Bank of Queensland Ltd

|

Bank of Queensland Ltd |

BOQ:ASX |

|

Average volume |

1.81m |

|

Shares outstanding |

370.77m |

|

Free float |

370.41m |

|

P/E (TTM) |

15.79 |

|

Market cap |

4.85bn AUD |

|

EPS (TTM) |

0.8275 AUD |

|

Annual div (IAD) |

0.74 AUD |

|

Annual div yield (IAD) |

5.66% |

|

Div ex-date |

Oct 29 2015 |

|

Div pay-date |

Nov 24 2015 |

BOQ Dividend Details

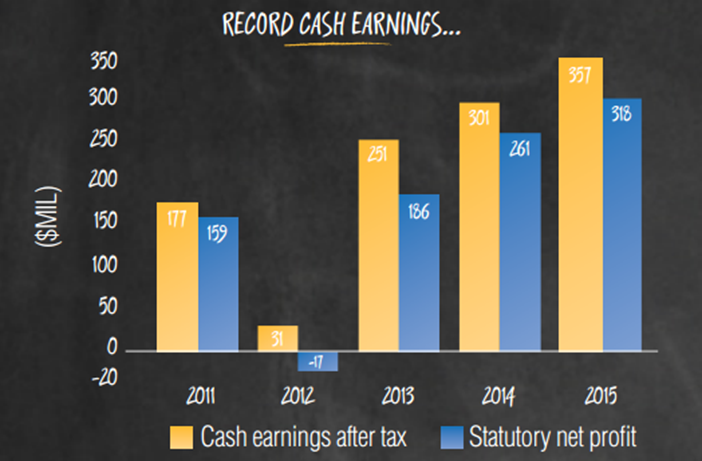

Enhancing customer relationships: Bank of Queensland Limited (ASX: BOQ) was able to deliver solid levels of customer satisfaction wherein it’s Net Promoter Score improved by 36.7 points over the last 2.5 years, as per Independent Roy Morgan research. Bank of Queensland was able to deliver a better total return to shareholders of 6.3% in FY15 as compared to group’s peer banks. The bank recently priced A$550 million of 3.5 year floating rate Notes at a margin of 115 basis points over the 3 month Bank Bill Swap Rate. Earlier, BOQ also raised over $150 million by issuing Wholesale Capital Notes at a margin of 4.35% over the 6 month Bank Bill Swap Rate. The group also maintained its solid performance for fifth consecutive half, and delivered a 19% year on year (yoy) increase of net profit after tax to $357 million during fiscal year of 2015 while the group reported a statutory profit after tax rise of 22% yoy to $318 million. Bank of Queensland is now focusing on its niche segments by developing a better customer banking relationship. The group even enhanced its margins and asset quality during the year as the group’s strategy related efforts paid off.

Improving performance (Source: Company Reports)

BOQ cash earnings surged by 19% yoy to $357 million in FY15 while dividends improved by 12% leading to a rise in total dividends to 74 cents per share during the year. Meanwhile, Bank of Queensland stock rallied over 12.6% in the last four weeks alone (as of Oct 30, 2015) and we believe the positive momentum in the stock would continue in the coming months. BOQ also has a decent annual dividend of 5.7%. We maintain our “BUY” recommendation to the stock at the current price of $12.82

.png)

BOQ Daily Chart (Source: Thomson Reuters)

Westpac Banking Corp

|

Westpac Banking Corp |

WBC:ASX |

|

Average volume |

8.10m |

|

Shares outstanding |

3.32bn |

|

Free float |

3.15bn |

|

P/E (TTM) |

13.24 |

|

Market cap |

104.26bn AUD |

|

EPS (TTM) |

2.37 AUD |

|

Annual div (IAD) |

1.86 AUD |

|

Annual div yield (IAD) |

5.94% |

|

Div ex-date |

May 13 2015 |

|

Div pay-date |

Jul 02 2015 |

|

Next div ex-date |

Nov 11 2015 |

|

Next div pay-date |

Dec 21 2015 |

WBC Dividend Details

Full Year Result driven by Australian Retail and Business Banking: Westpac Banking Corp (ASX: WBC) announced its result with statutory net profit for the 12 months to 30 September 2015 surging up 6% to $8,012 million as opposed to prior year in view of WBC’s service-led strategy. Cash earnings per share of 249.5 cents reflected a rise of 2% while cash return on equity was reported to be 15.8%, down 57 basis points. However, cash earnings of $7,820 million were up 3%. Westpac Retail & Business Banking emphasized on service. This along with Australia’s leading mobile/online capability for customers led to core and cash earnings growth of 8%.

