Telstra Corporation Ltd

.png)

TLS Dividend Details

Growth via mobile segment: Telstra Corporation Ltd (ASX: TLS) mobile services continued to deliver strong performance with revenue rise of 7.2% in FY15 which is the highest growth rate in three years. Postpaid handheld revenue was boosted by 1.6% SIO increase coupled with 4.4% ARPU increase. Higher data usage drove ARPU by 6.7%, while unique users rose by 3.5% leading to a better prepaid handheld revenue. M2M performance remains strong driven by transport and banking sectors. On the other hand, the group bottom line continued to witness pressure, wherein EBITDA and net profit after tax declined by 3.5% yoy to 5.8% yoy to $10.7 billion and $4.3 billion, respectively, in FY15. Telstra reported that it’s handheld, mobile broadband and M2M businesses performance rate decreased in second half of 2015 against first half while postpaid handheld growth also slowed on the back of decrease in excess data rates and higher data allowances. Telstra’s Retail mobile customer growth reached 664,000 during FY15 wherein second half customers reached 298,000 while first half of 2015 customers reached 366,000.

.png)

Telstra Corporation mobile division performance (Source: Company Reports)

Moreover, the pressure from the consolidation of the smaller players might affect Telstra’s growth prospects in the coming months. Management also estimates a low single EBITDA growth in FY16. The shares of Telstra declined over 16.20% in the last six months (as at January 20, 2016) and the negative sentiment is expected to continue in the coming months. Based on the foregoing, we place an “Expensive” recommendation on this stock at the current price OF $5.52

TLS Daily Chart (Source: Thomson Reuters)

Wesfarmers Ltd

.png)

WES Dividend Details

Offshore acquisition to drive growth: Wesfarmers Ltd (ASX: WES) updated about its agreement to acquire 100% of the Home Retail Group plc holding in Homebase for $705 million. The offer is unanimously supported by the Home Retail Group, Board, which provides execution certainty and attractive cash consideration for the shareholders. The completion of the transaction is conditional on approval of the shareholders and its banking syndicate and the acquisition is expected to be completed by the end of the first quarter of calendar year 2016.

.png)

Homebase Sales and EBIT (Source: Company Reports)

This is expected to deliver an established and scalable platform with stores that are the right size for the UK market and support warehousing merchandising in a low-cost operating model. The acquisition seems to present a solid platform for growth but we consider that the stock is expensive at the current stock market price of $41.15

WES Daily Chart (Source: Thomson Reuters)

Patties Foods Ltd

.png)

PFL Dividend Details

Exit from the frozen food business: Patties Foods Ltd (ASX: PFL) announced that it has signed a sales agreement with Entyce Food Ingredients Pty Ltd in respect of the Creative Gourmet frozen food business subject to a number of customary conditions. The business was acquired in 2007 and has been delivering a range of market leading frozen berry products to supermarkets. The sale will help the company to invest time and resources on its profitable savoury business (accounting for more than 90% of the company’s sales and EBIT) and will be a part of the refreshed strategic growth roadmap which aims at delivering profitable growth for shareholders. Following the sale, the company will also undertake a managed exit of the Nanna’s brand of frozen fruit products which will continue to focus on sweet dessert and apple pie pastry. However, we believe that the current price over values the stock and we would therefore consider the stock to be expensive.

Onevue Holdings Ltd

.png)

OVH Details

Support for Share purchase plan: Onevue Holdings Ltd (ASX: OVH) announced that the recent Share Purchase Plan 2016 resulted in $6.38 million in applications exceeding the $2.5m original offer. With the share placement to institutional investors, the retail support through the SPP has been maximised. The Company board supported a 100% increase from $2.5m to $5.0m being accepted into the SPP. A scale back of applications has been planned in order to return the excess received over $5m ($1.38m). The company now intends to support the working capital requirements with regards to steps such as delivery of the Fund Services transitions pipeline, strengthen balance sheet, and repay about $1.5million of the ANZ debt facility from the capital raised from the SPP and the Private Placement totalling $17.5m (before costs). The Company demonstrated a 92% growth in total revenue. We still believe that the stock is expensive at the current market price.

