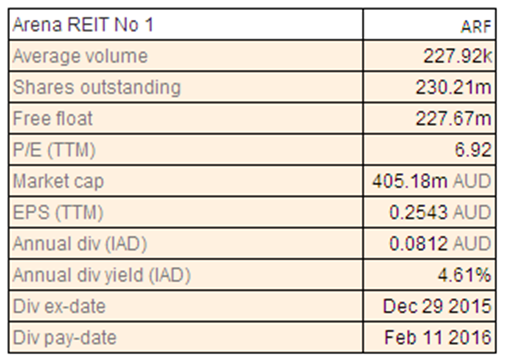

Arena REIT No. 1

ARF Dividend Details

Positive property revaluations results: Arena REIT No. 1 (ASX: ARF) recently reported an increase in its net revaluation of its property portfolio by over $30 million, indicating the group’s high quality assets as well as its lucrative lease term with quality tenants and security arrangements. ARF delivered a revaluation rise by 7.1% in its portfolio as of December 30, 2015, resulting to over 10% or 13 cents in net asset value per ARF security from June 2015. Consequently the group’s gearing is forecasted to decrease to over 27%. Arena’s independent valuations of 35 childcare centers and seven medical Centre assets, which accounts over 34% of the group’s value delivered an increase of the revaluations as of Dec 30 2015, contributed to the overall increase.

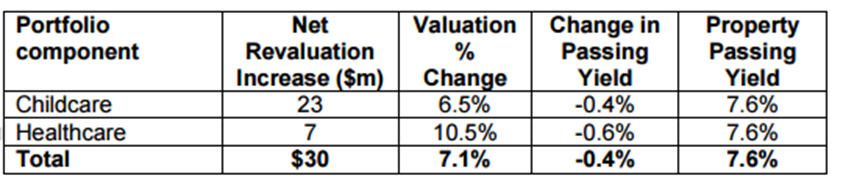

Property revaluations performance (Source: Company Reports)

Accordingly, the independent valuations rose by an average 8.8% for the group’s Childcare Centre portfolio leading to an average of 6.5% rise above the book value. As per the healthcare portfolio, the independent valuations indicated an average net rise of 10.5% in December 30, 2015 against the June 2015 book value. With the stock surging by 14.5% in the last six months (as of January 13, 2016), we believe ARF has the potential to rise further and accordingly place a “BUY” at the current price of $1.725

ARF Daily Chart (Source: Thomson Reuters)

Finbar Group Ltd

.png)

FRI Dividend Details

Ongoing expansion of its project pipeline: Finbar Group Ltd (ASX: FRI) got the development approval for its East Perth JV project which has 247 apartments and five commercial lots. The group would get 50% of the project profit coupled with management fee, with a forecasted project end value of $162 million. FRI intends to start marketing this year for the project. Meanwhile, FRI has been building a strong assets base and delivered a presales of over $407.7 million in 2015 adding to its >$2 billion project pipeline. The group finished the Arbor North JV project which has 154 one and two bedroom apartments and already received $54.9 million in sales from the $75.6 million project. Management estimates these revenues to be reflected in its first half of 2016 results.

On the other hand, FRI stock corrected over 23% in the last year (as of January 13, 2016) due to weak market conditions and group’s performance. But, FRI is trading at very cheaper valuations with a low P/E and has an outstanding dividend yield. We believe that the group’s strong project pipeline coupled with its ongoing buyback program would drive the stock further. Based on the foregoing, we give a “BUY” recommendation on the stock at the current price of $1.01

.png)

FRI Daily Chart (Source: Thomson Reuters)

BWP Trust

.png)

BWP Dividend Details

Expensive Valuations: BWP Trust (ASX: BWP) delivered $176 million improvement of its portfolio value to 2.158 billion, which is a 8.9 % increase as of half year ending on December 2015 against June 2015, leading to a further 26.6 cents per unit asset backing. The portfolio weighted average capitalization rate is forecasted to reduce to 6.81% in half year ended in December 2015 against 7.33% in June 2015 as varying lease terms in assets led to higher rates as compared to the new standalone properties rate. Meanwhile, the group also recently reported that they expected a distribution of 8.2 cents per unit.

