BHP Group Limited

Decent ROCE for FY19 at 18% than 15% on previous year:BHP Group Limited (ASX: BHP) is involved in the exploration, development and production of oil and gas, mining of copper, silver, lead, zinc, molybdenum, uranium, iron ore and gold, and mining of metallurgical coal and energy coal. The company recently announced a change in the director’s interest, where Susan Kilsby acquired 2,900 ordinary shares in BHP Group Plc at GBP 17.13 per share, effective from August 23, 2019. Another Director, Andrew Mackenzie acquired 63,486 shares and disposed 31,309 shares, taking the final holding to 391,433 ordinary shares, 1,369,104 Performance Shares and 52,061 Deferred Shares, effective from August 21, 2019.

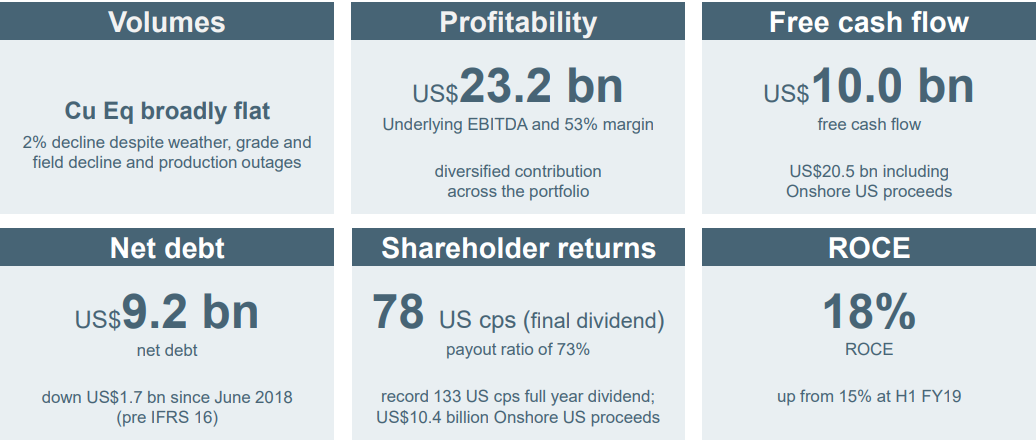

FY19 Key Highlights:Revenue from continuing operations increased by 3% to US$44,288 Mn, whereas revenue from discontinued operations decreased by 61% to US$851 Mn, taking the total revenue for the financial year 2019 at US$45,139 Mn. Profit after taxation from continuing operations attributable to the members of the BHP Group for the period was reported at US$8,648 Mn, which saw an increase of 88% on the previous year. Loss after taxation from discontinued operations attributable to the members of the BHP Group increased by 88% to US$342 Mn, taking the profit after taxation attributable to the members of the BHP Group to US$8,306 Mn, which was an increase of 124% on previous year. Underlying attributable profit for the period increased by 2% to US$9.1 Bn. Net tangible assets per fully paid share on June 30, 2019 stood at US$10.11, as compared to US$11.25 in the previous year. The Board of Directors declared a fully franked final dividend for the current period of US 78 cents per share, as compared to US 63 cents per share in the previous corresponding period. The record date and payment date are on September 6, 2019 and September 25, 2019, respectively.

FY19 Key Metrics (Source: Company Reports)

What to Expect: As per the release, the group expects global growth to register near the lower end of a range of 3¼% to 3¾% for the 2019 calendar year. Any further escalation in trade protection or loss of business confidence is a downside risk for consensus views of the world economy, commodity demand and energy and metals prices in the FY2020. Based on the economic and commodity outlook, the group has provided FY20 guidance.

Stock Recommendation: BHP’s share generated a positive YTD return of 12.38%. EBITDA margin and net margin for FY19 stood at 51.3% and 21.5%, better than the industry median of 29.5% and 14.0%, respectively, implying a decent fundamental for the company. Its ROE for FY19 stood at 16.8%, better than the industry median of 12.5%, implying that the company generated a better return for its shareholders than its peer group. Its current ratio for FY19 stood at 1.89x, better than the industry median of 1.71x, indicating that the company is in a better position to address its short-term obligations than its peer group.Considering the aforesaid facts and current trading levels, we recommend a “Hold” rating on the stock at the current market price of $36.580, up 0.799% on September 2, 2019.

Rio Tinto Limited

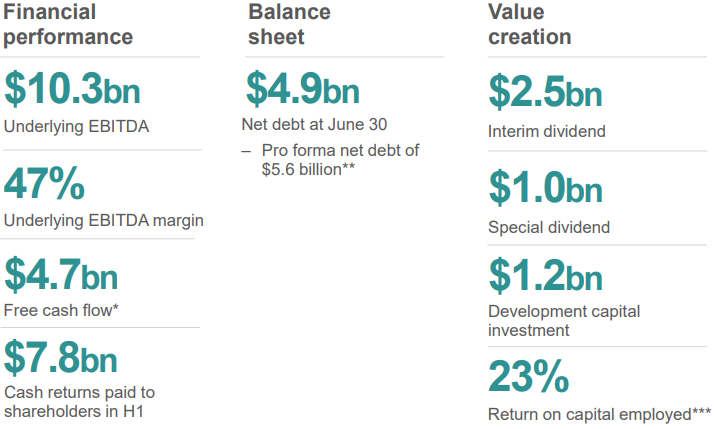

Group’s Sales Revenue for H1FY19 Increased by 9% to $20.7 Bn on pcp:Rio Tinto Limited (ASX: RIO) is involved in the minerals and metals exploration, development, production and processing and marketing. The company recently released its half-year results, where it highlighted that its underlying EBITDA and EBITDA margin were reported at $10.3 Bn and 47%, respectively. It was added that its financial performance was majorly driven by Pilbara operations with a 72% EBITDA margin, underpinned by strong iron ore prices. Free cash flow for the period was reported at $3.9 Bn, which was 35% higher than first half of FY18. Its cash balance at the end of the period was reported at $7.8 Bn, with net debt of $4.9 Bn.

