-

Research Reports

- High-Risk High-Reward

- Technical Analysis Reports

-

Low-To-Medium Risk

- Inflation Report

- Dividend Income Report

- Earnings Hunter Report

- kalGOLD® (Kalkine Gold Report)

- Healthcare Report

- KALIN®

- Kalkine Real Estate Report

- Kalkine Resources Report

- US Equities Report

- US Dividend Income Report

- Agriculture Report

- The Funds Report

- Global Tariff Report

- Global Travel and Leisure Report

- India Equity Opportunities Report

- Kalkine’s Global Critical Minerals Report

- Diversified Themes Reports

- Model Portfolios

- Screeners

- Daily Insights

- Market Analysis

-

AU

AU

.png)

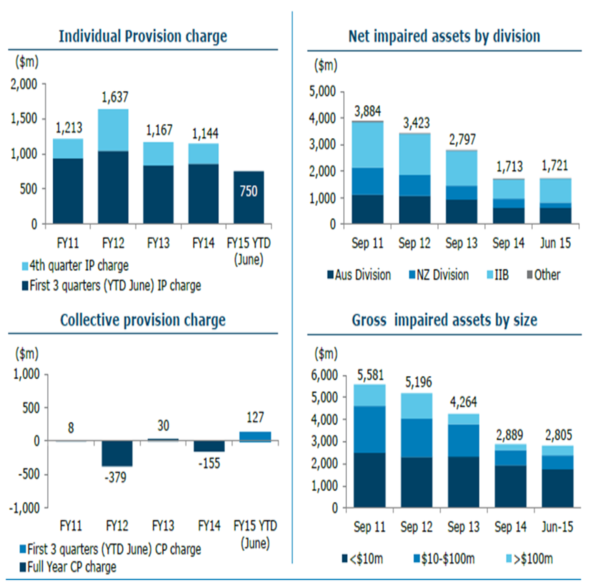

Delivered decent earnings performance, focusing on super regional strategy: Australia and New Zealand Banking Group (ASX:ANZ) generated decent performance in spite of the CET1 ratio pressure, with the group’s cash profit surging by 4.3% year-on-year (yoy) to $5.4 billion in the nine months ended on June 30 of fiscal year of 2015. Statutory profit improved by 11% yoy to $5.6 billion in 2015, against $5 billion in prior corresponding period (pcp), on the back of better customer franchises across Australia, New Zealand and Asia Pacific. Customer deposits witnessed solid performance with a surge of 9.5% on a year over year basis, driven by net loans and advances increase by 7.7% yoy during 2015. The bank is also selling its Esanda dealer finance business, an $8.3 billion business of loans to motor vehicle dealers, to focus on its core business. In fact, the latest update reveals that the Australian antitrust regulator has given the decision of not opposing a possible bid from Macquarie for ANZ’s vehicle-finance unit. Global markets business income for ANZ rose 6% yoy to $1.8 billion during the nine months ended on June 30 of fiscal year of 2015, while the customers for International and Institutional Banking improved 9% yoy, boosted by Asian business. ANZ is heavily focusing on its Asian business growth and launched a “super-regional strategy” program to build a solid presence in Asia as compared to its Australian peers.

Delivered decent earnings performance, focusing on super regional strategy: Australia and New Zealand Banking Group (ASX:ANZ) generated decent performance in spite of the CET1 ratio pressure, with the group’s cash profit surging by 4.3% year-on-year (yoy) to $5.4 billion in the nine months ended on June 30 of fiscal year of 2015. Statutory profit improved by 11% yoy to $5.6 billion in 2015, against $5 billion in prior corresponding period (pcp), on the back of better customer franchises across Australia, New Zealand and Asia Pacific. Customer deposits witnessed solid performance with a surge of 9.5% on a year over year basis, driven by net loans and advances increase by 7.7% yoy during 2015. The bank is also selling its Esanda dealer finance business, an $8.3 billion business of loans to motor vehicle dealers, to focus on its core business. In fact, the latest update reveals that the Australian antitrust regulator has given the decision of not opposing a possible bid from Macquarie for ANZ’s vehicle-finance unit. Global markets business income for ANZ rose 6% yoy to $1.8 billion during the nine months ended on June 30 of fiscal year of 2015, while the customers for International and Institutional Banking improved 9% yoy, boosted by Asian business. ANZ is heavily focusing on its Asian business growth and launched a “super-regional strategy” program to build a solid presence in Asia as compared to its Australian peers.

.bmp)

.png)

Please wait processing your request...

Please wait processing your request...