Australia and New Zealand Banking Group Ltd

.png)

ANZ Dividend Details

Outstanding dividend yield: Australia and New Zealand Banking Group Ltd (ASX: ANZ) stock plunged over 15.17% during this year to date (as of November 27, 2015) as investors were concerned that slowdown in China would impact the group’s Asian business. Accordingly, the group’s China’s cash profit fell by 2% in International and Institutional Banking. On the other hand, the group delivered a solid Australia and New Zealand business and estimates a better performance in the coming periods. ANZ also improved its capital position and almost doubled its total assets to $890 billion to comply with APRA standards. The group recently issued $600 million worth of subordinated notes which are due in May 2026 as a part of its Australian dollar debt issuance programme.

.png)

FY15 Financial Performance (Source: Company Reports)

Moreover, management estimates a fully frank dividends in future while ANZ has solid annual dividend yield of over 6%. We note the recent internet banking outage that started mid-morning and extended into the late afternoon on November 30, 2015 following a revamp of its internet banking system. Though, the outage has elicited a chaos, it will be too early to comment on the revamped system.

From performance standpoint, the stock is trading at a very cheap P/E of about 10x relative to its peers. We maintain our “BUY” recommendation on the stock at the current levels of $27.15

ANZ Daily Chart (Source: Thomson Reuters)

BHP Billiton Ltd

.png)

BHP Dividend Details

Samarco tragic event hammering the stock investment opportunity: BHP Billiton Ltd (ASX: BHP) Samarco operations Fundao dam failed and the downstream Santarem dam has been affected leading to major damage. Further, one fatality has been reported with an additional 13 members of the workforce missing. The federal and state governments in Brazil have indicated about suing BHP Billiton and Vale for the damage caused. It is to be noted that BHP has offered instant necessary support to address the fatality and made arrangements for the cleanup and subsequently investigate the site. On the other hand, BHP stock fell over 22.88% in the last four weeks alone (as at November 27, 2015) due to the Samarco incident. Management is reviewing its iron ore production guidance for fiscal year of 2016. But investors need to note that the group has solid assets with diversified base. BHP’s share of Samarco production was 14.5 Mt in FY15 while Samarco contributes only 3% of the BHP’s underlying EBIT.

.png)

Capital and Exploration Expenditure (Source: Company Reports)

More updates on the performance so far are expected in the month of February. Further, changes in dividends, if any as speculated, may get a shielding from the recent hybrid bond issue to enable BHP deliver its interim payout to shareholders for the year.

As of now, the company has an annual dividend yield of about 9%. Accordingly, we give a “BUY” recommendation on the stock at the current price of $18.09

BHP Daily Chart (Source: Thomson Reuters)

National Australia Bank Ltd

.png)

NAB Dividend Details

Divesting non-core assets to boost cash flow: National Australia Bank (ASX: NAB) Common Equity Tier 1 ratio rose by 137 basis points to 10.2% as at September 2015, against March 2015, boosted by proceeds from rights issue. Moreover, NAB is boosting its capital position by divestments of non-core assets. NAB earlier divested Great Western Bancorp business and now confirmed the divestment of the Clydesdale Bank in the UK while proposing the initial public offering for CYBG. The group is recently seeking to partly divest its insurance operations to Nippon Life Insurance, boosting its capital position further. Moreover, NAB enhanced its asset quality during fiscal year of 2015, wherein its total charge for Bad and Doubtful Debts fell by 5% yoy to $823 million on the back of decrease in Australian Banking and UK Banking. The bank is investing over 300 million in its Wealth business for the next four years and also focusing on customer relationships.

.png)

National Australia Bank performance (Source: Company Reports)

NAB is trading at attractive valuation with a relatively cheaper P/E of about 12x and has a decent dividend yield of 6.67%. We reiterate our “BUY” recommendation on the stock at the current stock price of $29.39

NAB Daily Chart (Source: Thomson Reuters)

Telstra Corporation Ltd

.png)

TLS Dividend Details

Focusing on mobile and services as well as Asia region for growth: Telstra Corporation Ltd (ASX: TLS) shares slightly fell by 2.17% in the last four weeks (as at November 27, 2015) as Australian Competition and Consumer Commission’s demanded the firm to cut access prices by 9.4%, which TLS charges other operators who use the group’s network. The group witnessed a solid revenue growth in three years across its mobile division, which rose 10.2% year on year (yoy) to $10.65 billion in fiscal year of 2015. The group is increasing its capex to 15% of sales in the coming two years, and investing more than $5 billion on its mobile services and network in the next three years to June 2017.

