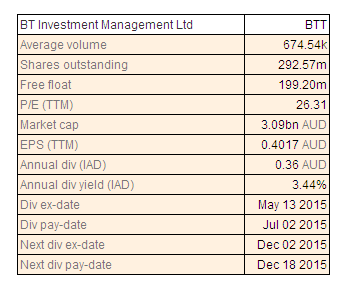

BT Investment Management Ltd

BTT Dividend Details

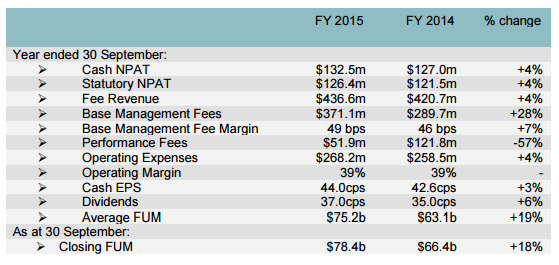

Record Performance for the year: BT Investment Management Ltd (ASX: BTT) announced its record result of cash net profit after tax of $132.5 million which surged by 4% over prior corresponding period. Cash earnings also went up 3% to 44 cents. The Company reported a 6% surge in total dividends up to 37.0 cents per share. Further, 28% rise in base management fees was another highlight. The company delivered about 493% total shareholder return on a three-year basis. Funds under management rose to over $78 billion, which is indicative of $12 billion rise over the year partly owing to lower Australian dollar. However, we did note that total funds under management fell to $78.4 billion as at September 2015, as compared to $78.9 billion in June 2015. Meanwhile, the group recently extended the Master relationship agreement (MRA) with Westpac owned BT Financial group. On the other hand, MRA related funds under management reached $17 billion as at September 30, 2015, while the effective management fee for FUM declined from 32 basis points to 29 basis points translating into a loss of $5.1 million in terms of revenue. BT Investment Management reported a weak financial performance with performance fees falling to $38 million in the six months ended on March 2015 as compared to $114.7 million in pcp.

Results for year ending 30 September 2015 (Source: Company Reports)

The shares of BTT already delivered outstanding performance of generating over 53.86% during the year to date (as at 28 Oct, 2015), due to which the stock is trading at expensive valuations, with P/E trading higher at over 25x which is a little above most of the peers. Accordingly, we give an “Expensive” recommendation to the stock at the current price of $11.35

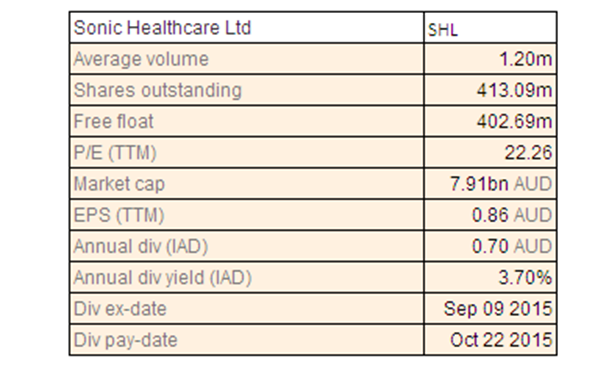

Sonic Healthcare Limited

SHL Dividend Details

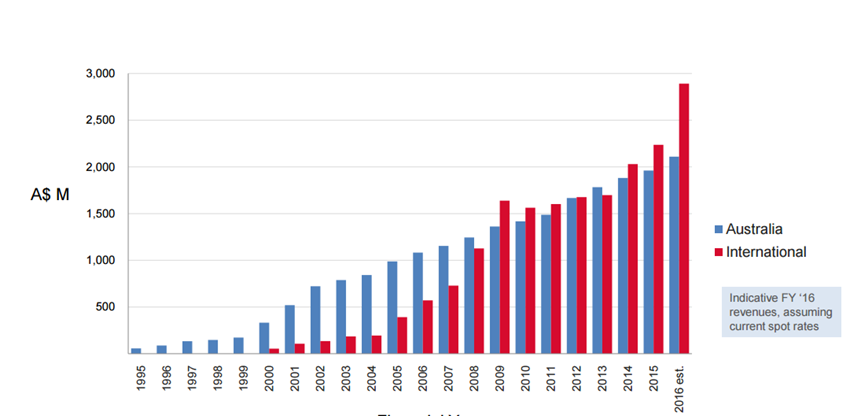

Focusing on international business: Sonic Healthcare Limited (ASX: SHL) reported an overall revenue growth of 7.3% year on year (yoy) to $4,201 million in fiscal year of 2015, boosted by synergies from the group’s acquisitions along with enhanced performance in US, Germany, UK and Switzerland regions despite tough Australian laboratory market conditions. The group’s US business improved on the back of the restructure of CBLPath from which SHL achieved a recurring annual savings of greater than US$10 million. European business revenues surged by 25% yoy, driven by three months contribution of joint venture with UCLH and Royal Free coupled with solid private market growth. The group estimates an ongoing growth of its UK revenues and accordingly projects a 40% revenue increase during FY16. There are market speculations about SHL’s interest in bidding for Unilabs SA (Swiss Diagnostics Company) wherein the deal is expected to be worth €1.5 billion.

International business growth (Source: Company reports)

However, the shares of SHL corrected over 6.27% (as of Oct 28, 2015) in the last three months as the group decreased its profit guidance before the release of its full year results. Moreover, SHL’s net profit fell more than estimated by 5.6% yoy to $363 million affected by the Australian collection infrastructure costs. The group also incurred a Non-recurring costs of over $14 million due to CBLPath restructure costs, New Zealand contract exit costs as well as acquisition costs. SHL shares are also trading at higher P/E of 21.15x. It is yet to be seen that how the Australian government’s review of the Medical Benefits Scheme for examining the merits of 5,700 subsidized items affects Sonic Healthcare. Given the overall scenario, we maintain our “Expensive” recommendation to the stock and would review the stock at a later date.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

AU

AU

Please wait processing your request...

Please wait processing your request...