Euroz Ltd

.png)

EZL Dividend Details

Transition phase over: Euroz Ltd (ASX: EZL), a diversified wealth management company with interests in stock broking and corporate finance, funds management and wealth management, has reflected paying dividends in excess of $ 175 million fully franked during the past 15 years. The company recorded a headline loss of $ 7.1 million for the year ended 30 June 2015, after taking into account an after tax decrease of $ 15 million in the market value of investments.

NPAT and Dividends (Source: Company Reports)

The past year has been a period of transition in which the foundations have been laid for future growth and a series of major goals to secure the future direction have been achieved. These include successful cultural and financial integration of Blackswan Equities boosting the private client dealing team and kick-starting wealth management ambitions. The establishment of Prodigy Investment Partners is a solid standard platform for future boutique fund partnerships and the first of these Flinders Investment Partners has been launched. The company has remained moderately profitable in the early months of the new financial year. Taking the performance for the first few months of the current year, we believe that the stock is overpriced and expensive at the current stock prices.

MNF Group Ltd

.png) TNZI contributing to performance

TNZI contributing to performance: MNF Group Ltd.’s (ASX: MNF) FY 2015 results depicted a 44% increase in revenue to $ 85.7, a 31% increase in gross profit to $ 31.8 million, and 35% increase in EBITDA to $ 12.2 million with an EBITDA margin of 14.2% compared to 15.2% in the previous year. The profit after tax grew by 24% to $ 7.2 million and EPS was 11.49 cents per share, compared to 9.26 cents per share in the previous year. The dividend per share fully franked was 5.75 cents per share, compared to 4.50 cents per share, a growth of 28%. The full year EBITDA was 9% ahead of the original guidance for FY 2015 and include three-month contribution from TNZI. The underlying result includes acquisition costs of $ 0.3 million for the transaction and the decrease in EBITDA margin is due to the weight of TNZI contribution at lower margin. Capital expenditure in FY 2015 was higher than the historical figure due to the re-engineering the domestic interconnect network. Future Expenditure for domestic business is expected to return to historical levels and the figure for the expansion of TNZI is expected to be around $ 5 million in FY 2016. At the current prevailing stock price, we consider the stock to be expensive and do not recommend an investment at the moment.

Vocus Communications Ltd

.png)

VOC Dividend Details

Strong penetration in domestic Australia and New Zealand division: Vocus Communications Ltd (ASX: VOC) continued to expand its penetration through fiber network and data center in Australia and New Zealand. VOC rose its Australian metro fiber network to 760km while over 4,200km in New Zealand added on completion of FX Networks acquisition. VOC has over 15 data center facilities spread across 11 locations with a total area of 5,788 square meters and started a new flagship data center in Melbourne CBD while extending its Auckland data center by state of the art facility. The group bought rights to 10% of the SE-ME-WE 3 cable connecting Perth to Singapore, to increase its international connectivity through the West coast. Meanwhile, VOC reported revenue and underlying EBITDA rise by 62% and 56% to $149.8 million and $51.6 million, respectively, during fiscal year of 2015. Moreover, the group and M2 Group entered into a Merger Implementation Agreement and accordingly VOC stock surged over 21.33% (as of January 20, 2016) in the last six months.

On the other hand, the surge in the stock placed VOC at unreasonable valuations which is trading at a relatively higher P/E. The group also has a very low dividend yield. We give an “Expensive” recommendation on the stock at the current price.

VOC Daily Chart (Source: Thomson Reuters)

China Integrated Media Corporation Ltd

.png)

CIK Details

Growing focus on advertising in glasses free 3-D display business:China Integrated Media Corporation Ltd (ASX: CIK) expects to have a net profit before tax for the year ended 31 December 2015 of about A$1,800,000 to A$2,100,000 compared to loss of about A$899,508 in 2014. This result is expected to be driven by the sales of MARVEL 3DPro Super Workstations. The company announced that its newly acquired subsidiary, Marvel Digital Limited launched the MARVEL 3DPro Super Workstations which is an all in one computer workstation delivering unparalleled computing power and speed for 2-D to 3-D content conversion. The company has received several orders from customers to the value of approximately $ 3.8 million. Shipment and installation of some of these machines was expected to be complete by the end of December 2015. For the six months ended 30 June 2015, the group continued to focus on the distribution of glasses free 3-D displays and software and the provision of 3-D consultancy services. The company acquired 100% interest in Conco International Co Ltd, which is primarily engaged in audio products and the business will complement the 3-D display business unit. The group also continues to build infrastructure and operations in Hong Kong to enter the growing advertising market in China. The main focus of the group continues to be development of digital media/advertising in glasses free 3-D and continue to seek potential acquisitions which can add value. However, we believe that the stock is pricey at the current stock price and, being expensive, should be avoided at the moment.