As a result, BWP stock surged over 4% in the last three months (as of January 13, 2016). On the other hand, we believe that this is a short term rally and with the ongoing slowdown the group would continue to be under pressure in the coming months. We believe BWP is trading at “Expensive” levels.

.png)

BWP Daily Chart (Source: Thomson Reuters)

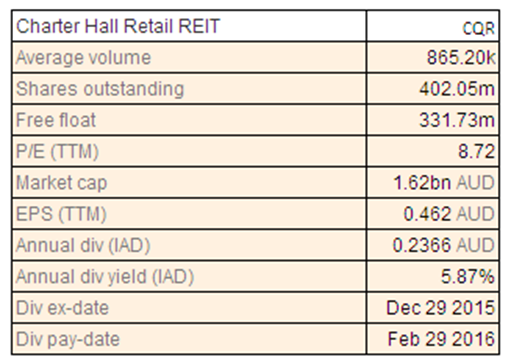

Charter Hall Retail REIT

CQR Dividend Details

Focusing on acquisitions: Charter Hall Retail REIT (ASX: CQR) is improving its portfolio via acquisitions and divestment to maintain its growth track. The group acquired four supermarkets for $192.0 million at an average yield of 7.2%, which were funded from the proceeds of its sale of non-core retail properties while a $50 million was funded from the institutional placement finished by the group in August 2015. The group is also focusing on redevelopments and accordingly finished two major redevelopments at Caboolture Square in Queensland and Lansell Square in Victoria leading to a better consumer shopping experience. On the other hand, the ongoing challenging market condition is impacting the group’s performance, which managed to deliver just 0.7% increase in its FY15 full year distribution to 27.50 cents per unit against FY14.

We believe the stock might face challenge to deliver positive performance in the coming months. Accordingly we place an “Expensive” recommendation on this dividend yield stock at the current price of $4.02

CQR Daily Chart (Source: Thomson Reuters)

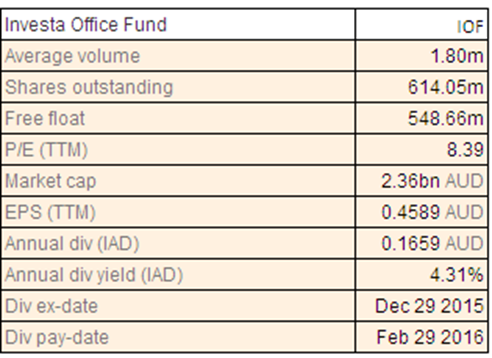

Investa Office Fund

IOF Dividend Details

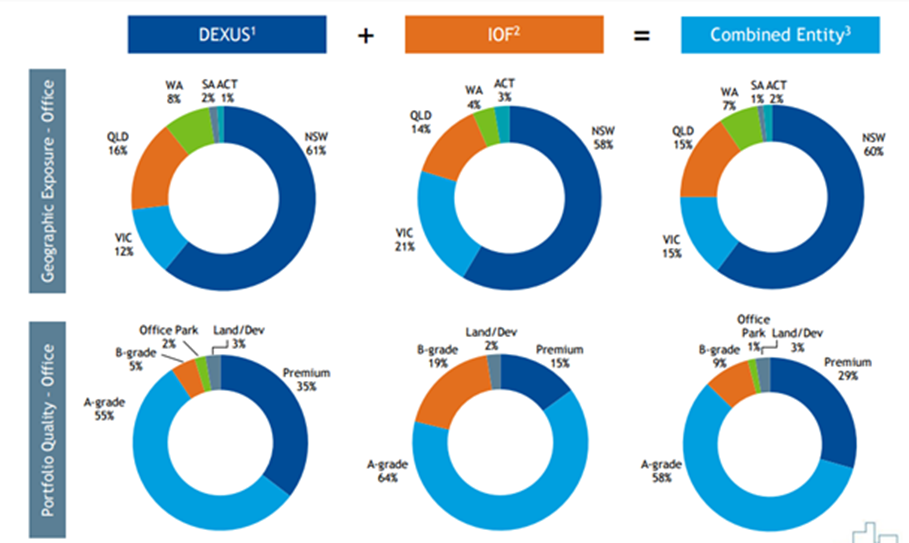

Made an implementation agreement with Dexus Property Group: Investa Office Fund (ASX: IOF) made an Implementation Agreement with Dexus Property Group leading to an Implied equity value of $2.5 billion and enterprise value of $3.5 billion. The combined portfolio would lead to over 66 properties with IOF contributing over 22 and Dexus contributing over 44.

