Myer Holdings Ltd

.png)

MYR Dividend Details

Falling profit: Myer Holdings Ltd(ASX: MYR) recently reported half yearly financial results with total sales higher by 1.8% to $1,794.8 million. Net profit after tax was down 4% to $59.7 million while basic earnings per share stood at 7.9 cents compared to 10.6 cents in earlier period. The company is looking to rollout New Myer initiatives in the second half which will lead to increased costs and capex. For full year 2016, MYR now expects a reduced net profit after tax, between $66 and $72 million compared to earlier estimated $64 and $72 million. However, this is based on no significant deterioration in consumer sentiment.

Trading at a high P/E ratio, recording an almost 21.35% (as of April 08, 2016) gain in the past six months and falling profit numbers, we recommend a "Expensive" rating on the stock at the current share price of $1.08

MYR Daily Chart (Source: Thomson Reuters)

Super Retail Group Ltd

.png)

SUL Dividend Details

High dividend and strong cash flow: Super Retail Group Ltd (ASX: SUL) recorded its first half financial year results with group total segment sales rising by 6% to $1.21 billion, while net profit after tax attributable to owners rose 33.6% to $44.9 million. SUL has a strong working capital management as indicated by a 26% growth in operating cash flow to $177 million.

.png)

Divisional results (Source: Company reports)

Trading with a high dividend yield at the back of a strong performance, makes us believe that there is room for growth and thus recommend a "Speculative Buy" at the current share price of $8.15

.PNG)

SUL Daily Chart (Source: Thomson Reuters)

JB Hi-Fi Limited

.png)

JBH Dividend Details

Growing stores and strong dividend: For the first half financial year 2016, JB Hi-Fi Limited (ASX: JBH) recorded total sales of $2.12 billion, an increase of 7.7% from prior year period. Meanwhile, comparable sales were up by 5.2% and gross profit up by 7.6%.

.png)

Rising store count (Source: Company reports)

Net profit after tax stood at $95.2 million, an increase of 7.5%. For full year 2016, JBH expects total sales to be around $3.9 billion and net profit after tax in the range of $143 to $147 million. In the past six months, the company's stock price increased 22.76% and is currently trading close to its 52-week high levels (as at April 08, 2016). We recommend a "HOLD" at the current share price of $22.60

JBH Daily Chart (Source: Thomson Reuters)

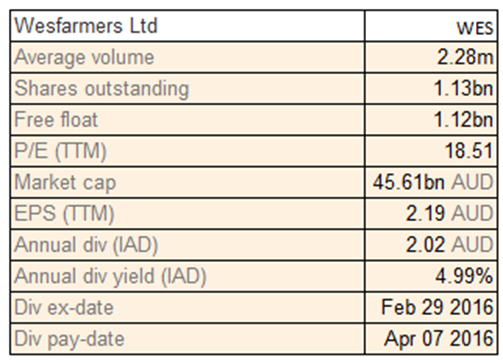

Wesfarmers Ltd

WES Dividend Details

Challenging Resource business outlook: Recently, Wesfarmers Ltd (ASX: WES) completed the acquisition of the Homebase business from Home Retail Group Plc for A$ 658 million. Besides, it was also known that the Australian Competition and Consumer Commission (ACCC) has decided not to oppose Coles' (owned by WES) proposed acquisition of five Supabarn supermarkets in NSW and the ACT as the brand would be free to compete under its name even post the acquisition. In its latest financial results, WES stated that low export coal prices, locked-in currency hedge book losses and production impacts due to wet weather lead to a difficult short term outlook for its Resources business.

Then impact from Tassal’s decision on withdrawing tenders for two supply contracts with Wesfarmers-owned Coles is yet to be seen. With a relatively high P/E and a challenging short-term outlook for the Industrials division, we believe that the stock is "Expensive" at the current share price of $40.33

WES Daily Chart (Source: Thomson Reuters)

Metcash Ltd

.png)

MTS Dividend Details

Stable financials: For first half financial year 2016, Metcash Limited(ASX: MTS) recorded group revenue increase of 1.4% to $6.6 billion. Underlying EBIT stood at $133.7 million in line with expectations. Looking ahead, the company believes that the food & grocery headwinds would not be offset even by the positive results in ALM & Hardware and strategic initiatives in Food & Grocery.