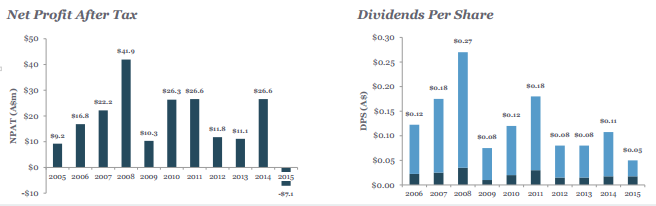

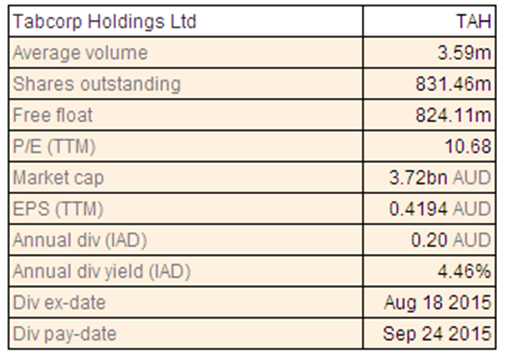

Tabcorp Holdings Ltd

TAH Dividend Details

Eying the UK Market: Tabcorp Holdings Ltd (ASX: TAH) announced that it has signed an agreement to partner with News UK to launch a new online wagering and gaming business in the UK and Irish markets to be known as Sun Bets in 2016. The new business will combine the company’s global wagering capabilities with the large customer base and market leading media assets of News UK such as The Sun newspaper and assorted sports and racing products such as Dream Team FC and Goals. The agreement is structured as a revenue sharing agreement and is subject to the company obtaining the necessary licenses and regulatory approvals and runs for an initial term of 10 years. Managing director and Chief Executive Director David Attenborough said that the UK market is an exciting opportunity worth more than AUD 7 billion and The Sun has more than 10 million readers per week and over 1 million football fans actively engaged. The deal provides the company with the opportunity to create a leading online bookmaker in the UK market.

.png)

Revenue Details (Source: Company Reports)

The company has also confirmed about potential merger with Tatts Group Ltd for which discussions have taken place. However, the companies were unable to come down to mutually acceptable terms. In FY 2015, a net profit after tax of $ 334.5 million, up 157.5% over the previous year was reported. The profit was inflated by two significant one-off income tax benefits.

The company has expanded its target dividend pay-out for FY 2016 to 90% of net profit after tax before amortisation of the Victorian Wagering and Betting Licence. However, we would not recommend an investment at the moment because we believe that the current share price makes the share expensive.

TAH Daily Chart (Source: Thomson Reuters)

Aristocrat Leisure Ltd

.png)

ALL Dividend Details

Sales driven in part by new Macau openings: Aristocrat Leisure Ltd (ASX: ALL) for the 12 months ended 30 September 2015, reported results attributable to shareholders with a profit of $ 186.4 million after-tax compared to a loss of $ 16.4 million in the previous period. The directors have authorised payment of a final dividend of 9 cents per share, compared to payment of 8 cents per share in the previous period. Total segment revenues from ordinary activities grew by 64.7% on a constant currency basis to $1.38 billion and, on a reported basis by 88.6 % to $ 1.58 billion. EBITDA grew by 101.4% to $ 441.7 million on a constant currency basis and by 138.5% to $ 523.1 million on a reported basis. Profit after tax grew by 21.5% to $ 158.2 million on a constant currency basis and 47.1% to $ 191.5 million on a reported basis.

.png)

Debt Coverage Ratios (Source: Company Reports)

Revenues increased largely due to the sustained performance of North American Gaming Operations with the acquisition of Video Gaming Technologies Inc completed in October 2014, outstanding growth in the Australian outright sales market and the strengthening of performance in Digital. Australia delivered significant market share gains. The Asia-Pacific performance improved with strong sales in new Macau openings during the period. However, we believe that the current share price overvalues the stock which is in our opinion expensive and we do not recommend a buy at this point of time.

ALL Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2016 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

AU

AU

Please wait processing your request...

Please wait processing your request...