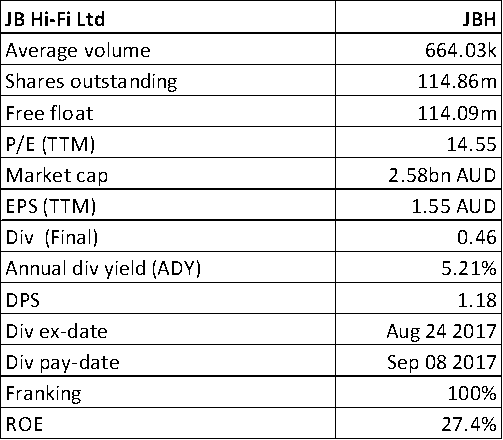

JB Hi-Fi Ltd (ASX: JBH)

JBH Details

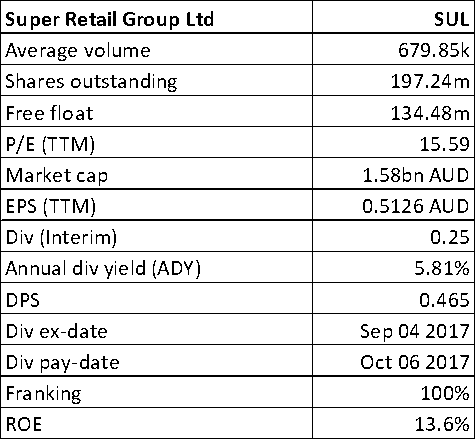

Growth seems to be moderating: JB Hi-Fi Ltd (ASX: JBH) shares have slipped by about 4% in last one month (as at November 16, 2017) at the back of developing pressure from Amazon’s entry in Australia via a two-pronged strategy on platform launches. In FY17, the group could forecast that synergy benefits from the acquisition of The Good Guys are expected to come in at the upper end of JB Hi-Fi’s $15 million to $20 million target and would be fully realised in 2019, one year earlier than anticipated with some benefits flowing in FY18. Total sales at JB Hi-Fi were up 4.3% in FY17 over FY16. The group had some shortcomings with regards to comparable sales growth.

Performance Indicators (Source: Company Reports)

Although the group expects to open five JB Hi-Fi stores and monitor opportunities for new The Good Guys stores for FY18, the growth seems to be moderating going forward with headwinds on macro trends and ability to sustain profits with impact from performance in New Zealand and gearing levels. JBH expects FY18 total group sales to be circa $6.8 billion (JB Hi-Fi $4.65 billion and The Good Guys $2.15 billion). We give an “Expensive” recommendation at the current price of $22.58

.png)

JBH Daily Chart (Source: Thomson Reuters)

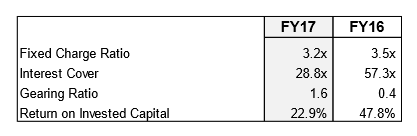

Myer Holdings Ltd (ASX: MYR)

MYR Details

Eying for better trading period: Myer Holdings Ltd (ASX: MYR) has faced tremendous pressure in the last six months and has swooned 23%, as at November 16, 2017, at the back of lower than expected performance and the allegations from Solomon Lew. On the other hand, ISS Governance and CGI Glass Lewis, were said to have been supporting the Myer board and cautioning shareholders against letting Mr Lew to have a control over the retailer without making a takeover bid. The picture will become clearer during the upcoming Annual General Meeting.

For Q1 FY18, the group’s sales of $699.0m, down 2.8% were reported with comparable store sales slipping by 2.1%. On the other hand, sales per square metre were up 3.6% and the online business witnessed a record sales growth of 67.8% over the prior corresponding period. Lately, Myer’s incoming chairman had acknowledged the disappointing results in a letter issued to its shareholders.The group had earlier signalled the tracking of an accelerated rollout of new retail concepts across its store network including six new food partners, five upgraded food offers and 12 locations for new beauty and grooming services. We give a “Hold” recommendation on the stock at the current price of $0.725, till we see some significant signs of recovery while MYR is eying the trading period during Spring Racing and Christmas.

