Stocks’ Details

JB Hi-Fi Limited

Sales of H1FY20 up by 3.9%:JB Hi-Fi Limited (ASX: JBH) is engaged in the retail of home consumer products, including consumer electronics, software, appliances, etc. The company recently announced that Greg Richards will be stepping down from the position of Chairman and Non-Executive Director on 30th June 2020. Stephen Goddard, who holds more than 30 years of relevant experience, will be replacing him as the Chairman of the Board.

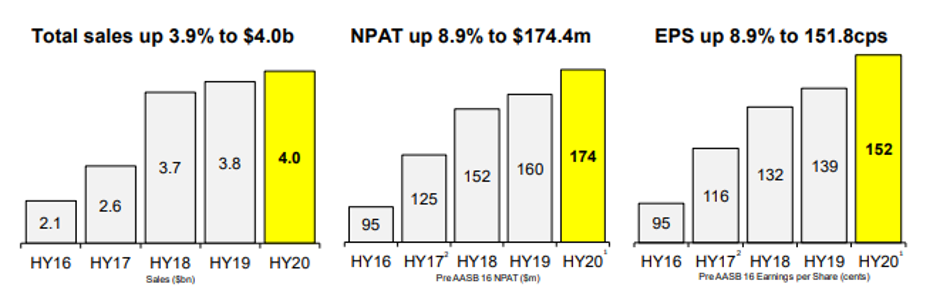

Half-Yearly Highlights: During the half-year ended 31st December 2019, the company reported total sales amounting to $4.0 billion, up 3.9% on pcp, backed by positive comparable sales growth across all divisions. NPAT for the half came in at $174.4 million, up 8.9% on pcp. The company reported an increase of 8.8% in interim dividends, at 99 cents per share. The momentum continued through January 2020, with JB Hi-Fi Australia and The Good Guys reporting sales growth of 6.5% and 1.4%, respectively, on the prior corresponding period. JB Hi-Fi New Zealand sales went down by 1.6%, as compared to a decline of 1.8% in the prior corresponding month.

H1FY20 Key Metrics (Source: Company Reports)

Outlook: Total sales for FY20 are expected to be ~$7.33 billion. NPAT for the year is expected to be in the range of $265 million - $270 million, representing growth in the range of 6.1% - 8.1% on pcp.

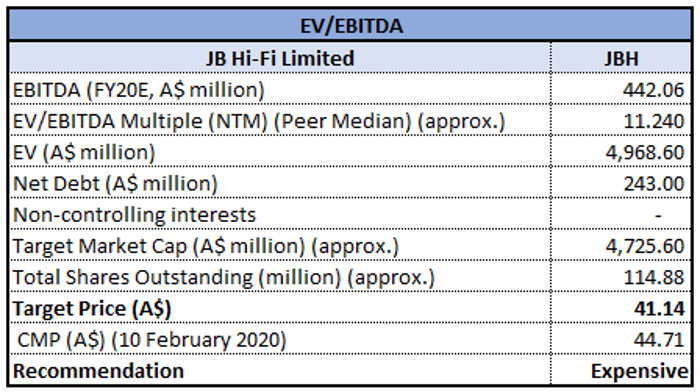

Valuation Methodology: EV/EBITDA Multiple Approach

EV/EBITDA Based Valuation (Source: Thomson Reuters)

Stock Recommendation: The stock of the company generated positive returns of 75.72% over a period of 1 year and is currently trading very close to its 52-week high of $46.090. The company reported record sales and earnings in the first half and is optimistic about growth in the future, with positive results reported in January 2020. We have valued the stock using EV/EBITDA based relative valuation method and for the purpose, have taken the peer group - Harvey Norman Holdings Ltd (ASX: HVN), Metcash Ltd (ASX: MTS), Wesfarmers Ltd (ASX: WES), etc. As a result, we have arrived at a correction of higher single-digit (in % terms). Hence, we give an “Expensive” recommendation on the stock at the current market price of $44.710, up 11.496% on 10th February 2020, owing to the release of half-yearly results.