Combined entity value (Source: Company Reports)

Meanwhile, IOF stock managed to deliver over 5.2% in the last 52 weeks driven by its Dexus agreement and performance.

On the other hand, the stock has been correcting over the four weeks by 3.3% (as at January 13, 2016) and we believe IOF is trading at higher valuations and place an “Expensive” recommendation on this dividend yield stock.

IOF Daily Chart (Source: Thomson Reuters)

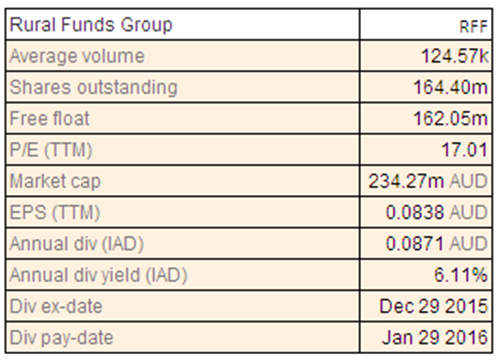

Rural Funds Group

RFF Dividend Details

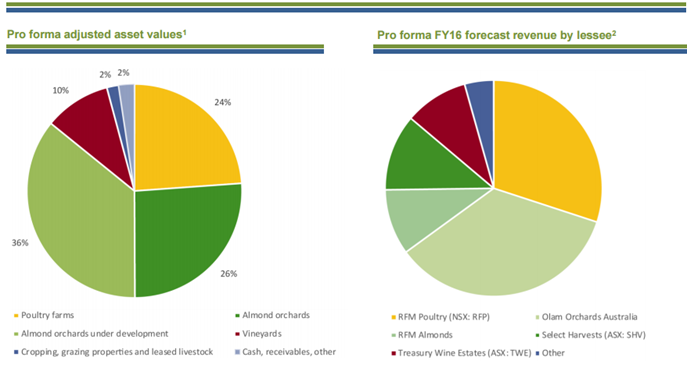

Built a diversified agriculture portfolio: Rural Funds Group (ASX: RFF) shares rallied over 35.75% in the last six months (as of January 13, 2016) driven by its diversified agricultural portfolio which offset the seasonal impacts. The group built a diversified portfolio with 29 properties which includes poultry farms, almond orchards and vineyard, as well as strong tenants with long weighted average lease expiry. Accordingly, its agricultural assets has an adjusted total asset value of $262 million (based on FY15 annual report) and a weighted average term of 12.2 years, leading to an investment yield of 7.8%, as per the year-end unit price of $1.10 during FY15.

Diversified assets and counterparts (Source: Company Reports)

RFF even acquired Tocabil Station at Hillston, NSW and entered into a 22 year lease agreement with Olam Orchards Australia. Moreover, the development of a 600 hectare almond orchard by Olam on Tocabil would enhance $5.2 million mixed farm into a $32.1 million almond, cropping and grazing asset. Meanwhile, RFF also has a solid dividend yield and management even reported a better distribution growth estimates to 4% per annum in FY16, as compared to earlier 3% per annum estimates. We recommend a “HOLD” on RFF at the current stock price of $1.43

RFF Daily Chart (Source: Thomson Reuters)

