BWP Trust

BWP Details

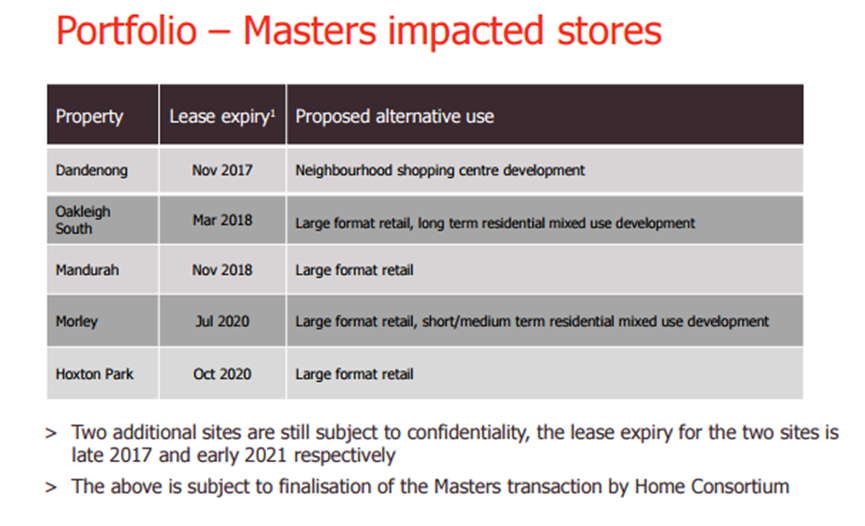

Weak performance:BWP Trust (ASX: BWP) reported its first half yearly performance for FY2017 with the total income growing a meagre 1.5% to $75.8 million. Distributable profit was up 4.1% to $55.5 million. The rental growth in the portfolio was at 2.4% and portfolio cap rate was at 6.77%. The net tangible assets of $2.60 per unit were reported and this was up 3.1%. BWP has zoned 15 properties for higher and better use. The management said that on the basis of expected rental growth from the existing portfolio, the company is expecting distribution per unit growth of 3% for FY2017 as mentioned earlier in August 2016. On the other side, the company’s major client Bunnings’ lease is expiring in next 3 years. Further, the company has five properties with lease expiry from November 2017 – October 2020 for its client Masters, which bears the risk of vacancy. The company said it would take immediate action to establish a repositioning or divestment strategy to manage the scenario.

Masters impacted Stores (Source: Company Reports)

Going forward, the company has concerns over the properties vacated or to be vacated by Bunnings to re-lease or re-zoning them. The company may also divest property if they have reached their valuation potential. The macro-economic factors also have an influence on the rent or portfolio growth opportunities. We believe that the stock is a “Sell” at the current market price of $ 2.78

.png)

BWP Daily Chart (Source: Thomson Reuters)

Growthpoint Properties Australia Ltd

GOZ Details

Rise in distributable income:Growthpoint Properties Australia Ltd (ASX: GOZ) reported a 16.8% rise in distributable income per security to 12.5 cents and a 4.2% increase in net tangible assets per security to $2.72 for H1FY17. The company has reweighted its property portfolio into office (66%) and NSW (26%). During the period the company has completed GMF takeover and integrated its assets adding $440.3 million and six office properties. Growthpoint Properties has sold $152.3 millions of industrial property during the period. The Company’s top five office properties contribute to 56% of office portfolio and are valued at $1,175.2 million with average seven years of lease expiry. The top five industrial properties account for 82% of industrial portfolio and are valued at $897.9 million with average lease of 5.5 years. The company has issued AUD 208 million in US Private Placement notes. The issue will comprise two tranches of USD denominated notes and one tranche of AUD across tenors of 10 and 12 years. On the other hand, the company reported that 55,126 sqm leasing was completed during the first half of 2017 and occupancy increased to 99%. The like to like property valuation gain was at 2.2% and property portfolio value increased by 12.8% to $3.2 billion as on December 2016. In terms of exposure, the company increased its exposure to NSW to 26% and office sector to 66% by December 2016 as compared with June 2016, while, GOZ has lowered Victoria industrial exposure to 13% from 20% as on June 2016.Given the volatile conditions in the sector, we feel the stock is a “Sell” at the current market price of $ 3.19

GOZ Daily Chart (Source: Thomson Reuters)

Investa Office Fund

IOF Details

Considering buying half of management platform: Investa Office Fund (ASX: IOF) is under the ongoing takeover dispute and has to decide whether to acquire a 50% stake in its management platform until end of May 2017. This would lead to an important ramification for the future ownership of $3.8 billion real estate fund. Meanwhile, for the first half of 2017, the company has reported 1.4% rise in Funds from Operations (FFO) per unit and distributable profit was up by 2% to 10 cents per unit. On the other hand, statutory net profit was down by 20.2% to $224 million. The portfolio value stands at $3.8 billion as on December 2016 with 434 tenants and has 22 office buildings. The company reported that the portfolio capitalization rate was reduced by 19 bps to 6.01% while NTA enhanced 26 cents to $4.49 per unit by December 2016 end. During January and February 2017, the company divested two properties for $211.2 million at premium to its book value. The occupancy rate is 97% as on December 2016. Meanwhile, the company has said that it has received an offer from Cromwell Property Group to acquire all of IOF’s outstanding issued capital for $4.45 per unit; however, the offer was not compelling as per the company’s directors.

.png)

Outlook in terms of Market Fundamentals (Source: Company Reports)

IOF has increased its FY17 FFO and distribution guidance, each now representing a 3.1% growth over FY16. IOF stock rallied over 5.36% in the last six months (as of March 21, 2017) and is trading close to its full value.We believe investors can book profit as we give a “Sell” on the stock at the current market price of $ 4.76

IOF Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...