Sigma Healthcare Limited

Project Pivot Progressing Well:Sigma Healthcare Limited (ASX: SIG) is engaged in the wholesale and distribution of pharmaceutical products. The company recently updated the market that Underlying EBITDA for FY20 is expected to be in the range of ~$46 – 47 million and $57-58 million after including the benefit arising out of the new accounting standard AASB 16 Leases. However, the company is anticipating insufficient franking credits for the fully franked final dividend for FY20, pursuant to the effect of the costs for transforming the business. As per another recent update, the company appointed Michael Sammells as an Independent Non-Executive Director on the Board.

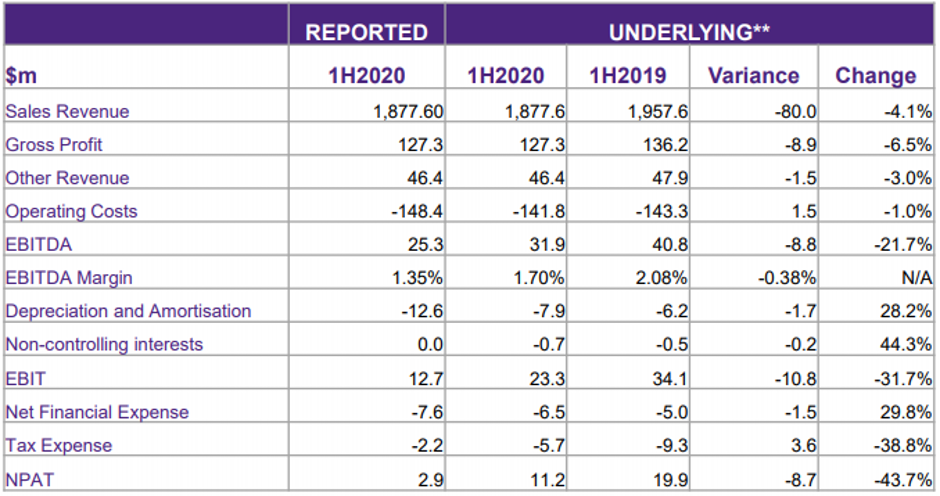

Half-Yearly Highlights: During the half-year ended 31st July 2019, reported EBITDA came in at $25.3 million, down 19.8% on the prior corresponding period, impacted by one-off restructuring costs. The company’s pharmacy brands reported like-for-like growth of 7.8% and its hospitals witnessed revenue growth of 23%. The company has undertaken a business transformation program, Project Pivot, which has resulted in a substantial decline in annualised costs of the business, which will benefit the company in 2HFY20 and beyond.

Financial Performance (Source: Company Reports)

What to Expect: The company will be releasing the results for FY20 on 25th March 2020, wherein it will be informing the market on its expectations for FY21. As far as the underlying performance of the business is concerned, the company has been performing strongly and expects accelerated underlying earnings growth in the core business in FY21.

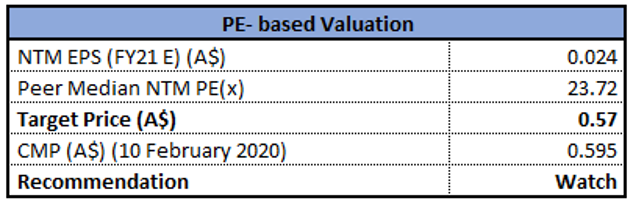

Valuation Methodology: P/E Multiple Approach

P/E Based Valuation (Source: Thomson Reuters)

Stock Recommendation:The stock of the company gave negative returns of 9.85% over a period of 3 months. The company has been delivering well on its transformation program and expects to achieve the targeted efficiency gains of over $100 million. We have valued the stock using Price to Earnings based relative valuation method and for the purpose, have taken the peer group - Sonic Healthcare Ltd (ASX: SHL), Healius Ltd (ASX: HLS), Ramsay Health Care Ltd (ASX: RHC), etc. As a result, we have arrived at a correction of lower single-digit (in % terms). Hence, we have a watch stance on the stock at the current market price of $0.595 as on 10th February 2020.

