Webjet Ltd

.png)

WEB Dividend Details

Ongoing TTV growth: Webjet Ltd (ASX: WEB) reported a TTV rise of 28.3% in the first half of 2016 to $796 million as compared to $620 million in the prior corresponding period (pcp). The group’s TTV for B2C (digital retail) and B2B (digital wholesale) segments surged by 22.3% and 52.7%, respectively. Webjet’s B2B investments were paid off during the period due to which Lots of Hotels (LOH) TTV increased by 103.3% year on year (yoy). Consequently, Webjet reported a strong overall top line growth of 26.8% while the profit before tax rose by 28.4%. B2C EBITDA rose by 33.6% on a yoy basis while B2B EBITDA remained flat impacted by the group’s investments. But, the group’s Webjet division (under B2C) domestic bookings continued to be very strong driven by the growing shift to online bookings and reported a growth of 14% in 1H16 as compared to the domestic market growth rate of 0.6%. Webjet division International bookings also gained momentum, and generated a 24% increase during the first half of 2016 against the International Bookings market growth rate of 5.2%. Zuji division’s bookings rose by 34% on a yoy basis but margins were under pressure on the back of rising competition. Meanwhile, Webjet Limited declared an Interim Dividend of 6.5 cents per share as compared to the 6.25 cents per share in the pcp.

.png)

First half of 2016 performance (Source: Company Reports)

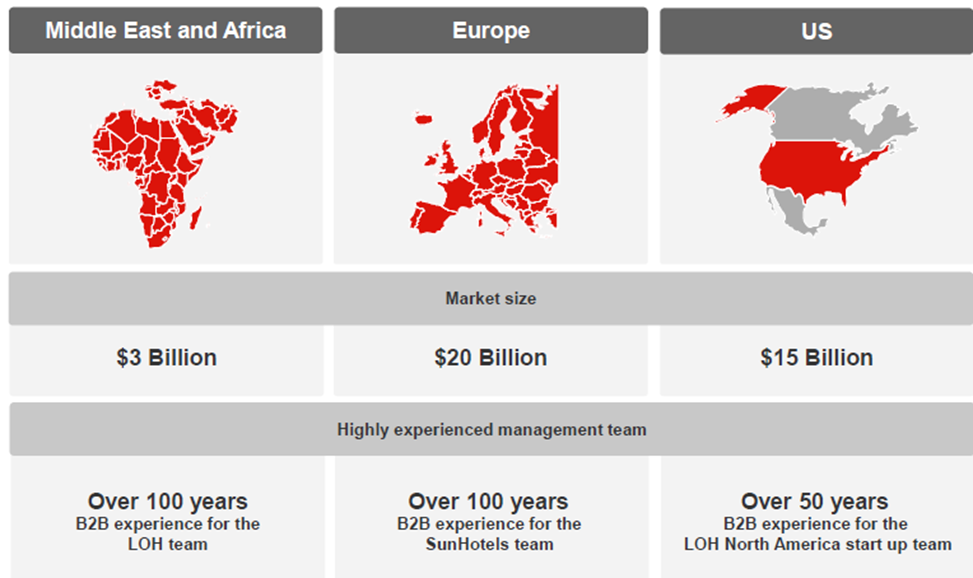

Investing on growth opportunities to boost B2B business: Webjet Ltd is strengthening its B2B business and accordingly making investments to improve this division’s performance further in the coming months. LOH division is the third major player in the Middle East and Africa market and the group is targeting to further expand its customer base via its unique cost model which enables more inventory at lower prices as compared to its peers. Accordingly, LOH enhanced its salesforce by more than 75% on a year on year basis. Moreover, the group intends to replicate the LOH in North American market and therefore making investments of over $1 million. LOH division in North America also signed first client in December 2015 and forecasts a TTV during second half of 2016. Meanwhile, the Sunhotels segment’s booking growth is also picking up, which reported a 10% yoy booking in the first quarter of 2016 and a 25% yoy bookings in the second quarter of 2016. WEB estimates its Sunhotels to generate a bookings growth of 40% yoy during the second half of 2016 and is targeting to further penetrate in existing and new markets including UK, Spain, Germany, Italy, Israel, Turkey, Greece, Russia, Romania, Portugal and Poland. As a result, the group is investing around $2 million in Sunhotels division to improve its direct contracted inventory to 12 key European markets as well as expand its offerings.

B2B division’s market opportunity (Source: Company Reports)

Guidance: Management reported that its TTV increase during the starting of the second half of 2016 is growing at greater than 30% which is a strong increase. But the group has maintained its EBITDA guidance of $33.5 million during the fiscal year of 2016. For B2C business, WEB estimates a better EBITDA growth rate for the FY16 as compared to its five year CAGR EBITDA growth rate of 10%. Even for its B2B business, the group estimates a better EBITDA growth against its five year CAGR EBITDA target growth of 30%. WEB is planning to invest over $3 million in B2B business for fiscal year of 2016. For fiscal year of 2018, B2B TTV is forecasted to be more than $700 million while the division has already generated an annualized TTV run rate of $375 million against a zero base in February 2013. WEB forecasts its B2B TTV to increase organically by >$500 million by FY18 against the TTV of $228 million in FY15. The group estimates its B2B EBITDA to grow double by FY17 with B2B EBITDA forecasted to be over $5.5 million in FY16 and $11 million in FY17.

Stock Performance: The shares of WEB have generated an outstanding performance of 368.19% (as of March 07, 2016) since its listing in ASX and surged over 65.22% in the last six months (as of March 11, 2016), driven by its ongoing TTV increase across its segments coupled with the group’s efforts to position itself in growth markets.

Moreover, the rapid shift to online booking has also contributed to the strong stock performance. On the other hand, the rising competition and ongoing investments by the group to achieve long term growth might hurt its short term performance. Moreover, we believe that the heavy rally in the stock placed WEB at unreasonable valuation which is trading at a high P/E. Based on the foregoing, we give a “SELL” on this stock at the current price of $6.46

.PNG)

WEB Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2016 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

AU

AU

Please wait processing your request...

Please wait processing your request...