Its underlying earnings for the period was reported at $4.9 Bn, which is 11.7% higher than the previous corresponding period, due to a strong contribution from Iron Ore.

It announced a cash return of $3.5 Bn, which comprised interim ordinary dividend of $2.5 Bn, equivalent to US 151 cents per share (A 219.08 cps), and special dividend of $1.0 Bn, equivalent to US 61 cents per share (A 88.50 cps). It will be payable on 19 September 2019 with a record date of 9 August 2019.

Consolidated sales revenue increased by 9% on pcp to $20.7 Bn, excluding the $0.8 Bn contributions from the coking coal assets divested in 2018. The higher iron ore prices offset the impact of lower volumes and lower aluminium prices.

H1FY19 Key Metrics (Source: Company Reports)

What to expect: As per the release, in 2019, RIO expects the run-rate from the mine-to-market programme to be around $0.5 Bn, despite weather impacts. This reflects operational challenges experienced in the Pilbara, which reduced 2019 first half run-rate to $0.2 Bn. The company expects its mine-to-market productivity programme to deliver an additional free cash flow run-rate of $1.0-1.5 Bn (previously $1.5 Bn) from 2021. The Capital Expenditure is expected to be around $6.0 Bn in 2019 and around $6.5 Bn in 2020 and 2021. The company is expecting an effective tax rate on underlying earnings of around 30% in 2019. The Pilbara unit cash costs are expected to come in at $14-15 per wet metric tonne (excluding freight) in 2019.

Stock Recommendation: Its EBITDA margin and net margin for H1FY19 stood at 47.7%, and 14.1%, better than the industry median of 33.1% and 13.7%, respectively, implying decent fundamentals of the company. Its ROE for H1FY19 stood at 9.9%, better than the industry median of 6.7%, implying that the company generated a better return for its shareholders than its peer group. On the valuation front, its next twelve months EV/Sales and EV/EBITDA multiple stood at 2.1x and 4.4x, above than the industry median (Next Twelve Months, NTM basis) of 1.5x and 3.1x, respectively, indicating an overvalued position at the current juncture. Currently, the stock is trading above the average of its 52-week trading range of $66.315 - $106.922. Hence, considering the aforesaid facts and current trading levels, we recommend an “Expensive” rating on the stock at the current market price of $88.830, up 1.427% on September 02, 2019.

Western Areas Limited

WSA share surged by ~14% post new (Ni-Cu Sulphides) Discovery Announcement:Western Areas Limited (ASX: WSA) is involved in the mining, processing and sale of Nickel Sulphide concentrate. On September 2, 2019, St George Mining Limited (ASX: SGQ) announced about a new discovery of high-grade nickel-copper sulphides at its flagship Mt Alexander Project (Joint Venture, St George Mining Limited (75%) and Western Areas Limited (25%)), located in the north-eastern Goldfields. This discovery of high-grade nickel-copper sulphides with the first ever drill hole in an area with about 10 meters of transported overburden and more than 1 km from the nearest known mineralisation on the Cathedrals Belt is an excellent exploration result.

FY19 Key Highlights:Company’s cash balance at the end of the period was reported at A$144.3 Mn, with no debt. Sales revenue for the period was reported at A$268.7 Mn, as compared to A$248.3 Mn in the previous period. Net Profit After Tax for the period was reported at A$14.2 Mn, as compared to A$11.8 Mn in FY18. The Board of Directors declared a fully franked final dividend of 2.0 cents per share, with record date and payment date on September 13, 2019 and October 4, 2019, respectively.

FY19 Key Metrics (Source: Company Reports)

FY20 Guidance:Nickel tonnes in Concentrate Production for FY20 has been estimated at 21,000 to 22,000 tonnes.Unit Cash Cost of Production (Nickel in Concentrate) for FY20 has been estimated at A$2.90/Ib to A$3.30/Ib. Mine Development cost has been estimated at A$33 Mn to A$38 Mn. Capital & Growth expenditure has been estimated at A$7 Mn to A$10 Mn. Odysseus Development cost has been estimated at A$75 Mn to A$85 Mn. Exploration cost has been estimated at A$14 Mn to A$17 Mn.

Stock Recommendation: WSA’s share generated a positive YTD return of 30.53%. Its current ratio for FY19 stood at 3.55x, which was better than the industry median of 1.71x, indicating a better position to address its short-term obligations than its peer group. Its long-term debt to total capital for FY19 stood at 0.1%, lower than the industry median of 5.4%. Hence, considering the aforesaid facts and current trading levels, we recommend a “Hold” rating on the stock at the current market price of $2.830, up 14.113% on September 2, 2019, on account of new discovery of Nickel-Copper Sulphide at its joint venture Mt Alexander Project.

Daily Comparative Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...