.png)

Stocks’ Details

Woodside Petroleum Limited

Sangomar Development Gets a Nod for the Exploitation PlanExecution: Woodside Petroleum Limited (ASX: WPL) is engaged in the evaluation, development, operation and management of hydrocarbon. On 10th January 2020, the company stated that the Sangomar Field Development Phase 1 (Sangomar Development) was approved by the JV of Rufisque Offshore, Sangomar Offshore and Sangomar Deep Offshore (RSSD) and WPL has begun with the execution of activities with respect to the same.

Other Recent Updates:On 24th December 2019, the company stated that Woodside Energy Trading Singapore Pte Ltd executed a long-term sale and purchase agreement with Uniper Global Commodities SE for a period of 13 years, starting in 2021.

Key Highlights of the Quarter Ended 30 September 2019:During the quarter, the company’s sales revenue stood at $1,164 million, up 58% on a sequential basis. The rise can be attributed to a 44% increase in production and higher realised LNG pricing. The company provided a production of 24.9 mmboe and attained 99.7% reliability at Pluto LNG in the third quarter.

.png)

LNG Production Highlight (Source: Company Reports)

Outlook: The company said that its main growth projects are proceeding well towards key decision points. The company anticipates Pluto LNG and the Greater Enfield Project to be the key contributors for attaining a production goal of approximately 100 MMboe in 2020.

Valuation Methodology:Price to Book Multiple Approach

.png)

P/BV Based Valuation (Source: Thomson Reuters), *1 USD = 1.45 AUD

Note: All the forecasted figures have been taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: As per ASX, the stock is trading above the average of its 52-week low and high of $30.580 and $37.70, respectively. The stock gave a return of 7.1% in the past one year. Quick ratio and current ratio of the company stood at 3.31x and 3.45x, higher than the industry median of 0.82x and 1.17x, respectively. Considering thedecent financial performance and current trading levels, we have valued the stock using P/BVbased relative valuation method and for the purpose we have taken the peer group - Origin Energy Ltd (ASX: ORG), Beach Energy Ltd (ASX: BPT) and Oil Search Ltd (ASX: OSH), to name few. Therefore, we have arrived at a target price of lower double-digit growth (in % terms). Hence, we recommend a “Hold” rating on the stock at the current market price of $35.66, up 0.649% on 14h January 2020.

Origin Energy Limited

Integrated Gas Revenue Increased by 7% Year Over Year: Origin Energy Limited (ASX: ORG) is an Australia-based public company, which handles energy businesses that comprise the production of natural gas, along with the generation of electricity. On 23rd December 2019, the company announced that Frank Calabria, one of the Directors, has disposed 50,000 common shares for a consideration of $8.80 per share.

September Quarter 2019 Highlights: During the quarter, the company’s APLNG production improved 3% on a year over year basis, due to higher well accessibility and the ERIC pipeline online since July 2019. Revenue from integrated gas rose 7% to $687.9 million in the quarter, mainly due to greater Australian dollar oil prices and improved LNG volumes. Electricity Sales from Energy Markets declined 8% year over year. Natural gas sales declined 7% year over year, due to lack of short-term wholesale contracts in Queensland.

.png)

Quarterly Highlights (Source: Company Reports)

Outlook: In FY2020, the company expects Australia Pacific LNG (APLNG) production to be in the band of 690 to 710 petajoules. In FY2020, Energy Markets’ Underlying EBITDA is predicted to be between $1,400 – $1,500 million. The company continues to anticipate capital expenditure and investments, to be in the band of $530 to $580 million.

