd (ASX: AIZ) recently reported that it carried 1,071,000 passengers in May 2016 resulting in a 4.1% surge over same period last year. There was a 7.3% rise in revenue passenger kilometers (RPKs) on a capacity (ASKs) rise of 6.9%. The group lately also reported about Fuel Hedge Position, and that it has a Brent Collars volume of 3.09 million Barrels at a Ceiling Price of $ 50.07 and a floor price of $35.81 for second half of FY16. Overall, AIZ has a total hedged volume of 74% as proportion of total and estimated fuel consumption of 4.16 million barrels in second half of FY16. Meanwhile, on a medium term basis the group is focusing on Virgin Australia investment, fleet simplification and financial framework. AIZ has also announced the review of a Virgin Australia investment including a possible sale of all or part of their shareholding. The company intends to reduce the number of fleets by 2018 under its fleet simplification program. AIZ will close two regional routes, Whanganui to Auckland and Blenheim to Christchurch from the end of July due to insufficient demand.

May 2016 update (Source: Company Reports)

On the other hand, the group’s stock has been under pressure and fell over 17.89% (as of June 15, 2016) in the last three months. AIZ also reported weak group-wide yields for the financial year to date as of April 2016 which fell by 1.5% against prior corresponding year.

Short Haul yields dropped 1.8% on a yoy basis while Long Haul yields improved by 2.0% yoy. Group-wide yields lost 5.5% excluding the impact of foreign exchange. We believe that AIZ stock would be under pressure in the coming months despite the group’s efforts to enhance its efficiency given the weakening demand coupled with rising oil prices and accordingly, we give an “Expensive” recommendation on the stock at the current price of $2.05

AIZ Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...