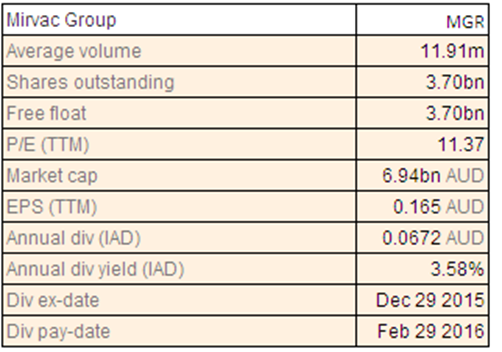

Mirvac Group

MGR Dividend Details

Higher valuations: The shares of Mirvac Group (ASX: MGR) rallied over 11.5% in the last three months (as at January 13, 2016) driven by its ongoing property acquisitions and developments which would contribute to its long term performance. The group entered into a JV with Ping An Real Estate for developing residential projects in major Australia cities. The first project in this joint venture is The Finery which is Mirvac’s apartment development in Waterloo. The group also made a long term agreement for lease with Westpac till 2030 starting from 2018 for its 275 Kent Street in Sydney.

MGR was also chosen as the asset manager of Investa Property, a subsidiary of China Investment Corporation, indicating the group’s expertise while Mirvac would invest $25 million in the CIC controlled trusts managed by them. On the other hand, we believe these agreements would although contribute to the long term performance of MGR, the stock might still be under pressure in the coming months given the volatile economic conditions in Australia. Based on the foregoing, we give an “Expensive” recommendation at the current price of $1.88

MGR Daily Chart (Source: Thomson Reuters)

Stockland Corporation Ltd

SGP Dividend Details

Better rentals coupled with strict portfolio’s weighted average capitalization rate drove the property revaluations performance: Stockland Corporation Ltd (ASX: SGP) reported that their commercial property portfolio rose by over $430 million driven by better rental growth and weighted average capitalization rate for portfolio decreased to 6.5% in half year ending at December 2015 as compared to 6.9% ending at June 2015. Meanwhile, the group even reported that it had forecast its distribution of 12.20 cents per ordinary Stapled Security for half year ending at December 2015, and is on track to deliver a 24.5 cents per security for FY16. Moreover, SGP stock is trading at relatively attractive P/E and has a good dividend yield.

With the stock raising by over 9.5% in the last three months (as at January 13, 2016), we believe the positive momentum to continue and accordingly suggest a “BUY” at the current price of $4.09

SGP Daily Chart (Source: Thomson Reuters)

Cedar Woods Properties Ltd

.png)

CWP Dividend Details

Strengthening its South-East Queensland penetration: Cedar Woods Properties Ltd (ASX: CWP) acquired a 3.81 hectare infill site in Wooloowin, in Brisbane’s inner north for $24.6 million to further boost its presence in South-East Queensland. CWP has been building a strong pipeline of assets and even got the approval from Queensland Government for developing 480 lots. Therefore, to position itself with strong funds the group even extended its three-year, $135 million bank facility till November 2018. Although CWP stock plunged over 19.5% in the last six months due to weak investor’s sentiment on Western Australia exposed firms, the stock rallied over 3.8% in the last four weeks (as at January 13, 2016) given the recovering residential property market in Western Australia, Victoria and Queensland. Moreover, the stock is trading at cheaper valuations with low P/E while has a strong dividend yield.

Accordingly, we give a “BUY” recommendation on the stock at the current price of $4.12

CWP Daily Chart (Source: Thomson Reuters)

Scentre Group

.png)

SCG Dividend Details

Efforts to enhance its capital position: Scentre Group Ltd (ASX: SCG) recently reported that it would be offloading three shopping centers (Westfield Glenfield, Westfield Queensgate and Westfield Chartwell) in New Zealand, enabling the group with gross proceeds of NZ$549 million. With this move, SCG would be able to improve its capital position and aim for potential growth. Meanwhile, the group also delivered a decent third quarter performance, with its specialty sales rising by 5.4% year on year in the third quarter. SCG also has a strong pipeline of > $3 billion and improved its releasing spreads which were down 2.5% as compared to releasing spreads decrease by 4.2% in prior corresponding period.

Scentre Group had forecast its comparable NOI growth in the range of 2% to 2.5% for the year ended on 31 December 2015. With the stock trading at a decent P/E and a dividend yield, we recommend a “HOLD” on this stock at the current price of $4.15

SCG Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2016 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

AU

AU

Please wait processing your request...

Please wait processing your request...