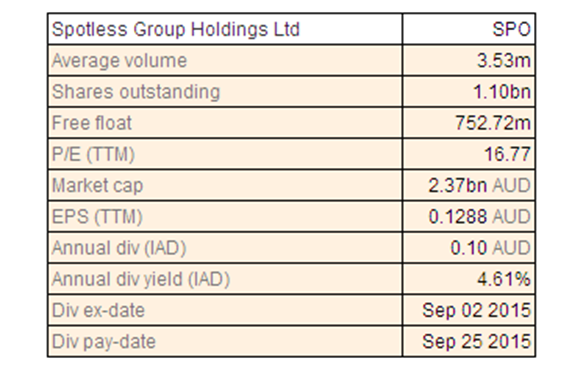

Spotless Group Holdings Ltd

SPO Dividend Details

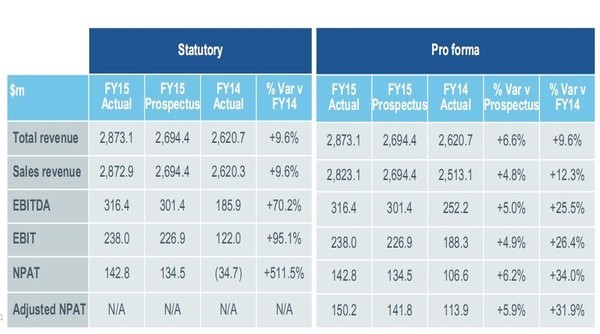

On strong trajectory through new contracts and acquisitions: The company produced impeccable results for FY 2015 which exceeded the prospectus forecast. Statutory sales revenue was up 9.6% over the previous year to $ 2.87 billion and pro forma sales were up 12.3%. Statutory EBITDA was up 70.2% to $ 316.4 million and pro forma EBITDA was up 25.5%. Statutory NPAT was up 511.5% to $ 142.8 million with the pro forma number up by 34% while adjusted pro forma NPAT was up 31.9% to $ 150.2 million. The company established a strong platform for growth with five acquisitions during the year and over $ 950 million per annum in renewals and in excess of $ 350 million per annum in new contracts wins. Leverage continues to be low with net debt to EBITDA of 1.8x providing the opportunity to finance further growth in FY 2016. The company, because of the strength of the business performance and the pipeline, declared a dividend of 5.5 cents per share.

Performance Overview (Source: Company Reports)

The organic growth has been impressive and notable new contract wins include facilities management contracts for the Melbourne Airport Terminal, catering contracts for Newcastle Airport, Emirates lounges nationally, the Western Australia Department of Housing and Aurrum Aged Care. Other catering contracts include JetStar at Brisbane International Airport, Adelaide City Council and Auckland City Council. Contracts which combine facilities and township management, catering and cleaning were concluded with Glencore's Lady Loretta mine in Queensland, BHBP Kurra Village and Olympic Dam at BHP Billiton. The company also expects the results for FY 2016 to be substantially better than the results for FY 2015. The stock has fallen 4.85% in last six months (as at November 04, 2015). Nonetheless, we believe that the company is in a strong position and should have no difficulty in achieving these better results and have no hesitation in recommending the stock as a Buy at the current price of $2.15.

Flight Centre Travel Group Ltd

FLT Dividend Details

Set to fly high with new revenue stream through AVMIN: In the latest development, the group has announced that it is boosting its leisure and corporate offerings by acquiring a leading Australian specialist in charter aircraft and logistics solutions. It is acquiring a 51% stake in a private company based in Brisbane, AVMIN Pty Ltd, and the existing top management of said company will continue to retain 49% and oversee the day-to-day operations. AVMIN specialises in complete fly in and fly out logistics as well as ad hoc charter aircraft and VIP travel both in Australia and internationally, and has a solid client base across industries such as mining and resources and construction along with having a strong track record. The acquisition will provide FLT with a new and profitable revenue stream and future opportunities for launching new services where charter is a viable alternative to scheduled air services as well as providing charter services on underserviced routes and in niche markets. Separately, the group has recorded its disappointment that the ACCC has launched a further appeal against the competition Law test case that it initiated in 2012. You will recall that the Full Court of the Federal Court of Australia ruled unanimously in favour of the company. We continue to believe that the group has considerable growth potential and that the new acquisition will only make it a better investment. We also believe that the ACCC action will not have a material impact on the prospects of the company.

