.png)

Stocks’ Details

BHP Group Limited

Reduced Guidance for FY19 Iron Ore Production:BHP Group Limited (ASX: BHP) released the operational activity report for March quarter. According to the report, the company witnessed strong performance on the operational front. Production of Petroleum at 29 MMboe witnessed a de-growth of 5% on q-o-q basis. Copper production stood at 1,245 kt on YTD basis which was down 3%. In March 2019 quarter, there was higher production from Olympic Dam which was largely offset by the impact of expected lower copper grades at Escondida. Iron Ore, Metallurgical coal and Energy Coal posted a flat growth on a YTD basis.

.png)

Operational Review for March Quarter (Source: Company Reports)

Financial Performance in 1HFY19: Thecompany recorded an attributable profit of US$3.8 billion and Underlying attributable profit of US$3.7 billion in 1H FY19. The underlying EBITDA for the period stood at US$10.5 billion with the margin of 52%.

.png)

Financial Performance for 1H FY19 (Source: Company Reports)

What to Expect: Themanagement has decreased the production guidance for Iron ore to be in the range of 265-270 Mt (100% basis) on the back of 6-8 Mt negative impact of Tropical Cyclone Veronica.Production guidance for the rest segments – petroleum (at 113-118 MMboe), copper (at 1645-1740 kt), metallurgical coal (at 43-46 Mt) and energy coal (at 28-29 Mt) remains unchanged.

Stock Recommendation:At the current market price of $38.330, the stock is trading slightly towards its upper band of 52 week high/low which is $40.130/$28.544.

Looking at the price to book multiple, the stock is trading at 2.6x which is quite higher as compared to “Metals & Mining” Industry Median of 1.4x.

At the current level, market capitalization for the stock stands at ~$112.62 billion with an annual dividend yield at 4.36%.The stock has appreciated 32.60% in last one-year and 15.46% in the past three-months. Hence considering the aforesaid parameters, valuations and price performance, we maintain our “Hold” recommendation on the stock at the current levels (up 0.262% on 23 April 2019).

Fortescue Metals Group Limited

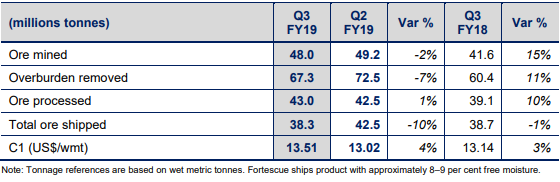

Total Ore Shipped Saw a De-Growth Of 10%:Fortescue Metals Group Limited (ASX: FMG) recently came out with the quarterly production report for March 2019 mentioning that company delivered shipments of 38.3mt in Q3 FY19 which is down 10% on q-o-q basis while Ore mined and overburden removed increased by 15% and 11%, respectively reflecting that inventory has been maintained and product mix has been improved. Cash on the balance sheet stood at US$1.1 billion with gross debt at US$4.0 billion and net debt at US$2.9 billion as on March 2019.

Production Summary for Q3FY19 (Source: Company Reports)

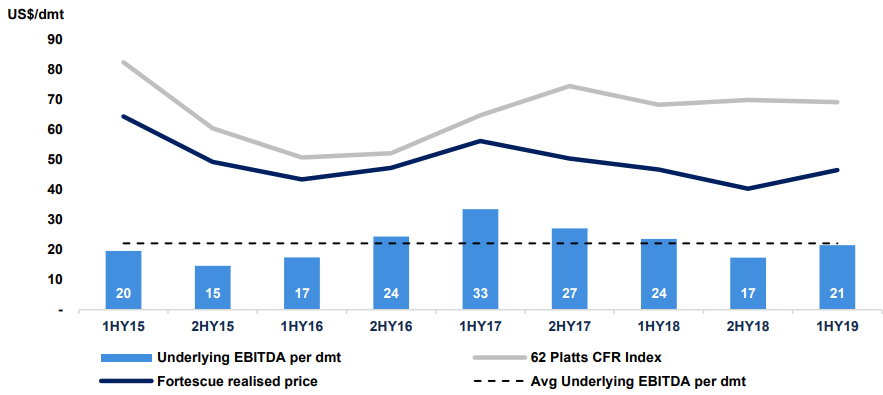

Financial Performance in 1HFY19: Revenue for the group dipped 4% (pcp basis) to US$3,540 million in 1H19.There was a growth of 10% in the revenues in 1H FY 2019 as compared to 2H FY18 on account of higher average realised iron ore price to US$47/dmt against US$40/dmt in 2H18.

Underlying EBITDA margin chart (Source: Company Reports)

What to Expect: Theprogress at Eliwana Mine and Rail development Project is on schedule and budget. The Eliwana development, which was announced in May 2018, is on track to deliver first ore in December 2020. FMG has applied for 25 tenements across 7,000 km in Portugal which are expected to progress to grant later in 2019.

Stock Recommendation: Analysing the valuation parameters, the stock is trading at price to book value of 1.6x, slightly higher as compared to 1.4x of its industry median. At CMP of $7.740, the stock is available at P/E of 18.920x with market capitalisation at $23.03 billion and the annual dividend yield of FMG stood at 4.14%.

The stock has performed well throughout the year with one-year gain of 67.28%. The stock has witnessed a substantial gain of 91.71% in the last 6-months. At the current level, the stock is trading slightly towards 52-week high level of $8.240.

