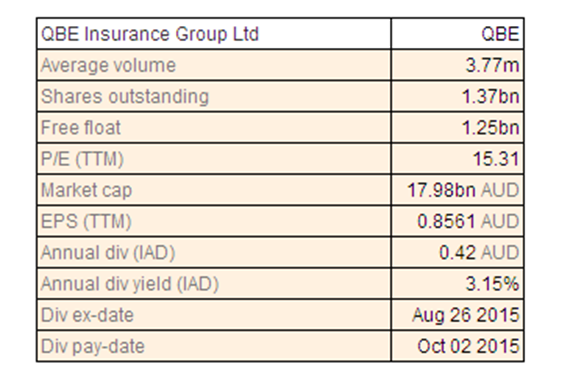

QBE Insurance Group Ltd

QBE Dividend Details

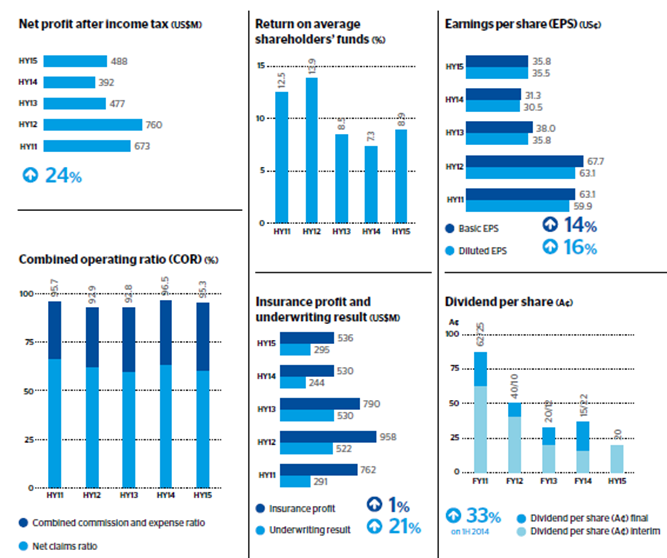

Weak first half performance: QBE Insurance Group Ltd (ASX: QBE) reported a revenue decline of 6% year on year (yoy) to $7,928 million in the first half of 2015. However, the group delivered an expense savings of $242 million during the period, and estimates to achieve more than $350 million. QBE net profit after tax improved by 24% yoy to $488 million during the period, driven by its sale of the Argentine workers’ compensation business in February. The group priced for over $200 million worth of Tier 2 subordinated debt with a term of 25 years, which accordingly would boost its gearing ratios and the group intends to repay over £300 million of maturing senior debt. On the other hand, QBE projects a decrease of its gross written premium to be in the range of $15.2 billion to $15.6 billion during fiscal year of 2015. The group reported a decrease of its Net investment income to $386 million in the first half of 2015 against $429 million in the first half of 2014.

QBE Insurance Group performance (Source: Company Reports)

QBE Insurance Group stock already delivered a solid returns of 18.9% (as of Oct 30, 2015) during this year to date, despite tough market conditions. On the other hand, the stock corrected over 8.75% in the last three months. Although the balance sheet is strong and the cost-out program is working out, second half of the year which is generally expected to be little costly may also witness some premium rate pressure. Given a weak outlook, we believe that the stock is “Expensive” at the current price of $13.25 , and would review the stock at a later date.

QBE Daily Chart (Source: Thomson Reuters)

Insurance Australia Group Ltd

.png)

IAG Dividend Details

Focusing on its core Australia and New Zealand business and Asia regions (except China) for growth:Insurance Australia Group Ltd (ASX: IAG) reported an Insurance profit decline to $1.1 billion in the fiscal year of 2015 against $1.6 billion in the fiscal year of 2014 as the net natural peril claims surged to $1.05 billion in FY15, exceeding the allotted allowance of $700 million for the year by additional $348 million. On the other hand, IAG entered into a strategic relationship with Berkshire Hathaway to protect its earnings volatility and capital requirements for the next ten years. The group intends to maintain 15% return on equity, as Berkshire Hathaway alliance would reduce IAG’s capital requirement of over $700 million for the next five years, while $400 million of that benefit might be realized by FY16. IAG is also targeting to boost its Asia pacific markets by raising its stake in the State bank of India and acquiring PT Asuransi Parolamas for insurance license in Indonesia. But, the group recently clarified that it would not be making any further investments in China. Insurance Australia Group recovered over 15.91% in the last four weeks (as of October 30, 2015) and we believe this positive momentum to continue. IAG issued a fairoutlook in next fiscal year and expects insurance margin to be in the range of 14% to 16%, including the contribution from the Berkshire Hathaway agreement.The Group also has a decent annual dividend yield of 5.17%. We maintain our positive stance on the stock and give a “BUY” recommendation at the current levels of $5.61.

IAG Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

AU

AU

Please wait processing your request...

Please wait processing your request...