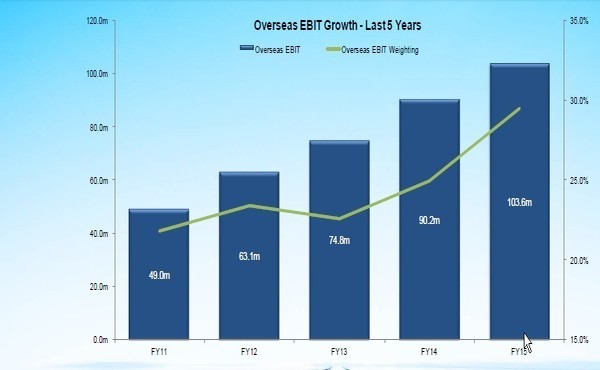

Overseas EBIT Growth (Source: Company Reports)

The stock has fallen about 14% in the last six months (as at November 04, 2015) and recovered about 0.67% in last one month. We continue to regard this company highly and to reiterate our Buy rating on the stock at the current price of $37.48.

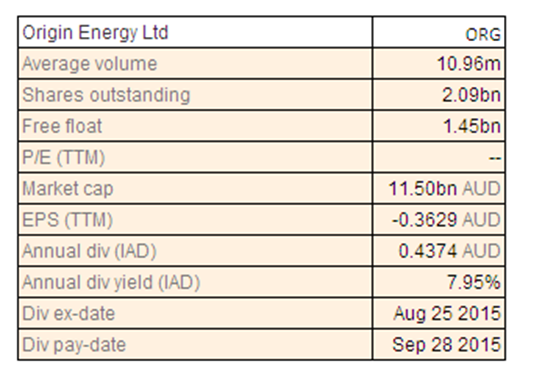

Origin Energy Ltd

ORG Dividend Details

Stake in APLNG and quality gas reserves to strengthen position: In the quarterly production report for September 2015, the company reported a 13% increase over the preceding quarter’s production owing to improved production as Australia Pacific LNG ramps up ahead of the first LNG cargo and the commencement of production at the new Yolla-5 AND Yolla-6 production wells in the Bass Basin. Despite the strong increase in production, revenue declined by 1% because of the lower prices for liquids and the lower average gas prices realised by the company. When compared to the same quarter of the previous year, production increased by 37% while revenues decreased by 10%. The company said that it is on the brink of achieving two major milestones at Australia Pacific LNG with the commencement of production shortly and the first LNG cargo shortly thereafter. Flow testing of the Waitsia 1 appraisal well has shown positive results with a total combined flow rate of better than 50 million standard cubic feet/day from the Kingsia and High Cliff Sandstones Zones. The appraisal well reached a total depth of 3530 m and has been cased and suspended for future production. We also note that Senex Energy has provided an update about drilling of the Efficient-1 gas exploration well in the South Australian Cooper Basin under its exploration program with Origin. Then Beach Energy also updated about the six-well development campaign which is underway in the Tirrawarra and Gooranie fields under the development program with ORG and Santos. Even the Windorah near-field exploration program (Beach, Santos and Origin) for Queensland gas indicated casing and suspension of the third well of the campaign following intersection of gas pay that exceeded pre-drill estimates.

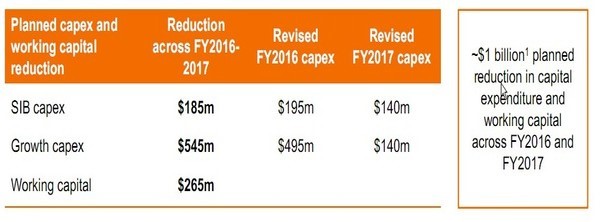

Capex Reduction (Source: Company Reports)

The company has also successfully completed the second stage of the Retail Entitlement Offer of the $ 2.5 billion equity raising of which the institutional component of roughly $ 1.35 billion was completed earlier. The retail offer attracted strong demand with valid acceptances for approximately $ 791 million accounting for approximately 66% of new shares available under the offer. The company has also completed its retail shortfall bookbuild. ORG has received an indicative approval from the Queensland Department of Natural Resources and Mines to transfer Roma Shelf assets to Armour Energy. In addition to the strengthening of the equity base, the company is set to grow its bottom line considerably over the next two years and we are optimistic that this growth rate will be achieved. ORG’s debt is expected to reduce by 2017 and there may be enough working capital to focus on the APLNG project given the current oil price situation. Based on the foregoing, we think this is a good buy opportunity at the current price of $5.45.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

AU

AU

Please wait processing your request...

Please wait processing your request...