.png)

MYR Daily Chart (Source: Thomson Reuters)

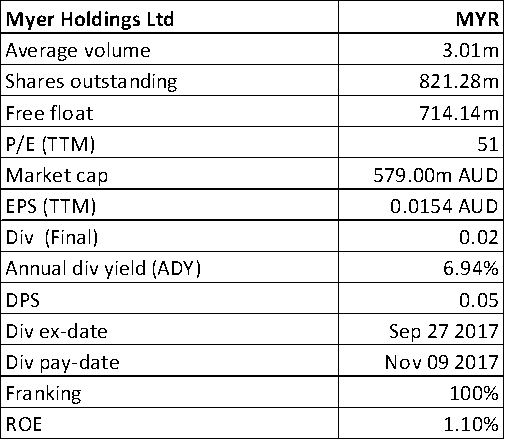

Super Retail Group Ltd (ASX: SUL)

SUL Details

Positive trading update: Super Retail Group Ltd.’s (ASX: SUL) latest trading update of October 2017 reflected a strong lift in like for like sales compared to the same period from last year. The sales performance was strong with Sports team focusing on integrating the Amart Sports business under the Rebel brand. Further, conversion of the former Amart Sports stores is almost over. The Auto Division is also delivering well, and the group expects to open-up ten new stores while refurbishing up to 44 stores. In the Leisure Division, SUL forecasts to open three new BCF stores and one new Rays store. The group is expected to witness revenue growth from $2,423 million to $3,045 million in 2020 and profits are predicted to grow from $63 M to $188 M in 2020. Margins are said to remain at acceptable levels. On the other hand, the group expects to have capital expenditure of about $120 million for the year given the efforts on development, refurbishment and conversion.

Sales Growth for 16 weeks to October 21, 2017 (Source: Company Reports)

The stock seems to provide good value at the back of core fundamentals. Keeping the on-going performance with capital investments and retail industry competition in view while SUL’s return on equity is at a better level, we put a “Hold” recommendation on the stock at the current price of $8.07

.png)

SUL Daily Chart (Source: Thomson Reuters)

Harvey Norman Holdings Ltd (ASX: HVN)

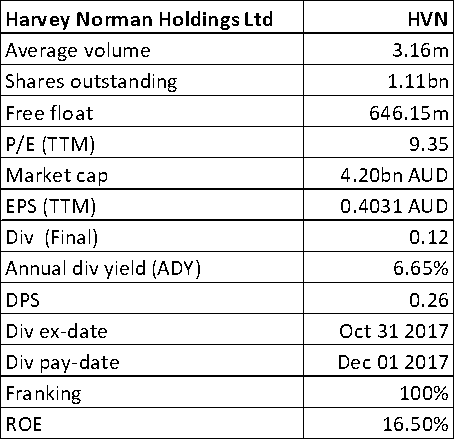

HVN Details

Gearing up on sentiments: Harvey Norman Holdings Ltd.’s (ASX: HVN) shares, which were earlier succumbing under short-selling activity, were seen to soar by 4% in last five days (as at November 16, 2017) at the back of recent sales performance. The group’s sales in Australia for the period 1 July 2017 to 28 August 2017 rose by 4% compared to the period 1 July 2016 to 28 August 2016, and 3.2% on a comparable basis. Further, Harvey Norman, Domayne and Joyce Mayne branded franchisee sales for the period 1 July 2017 to 31 October 2017, were seen to move up 4.8% over prior corresponding period, and up 4.0% on a comparable sales basis. HVN also opened one company-operated store in Ireland and one company-operated store in Singapore while no franchised complexes in Australia were opened or closed during the period. While the market seems to be vouching for the stock, we believe that it might be crucial to wait for more positives given the challenging retail landscape. We put an “Expensive” recommendation on the stock at the current price of $3.95

.png)

HVN Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...