.png)

Divisional Performance (Source: Company Reports)

An important highlight was the fully franked dividend of 94 cents per share (cps) which led the total dividends paid for the year to be 187 cps, which is an increase of 3%. There was a rise in lending and customer deposit growth by 7% and 4% respectively. Common equity tier 1 capital ratio of 9.5% was reported. WBC reported weak performance in wealth and institutional businesses. The outlook was not explicit but indicated positive essence given low interest rates, low AUD and shifts to service-sector.

Service based strategy; boosting capital position: WBC increased its interest rates to comply with CET1 ratio requirements, with home loan variable rates rising by 20 basis points per annum to 5.68% per annum and residential investment property variable rates improving by 20 basis points per annum to 5.95% per annum. The group also undertook a renounceable entitlement offer to raise around $3.5 billion of ordinary equity, with the price of the offer at $25.50 per ordinary share. Westpac would improve its CET1 capital ratio by 100 bps via this offer. The group is increasing its annual investment by 20% to over $1.3 billion for service, growth and efficiency. Accordingly, Westpac estimates to add around 1 million new customers from 2015 till 2017 and also building a Customer Service Hub by merging multiple technology systems to a single view of the customer. On the other hand, Westpac was ordered by ASIC to pay refunds for WBC clients for selling insurance when they did not need it and collecting unnecessary premiums.

.png)

Full Year Result (Source: Company Reports)

WBC shares fell over 9.17% in the last three months (as at October 30, 2015) and we believe the pressure on stock might continue in the coming months. Despite the group’s efforts to drive its customer’s base, we believe that the stock might face short term pressure due to ASIC investigation impact and the group’s efforts to comply CET1 ratio targets. Based on the foregoing we give an “Expensive” recommendation to the stock at the current price $30.61

WBC Daily Chart (Source: Thomson Reuters)

Bendigo and Adelaide Bank Ltd

|

Bendigo and Adelaide Bank Ltd |

BEN:ASX |

|

Average volume |

1.26m |

|

Shares outstanding |

456.73m |

|

Free float |

455.41m |

|

P/E (TTM) |

12.25 |

|

Market cap |

4.89bn AUD |

|

EPS (TTM) |

0.8736 AUD |

|

Annual div (IAD) |

0.66 AUD |

|

Annual div yield (IAD) |

6.17% |

|

Div ex-date |

Aug 18 2015 |

|

Div pay-date |

Sep 30 2015 |

BEN Dividend Details

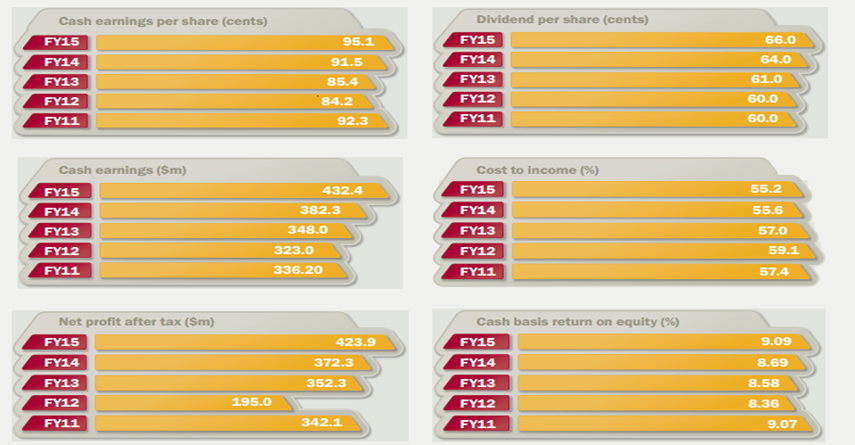

Stock highlights: Bendigo and Adelaide Bank Ltd (ASX: BEN) reported underlying cash earnings increase of 13.1% yoy to $432.4 million in FY15 while its net profit after tax rose to $423.9 million during the period against $372.3 million in FY14. BEN also enhanced its balance sheet position wherein Basel III common equity tier 1 ratio rose 15 basis points to 8.17%, while the total capital surged by 118 basis points to 12.57%. The group is focusing on its Basel II advanced accreditation program to enhance its risk management practices, processes and systems to drive value for shareholders in the long term.

Performance highlights over last few years (Source: Company Reports)

On the other hand the group’s wealth management business was under pressure during FY15 although the group delivered better agribusiness performance. The stock of BEN also corrected over 18.45% in the last three months (as of Oct 30, 2015) and we estimate this short term pressure in the stock to continue in the coming months. We believe BEN shares are trading at higher valuations and accordingly give an “Expensive” recommendation to the stock at the current price $10.47

BEN Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

AU

AU

Please wait processing your request...

Please wait processing your request...