.png)

Guidance (Source: Company Reports)

TLS is focusing on Network Applications and Services (NAS) portfolio as well as growth areas like Telstra Health, Telstra Media, the Telstra Software Group (TSG) and Telstra Ventures. The group is targeting Asia region for long term growth and completed the acquisition of Pacnet in April 2015 to expand its network and services in Asia. As per the latest news, TLS has uplifted its international roaming rates by about 50% under excess data rates plan for its mobile customers ahead of the Christmas. TLS is trading at a P/E of about 15x.

We believe that the stock is still expensive at the current stock price of $5.36

.png)

TLS Daily Chart (Source: Thomson Reuters)

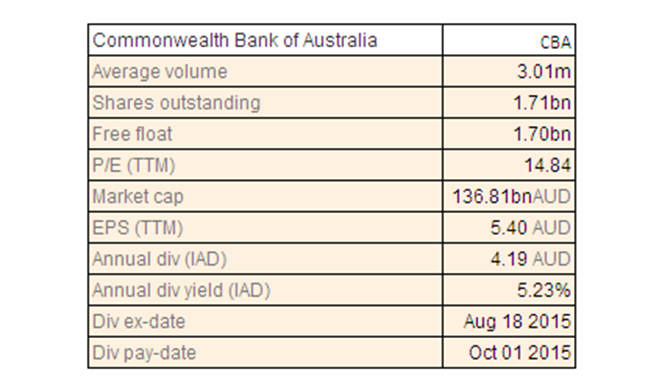

Commonwealth Bank of Australia

CBA Dividend Details

Strengthening capital position: Commonwealth Bank of Australia (ASX: CBA) stock has recovered over 4.83% in the last three months (as at November 27, 2015) as the firm improved its Common Equity Tier 1 (CET1) APRA ratio by 70 basis points to 9.8% during the September quarter, to comply with the APRA regulatory targets by enhancing its capital position via entitlement offer. CBA’s FirstChoice and Custom Solutions delivered an overall net flows of $0.9 billion during the September quarter in the wealth management business. The bank also reduced its bad and impaired assets to $5.5 billion during the September quarter while the total loan impairment expense reached $220 million during the quarter.

We believe that the stock is still expensive at the current price of $79.43

CBA Daily Chart (Source: Thomson Reuters)

QBE Insurance Group Ltd

.png)

QBE Dividend Details

Focusing on operating efficiency: QBE Insurance Group Ltd (ASX: QBE) stock plunged over 13.80% in the last six months (as at November 27, 2015) due to a legal proceeding against QBE by Money Max as well as the group’s poor FY15 performance. The group reported a revenue decline of 6% yoy to $7,928 million in the first half of 2015. On the other hand, QBE delivered an expense savings of $242 million during the period, and estimates to achieve more than $350 million. QBE net profit after tax improved by 24% yoy to $488 million during the period, driven by its sale of Argentine workers’ compensation business in February.

.png)

QBE Insurance Group performance (Source: Company Reports)

The Group recently priced for over US$300 million of subordinated debt for a term of 30 years while earlier priced over $200 million worth of Tier 2 subordinated debt with a term of 25 years, which would boost its gearing ratios as well as divert funds to repay over £300 million of maturing senior debt. QBE has a P/E of about 15x and a dividend yield of about 3.4%. However, QBE reaffirmed its insurance profit margin to be at the bottom end of guidance of 8.5%-10% for the year while the company recently warned its investors of increasing pressures owing to higher competition and pricing conditions that are going to impact revenue growth.

We think that the stock is still overvalued at the current levels.

.png)

QBE Daily Chart (Source: Thomson Reuters)

Suncorp Group Ltd

SUN Dividend Details

Positive Outlook: Suncorp Group Ltd.’s (ASX: SUN) subsidiary, AAI Limited (AAI) recently issued $225 million of floating rate subordinated notes via an offering to institutional and other wholesale market investors. The group is focusing on its core Australian and New Zealand markets and leveraging its leading position to capture the wide range of opportunities, after delivering a poor FY15 performance. Suncorp’s new Optimization program would generate more $170 million of annualized benefits by the fiscal year of 2018. Management issued a positive outlook on the group, which boosted the stock by over 3.30% in the last three months (as of November 27, 2015). SUN is also trading at reasonable valuations with a P/E of about 15x and dividend yield of 5.6%.

