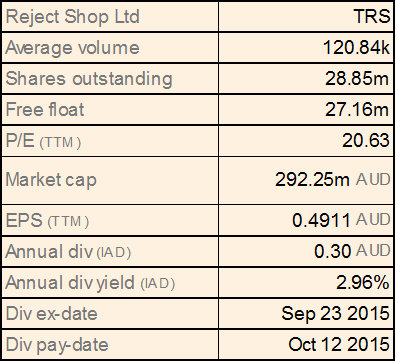

The Reject Shop Ltd

TRS Dividend Details

Disappointing first half FY15 performance impacted full year profit: The Reject Shop Ltd (ASX: TRS) reported its FY 2015 with topline sales growth of 6.4% which must be considered satisfactory because of the challenging first quarter performance which led to a disappointing result for the half-year. This growth was achieved through a combination of the sales benefits of the new stores opened during FY 2014 and FY 2015 as well as continued quarter by quarter improvements in same store growth which finished at +2.3% for the second half of the year and +4.7% in the fourth quarter. Because of the disappointing first half year performance, the full-year net profit after tax was slightly below that of the previous year though the business has returned to profit growth in the traditionally challenging second half of the year. In the new financial year, the change in sales momentum has continued into the first quarter of FY 2016 and comparable sales have been reported to be well above what was achieved in the previous year. This has been achieved in the context of a difficult retail environment in which disposable income in real terms continues to be flat and there is continued uncertainty about employment prospects.

Building Blocks to Success (Source: Company Reports)

TRS further stated that three new stores were opened in the first 13 weeks of FY16 with three stores relocated and five more store openings planned for the remainder of the year. The company continues to improve its offering and the operational improvement initially is focused on getting back to basics with a heightened focus on the customer. The share price has risen substantially since the results announcement in August and 58.78% this year to date (as at December 11, 2015). We think that the future prospects do not really justify the price.

Further, risks from discount department stores such as Big W, Kmart and the like do persist. We believe that the shares are expensive at the moment.

TRS Daily Chart (Source: Thomson Reuters)

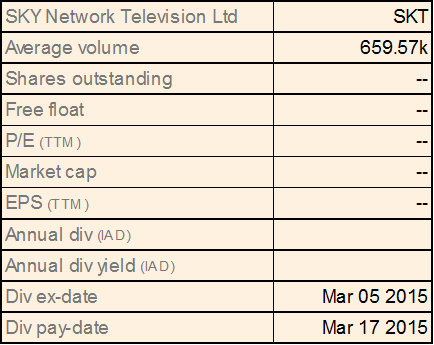

Sky Network Television Ltd

SKT Details

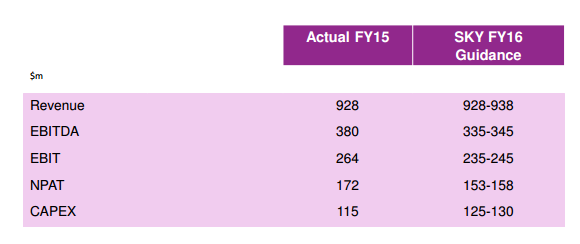

Conservative FY16 Guidance: Sky Network Television Ltd (ASX: SKT) has fallen 29.38% this year to date (as at December 11, 2015) despite reporting a successful FY15 given a very challenging market with rapidly changing technology and emergence of new competitors. For the year, it reported record revenues of $ 928 million while net profit after tax increased to a record figure of $ 171.8 million and the total dividend for the year was 30 cents per share up from a total of 29 cents per share in the previous year. The strong results were achieved despite an overall reduction of subscribers, and as at 30 June 2015, the company had market penetration of 48% of New Zealand homes with 851,561 subscribers. The company is taking advantages of the opportunities arising from changing technology and customer preferences and using the improved speed and reliability of the Internet. Despite delays, the company is well into an extended trial of the new On Demand service and customers will receive a brand-new interface with new features that enhance the viewing experience.

FY16 Guidance (Source: Company Reports)

Other features include improved presentation of recorded content, stacking shows from one series under one title and enhanced search capabilities. The most important feature in On Demand is the one that the internet allows subscribers to catch up with a vast selection of shows along with recent pay-per-view movies which can be downloaded at the touch of a few buttons. Last year, the company launched Sky Go which lets customers view content on other screens such as phones and tablets, and there have already been 335,000 downloads of the app. Neon is the monthly video on demand subscription service launched early this year which has a strong line-up of content with new release movies and quality drama from world-class production houses. The growth so far has been satisfactory.

Despite the above, we don’t expect great upside in earnings and revenues in view of the conservative guidance. Consequently, we think that the current stock price overvalues the stock.

SKT Daily Chart (Source: Thomson Reuters)

Transurban Group

.png)

TCL Dividend Details

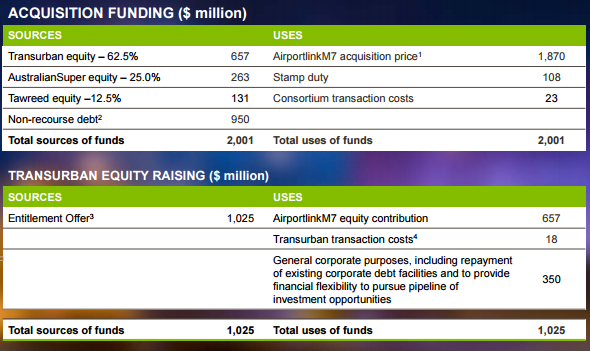

Acquisition of AirportlinkM7: Transurban Group (ASX: TCL) has surged 16.44% this year to date (as at December 11, 2015) and the company owns 62.5% of Transurban Queensland that has reached an agreement to acquire AirportlinkM7 for $ 1.87 billion plus stamp duty of $ 108 million and transaction costs of $ 23 million. AirportlinkM7 is an urban tunnel connecting Brisbane airport and the Australia TradeCoast with the CBD and the northern, southern and western suburbs of Brisbane. Recent upgrades to the network including Legacy Way and the increase in toll prices have substantially increased the earnings profile from 1 July 2015. The acquisition remains conditional on the consent of the Department of Transport and Main Roads as well as the approval of the ACCC. The financial closing is targeted for the first quarter of calendar year 2016. The acquisition strengthens the network of Transurban Queensland and further diversifies the group portfolio. The group expects to raise $ 1.025 billion through a fully underwritten pro rata accelerated renounceable entitlement offer and the proceeds will be used to fund the acquisition, reduce debt and provide the financial flexibility to pursue further investment opportunities.

Acquisition Funding (Source: Company Reports)

The exclusive negotiations with the Victorian Government for the Western Distributor project are on track but risks pertaining to financial close, traffic and operations do prevail. The company also intends to participate in the competitive process relating to procurement on I-66 by the Virginia Department of Transportation. First half FY 2016 distribution of 22.5 cents per share has been announced and the group has reaffirmed its distribution guidance of 44.5 cents per share for the whole of FY 2016. Given the entire scenario, we still believe that the stock is expensive at the moment.

TCL Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

AU

AU

Please wait processing your request...

Please wait processing your request...