.png)

FY20 Guidance (Source: Company Reports)

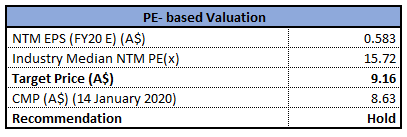

Valuation Methodology:Price to Earnings Multiple Approach

Price to Earnings Based Valuation (Source: Thomson Reuters)

Note: All the forecasted figures have been taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: As per ASX, the stock is trading close to its 52-week high of $8.890. The stock gave a return of 24.17% in the past one year. Quick ratio of the company stood at 1.18x, higher than the industry median of 1.03x. The business has drawn further growth opportunities, after continued production at Australia Pacific LNG and cost control initiatives. Considering thedecent financial performance, outlook and current trading levels, we have valued the stock using a price to earnings based relative valuation method and for the purpose,we have taken the peer group - AGL Energy Ltd (ASX: AGL), Woodside Petroleum Ltd (ASX: WPL) and Oil Search Ltd (ASX: OSH), to name few. Therefore, we have arrived at a target price of single-digit growth (in % terms). Hence, we recommend a “Hold” rating on the stock at the current market price of $8.630, up 0.583% on 14January 2020.

AGL Energy Limited

FY20 Underlying PAT to Decrease against FY19:AGL Energy Limited (ASX: AGL) is an Australia-based top integrated energy business. On 6 January 2020, the company announced the cancellation of 1499200 ordinary shares bought back under an employee share scheme buy-back programme.

Other Recent Highlights: On 2 January 2020, the company announced that it has bought back a total of 16,821,581 shares for a total consideration of ~$331,734,068. In another update, the company announced that State Street Corporation became a substantial holder of the company with a voting power of 5.02%.

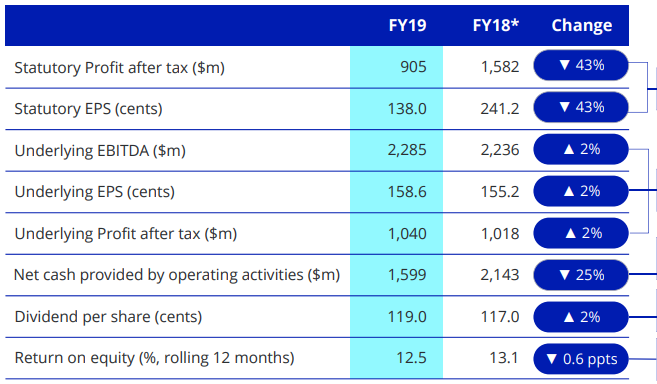

Financial Highlights for the Year Ended 30 June 2019:The company reported statutory profit after tax for FY19 at $905 million, down 43% year over year. Underlying EBITDA for FY19 stood at $2,285 million, up 2% year over year. Net cash provided by operating activities in FY19 was $1,599 million. The company declared a full year dividend of 119 cents per share.

FY19 Financial Highlights (Source: Company Reports)

Outlook:For 2020, the company predicts underlying EBITDA in the range of $780-$860 million, representing a decrease from FY19 on account of the impact of the outage of a unit till December 2019, increase in depreciation expense, lower wholesale price for electricity, etc.

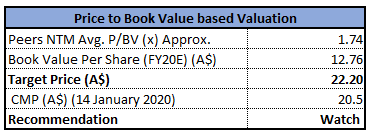

Valuation Methodology:Price to Book Multiple Approach

P/B Based Valuation (Source: Thomson Reuters)

Note: All the forecasted figures have been taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: As per ASX, the stock is trading close to the average of its 52-week low and high of $18.39 and $23.21, respectively. The stock gave a return of 6.73% in the past three months.

The company has acquired Perth Energy Holdings Pty Ltd for a total enterprise value of $93 million. The move will provide higher flexibility to AGL’s WA gas portfolio and will strengthen its competitive position. Considering theabove factors, we have valued the stock using P/B based relative valuation method and for the purposewe have taken the peer group - Origin Energy Ltd (ASX: ORG), Woodside Petroleum Ltd (ASX: WPL) and Beach Energy Ltd (ASX: BPT), to name few. Therefore, we have arrived at a target price of higher single-digit growth (in % terms). Hence, considering the above valuation and FY20 guidance, we have a watch stance on the stock at the current market price of $20.50, up 0.147% on 14h January 2020.

.jpg)

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...