Boral Limited

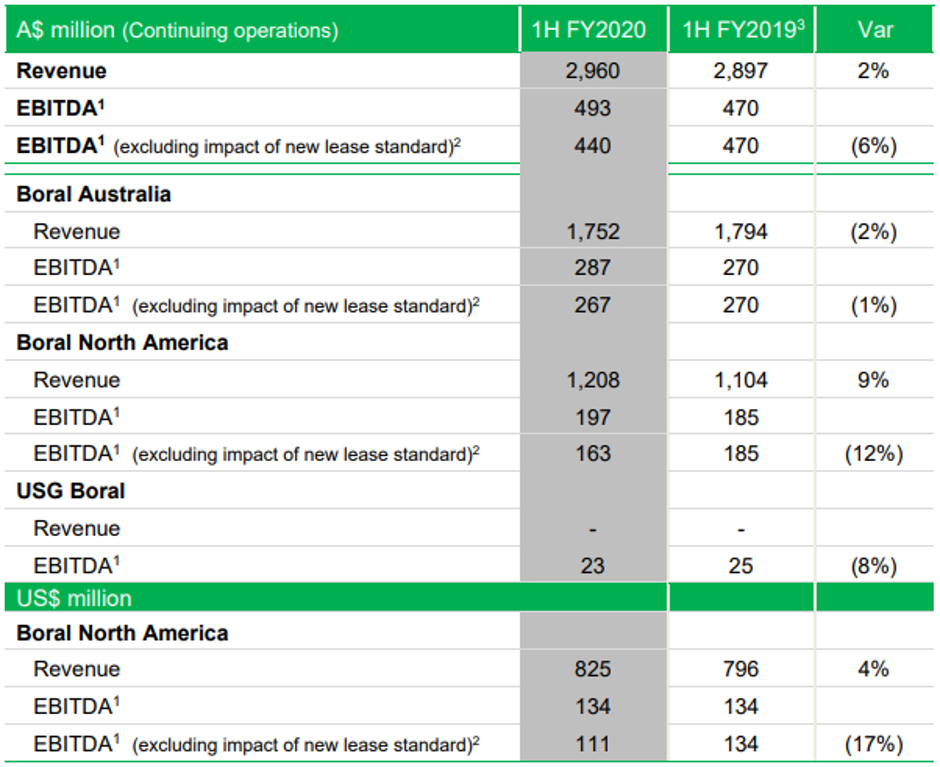

Update on North American Windows business:Boral Limited (ASX: BLD) is engaged in the manufacturing and supply of building and construction materials. The company recently announced a dividend amounting to $0.095 per ordinary share, to be paid on 15th April 2020.

Business Update: As per another recent announcement, the company informed that it has noticed certain irregularities with respect to inventory levels and raw material and labour costs, in relation to its North American Windows business. It was noted that the financial accounts were manipulated by the finance personnel to increase the overall profitability of the business. In response to the above, the company has put in place various mechanisms to avoid any such event, going forward.

First Half Results: During the first half ended 31st December 2019, the company reported NPAT amounting to $156 million. Revenue for the period came in at $2,960 million, up 2% on prior corresponding period revenue of $2,897 million.

Divisional and Group Results (Source: Company Reports)

Outlook: The company expects FY20 EBITDA to be lesser than that reported in FY19 across all divisions, as a result of bushfire and weather impact and lower earnings from the Windows business. NPAT for FY20 is expected in the range of $320 million - $340 million, as compared to the restated NPAT of $420 million in FY19. The company is looking forward to divesting its non-core assets and expects the sale of the Midland Brick business to be completed in 2HFY20.