Based on the foregoing, we reiterate our “BUY” recommendation for the stock at the current price of $13.39

SUN Daily Chart (Source: Thomson Reuters)

Origin Energy Ltd

.png)

ORG Dividend Details

Increasing production to offset commodity prices pressure: Origin Energy Ltd (ASX: ORG) recently reported that its production increased by 13% to 47.8 PJe for its Integrated Gas business in September Quarter as compared to earlier quarter, on the back of better Australia Pacific LNG production as well as new contribution from Yolla 5 and Yolla 6 production wells in the Bass Basin. ORG is also strengthening its balance sheet and raised over $1.19 billion via a retail entitlement offer. Moreover, Origin’s exploration efforts are generating positive results which would boost its prospects further. Origin’s joint venture of South Australian Cooper Basin with Senex Energy showcased that the first gas exploration well was spudded last month and was cased and suspended for future. Majority of the upstream component of the APLNG CSG to LNG project is finished while the downstream component is 94% finished, and the LNG production has started and the first cargo would be delivered soon. Waitsia-1 appraisal well flow testing generated positive results, wherein the overall combined flow rate is more than 50 mmscf/d.

.png)

Production Results (Source: Company Reports)

On the other hand, the group’s stock corrected heavily during this year falling over 50.18% in the last six months (as at November 27, 2015) on the back of volatile commodity prices. But, Origin Energy also has an outstanding dividend yield and the heavy correction in the shares placed the stock at an attractive opportunity. We maintain our “BUY” recommendation on the stock at the current price of $5.60

ORG Daily Chart (Source: Thomson Reuters)

Scentre Group

.png)

SCG Dividend Details

Efforts to enhance its assets quality: Scentre Group (ASX: SCG) reported that its specialty sales improved by 5.9% yoy for the nine months and rose 5.4% yoy during the third quarter. This solid growth in specialty sales is driven by the group’s efforts to enhance its specialty store rents, as well as decreased specialty store occupancy cost to 17.9%. SCG is selling three shopping centers (Westfield Glenfield, Westfield Queensgate and Westfield Chartwell) in New Zealand, from which they would receive a gross proceeds of NZ$549 million. Scentre Group is focusing to give out its centers to solid retailers to position itself for strong development in future. Accordingly, SCG already built a pipeline of more than $3 billion. Releasing spreads were down 2.5%, which are better than re-leasing spreads in prior corresponding period which decreased by 4.2%. The group estimates the comparable net operating income (NOI) growth for the 12 months to 31 December 2015 in 2% to 2.5% range. Meanwhile, SCG stock surged over 7.5% (as of November 26, 2015) and we believe the positive momentum would continue in the coming periods. The group is also trading at a very cheaper P/E of about 9x and has a decent dividend yield of about 5%. We give a HOLD recommendation on the stock at the current price of $4.00

SCG Daily Chart (Source: Thomson Reuters)

Brambles Ltd

BXB Dividend Details

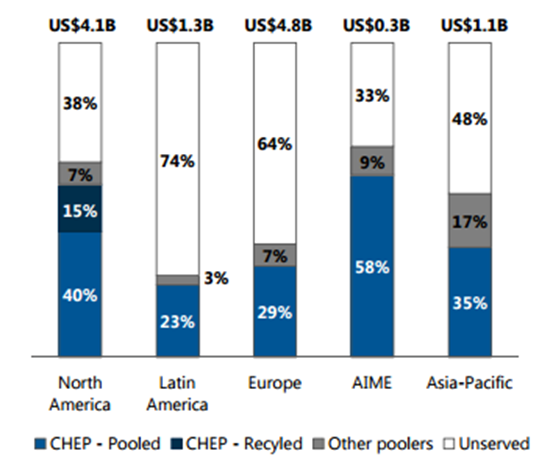

Superior economic returns: Brambles Ltd (ASX: BXB) reported a decent revenue increase of 8% during the first quarter of 2016, with pallets America, EMEA and Asia pacific increasing by 7%, 6% and 5%, respectively. The group estimates its sales revenue and underlying profit growth to be in range of 6% to 8% during fiscal year of 2016. Although BXB estimates its ROCI to be down slightly in FY16 due to short-term impact of its higher investments and acquisitions, the group forecasts its ROCI to be over 20% by FY19, delivering outstanding economic returns driven by its competitive edge on the back of customer value propositions.

Brambles addressable opportunity considering unserved opportunity exists in all markets (Source: Company Reports)

Accordingly, BXB stock surged over 6.86% in the last four weeks (as at November 27, 2015). However, the stock is trading at a relatively high P/E ratio of about 22x and we believe that the stock is expensive at the current price.

BXB Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

AU

AU

Please wait processing your request...

Please wait processing your request...