Considering the higher valuations supported by fundamental strength and looking at current trading level, we give a “Hold” recommendation on the stock at the current market price of $7.740 (up 3.476% on 23 April 2019).

Rio Tinto Limited

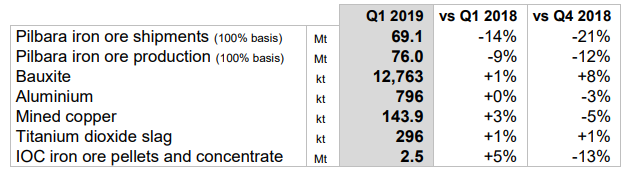

Lower production Activity Seen in 1Q FY19:Rio Tinto Limited (ASX: RIO) announced that Group executive Joanne Farrell will leave the company at the end of September 2019 after completing nearly 32 years with Rio Tinto.

The company released production results for the first quarter of FY19. Pilbara iron ore shipments of 69.1 Mt (100% basis) in 1Q FY19 was down by 14% as compared to 1QFY18 and down 21% against 4Q FY18. The lower production on the YoY basis can largely be attributed to weather disruptions in March and a fire at Cape Lambert A in the month of January. The cascading effect of these events is expected to be visible in second quarter performance.

Production Results for 1Q FY19 (Source: Company Reports)

Financial Performance in FY18:In 2018, the company delivered the underlying earnings amounting to $8.8 billion. Despite some volatility, the commodity prices were broadly supportive during the year, but growth in the end-markets was relatively subdued and inflationary pressures increased in some of the product groups. Thecompany reduced its net debt level by $4.1 billion from $3.8 billion to net cash of $0.3 billion as net cash generated from operating activities and disposal proceeds exceeded capex and cash returns to shareholders.

What to Expect:The management has revised its guidance for FY19 for Pilbara shipments to 333-343 Mt from earlier 338-350 Mt (100% basis), considering the weather and other disruption. Rio Tinto’s Pilbara unit cost guidance in 2019 stood at $13 - $14 per tonne.

Stock Recommendation: Looking at the valuations, the stock is trading at price to book value of 2.3x, higher as compared to its industry median of 1.4x. At CMP of $99.210, the stock is trading close to its 52-week high of $102.830. Annual dividend yield for the stock stands at 4.31% with the market cap at ~$36.28 billion at current level. In the past three months, the stock rose 25.59%. Hence considering the lower guidance by management, higher valuation along with the sharp run-up seen in short term period of 3-months, we give an “Expensive” rating on the stock at current market price of $99.210 (up 1.504% on 23 April 2019).

BlueScope Steel Limited

BSL posted Strong Half-Yearly results for FY19: BlueScope Steel Limited (ASX: BSL) announced that NS BlueScope Malaysia has completed the acquisition of YKGI Holdings Berhad’s manufacturing facility in Klang, Malaysia. The acquisition happens to be consistent with BlueScope’s strategy to grow its coated and painted steel business as well as provides a cost-effective source of cold rolled feed to supply to NS BlueScope Malaysia.

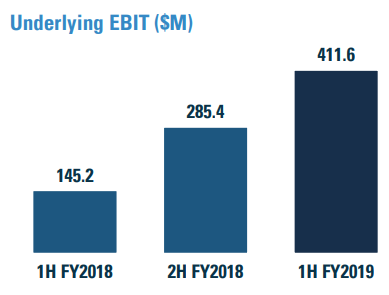

Financial Performance in 1H FY19: BlueScope reported NPAT of $624.3 million for 1H FY2019 posting a growth of 42% on the pcp basis. The underlying EBIT for the period came in at $849.6 million, up 62% (pcp). Excellent performance in terms of financials was driven by strong demand and steel spreads in U.S. and Australasian markets. Balance sheet remains healthy with net cash position at $127.5 million as on 31 December 2018. The company targets of $200-400 million of net cash, going forward.

Underlying EBIT (Source: Company Reports)

Buy-Back Update: As per its 3 December 2017 buyback scheme, the group has bought back a total of 94,11,133 shares via on-market trade for the total consideration of A$12,33,41,788.45 till 16 April 2019. The group intends to buy back remaining shares with an aggregate consideration up to A$126,658,211.55.

What to Expect: Thecompany had announced the possible expansion of North Star business for which estimated cost is in the range of US$600-700 million. The management expects underlying EBIT for FY19 to grow by 10%.The second half of FY2019 is expected to be benign than the first half of FY2019 due to uncertainty of FX, market conditions and softer global commodity steel prices relative to the iron ore and coking coal costs.

Stock Recommendation:Considering the price to book value, the stock is trading at 1.1x, lower to its industry median of 1.4x which suggests the stock is undervalued at the current juncture. ROE for the stock at 9.6% (in 1H FY19) which is significantly higher than the industry median of 6.4%.At the current market price of $14.100, the stock is available at P/E of 4.380x, significantly lower as compared to its peers like S32 (South32 Limited), KLA (Kirkland Lake Gold Ltd), AWC (Alumina Limited) as well as EVN (Evolution Mining Limited) of 8.91x, 24.09x, 7.54x, and 23.67x, respectively.

Considering the aforesaid factors, robust financials, and valuations to support the current level of the stock, we, therefore, recommend a “Buy” rating on the stock at the current market price of $14.100 per share (up by 1.148%).

.PNG)

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...