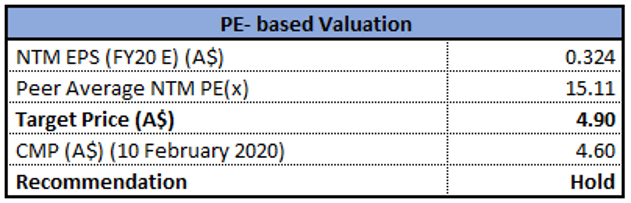

Valuation Methodology: P/E Multiple Approach

P/E Based Valuation (Source: Thomson Reuters)

Stock Recommendation: The stock of the company gave positive YTD returns of 14.44% and is currently trading below the average of its 52-week trading range of $3.930 - $5.735. We have valued the stock using Price to Earnings based relative valuation method and for the purpose, have taken the peer group - CSR Ltd (ASX: CSR), Fletcher Building Ltd (ASX: FBU) and Austin Engineering Ltd (ASX: ANG). As a result, we have arrived at a target price offering an upside of lower single-digit (in % terms). Considering the corrective measures taken for the Windows business and anticipated results thereon, performance during the first half, and valuation, we give a “Hold” recommendation on the stock at the current market price of $4.600, down 10.68% on 10th February 2020 after the release of business update.

Aurizon Holdings Limited

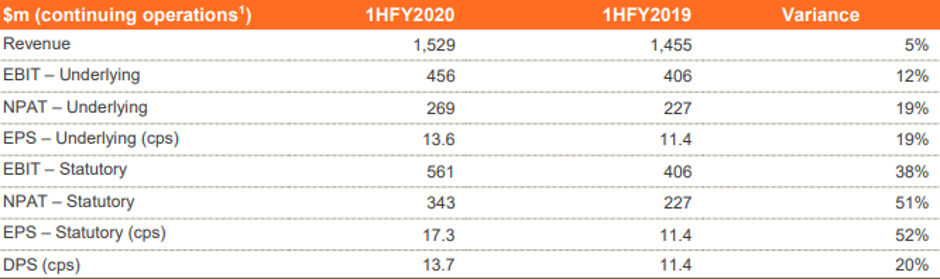

Strong Operational Performance in 1HFY20:Aurizon Holdings Limited (ASX: AZJ) is engaged in maintenance and renewal of network assets, transport of coal and bulk mineral commodities, etc.

Half Yearly Performance:During the six months ended 31st December 2019, the company reported underlying EBIT amounting to $456 million, representing an increase of 12% on the prior corresponding period. Revenue went up by 5% to $1,529 million. Statutory NPAT went up by 51%, as a result of profit on the sale of Aurizon’s Rail Grinding business. The Board declared an interim dividend of 13.7 cents per share, payable on 23rd March 2020.

Financial Highlights (Source: Company Reports)

Outlook: FY20 Underlying EBIT is expected to be between $880 million - $930 million.

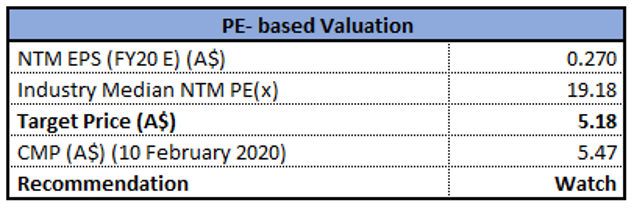

Valuation Methodology: P/E Multiple Approach

P/E Based Valuation (Source: Thomson Reuters)

Stock Recommendation: The stock of the company gave negative returns of 7.79% over a period of 3 months.Currently, the stock is trading above the average of its 52-week trading range of $4.340 - $6.100. Going forward, the company expects operational efficiency improvements to drive performance. The company signed two new contracts in the coal business and delivered strong progress against its strategy. We have valued the stock using Price to Earnings based relative valuation method and have arrived at a correction of single-digit (in % terms). Hence, we have a watch stance on the stock at the current market price of $5.470, up 2.627% on 10th February 2020.

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...