.png)

Financial overview (Source: Company reports)

But given its stable financials and efforts to maintain performance, we give a "HOLD" recommendation on the stock at the current share price of $1.66

.PNG)

MTS Daily Chart (Source: Thomson Reuters)

Beacon Lighting Group Ltd

.png)

BLX Dividend Details

Increase in sales with surge in margins: For its first half financial year 2016 results, Beacon Lighting Group Ltd (ASX: BLX) reported an increase of 8.5% in its sales to $98.5 million with company stores comparative sales rising 5.1%. EBITDA and NPAT increased 21.4% and 22.1% to $17.5 million and $11.1 million, respectively. Gross profit dollars went up 11.5% with strong gross profit margin of 65.9% led by innovative new products.

During the period, BLX opened two new company stores and purchased two franchised stores. Interim dividend for the period increased by 27.8% to 2.3 cents, over from same period a year ago. However, BLX stock is trading at a relatively low dividend yield and a high P/E ratio. We rate the stock "Expensive" at current share price of $2.04

BLX Daily Chart (Source: Thomson Reuters)

Nick Scali Limited

.png)

NCK Dividend Details

Ownership changes:Nick Scali Limited (ASX: NCK) has been delivering strong performance while management reaffirmed guidance of continued sales growth in the second half of the year with full year net profit after tax expected to be in the range of $22 to $24 million. Accordingly, the stock surged over 12.06% in the last six months (as of April 08, 2016). On the other hand, the group’s managing director recently increased interest in the company following sell down of part of Scali family interest to institutions. On the other hand, the ongoing volatile housing conditions seem to have an impact the group.

Therefore, the stock fell over 2.34% in the last three months (as of April 08, 2016) and we believe that the negative momentum may continue in the coming months and hence give an "Expensive" recommendation to NCK at the current share price of $4.18

NCK Daily Chart (Source: Thomson Reuters)

Cash Converters International Ltd

.png)

CCV Dividend Details

Strategy change and shift to profit levels: Cash Converters International Ltd (ASX: CCV) in its half yearly financial results reported a net profit after tax of $15.9 million compared to a loss of $5.3 million in year ago period. Revenue was up 5.8% to $198.6 million in same period. The growth was driven as Australia and United Kingdom improved, and there was strong online lending growth in Australia.

.png)

EBITDA Split (Source: Company reports)

Post its half yearly results, CCV announced a major change in its strategy which will now focus on building its brand and network strengths in Australia and significantly change strategy and structure for United Kingdom operations. Meanwhile, the stock is also trading at a good dividend yield and based on the foregoing, we maintain our "BUY" rating on the stock at the current share price of $0.54

CCV Daily Chart (Source: Thomson Reuters)

Automotive Group Holdings Ltd

.png)

AHG Dividend Details

Successful divestments: Automotive Group Holdings Ltd (ASX: AHG) completed the divestment of its Covs business to GPC Asia Pacific while retaining four of its stores (to be rebranded as Skipper Transport Parts in its AMCAP business). AHG also delivered record half yearly profit and an increased interim dividend led by outperformance in Automotive. The company has completed the acquisition of the Knox Mitsubishi dealership involving a total consideration of $5.4 million leading to AHG’s network to move up to 179 franchises at 104 dealership locations in Australia and New Zealand.

.png)

Financial metrics (Source: Company reports)

Statutory net profit after tax increased 7% to $48.2 million from prior year period, while group revenue rose 7.2% to $2.75 billion.

Operating EBITDA increased 8% to $112.4 million while Interim dividend rose to 9.5 cents from 9.0 cents earlier. Meanwhile, the group is also trading at attractive valuations at a reasonable P/E and has a solid dividend yield. Accordingly, we rate the stock "BUY" at the current share price of $3.87

AHG Daily Chart (Source: Thomson Reuters)

Woolworths Ltd

.png)

WOW Dividend Details

Reshaping the portfolio: Recently, Woolworths Limited (ASX: WOW) announced that Moody's Investors Service downgraded its issuer rating and senior unsecured notes rating by one notch to Baa2 with a negative outlook while Standard & Poor’s BBB+ (negative outlook) rating remains unchanged. On the other hand, WOW continues to have a solid credit profile and is confident that with the execution of its strategy it will deliver the best outcome for its customers and investors.

.png)

Rebuilding the business (Source: Company reports)

Looking ahead, WOW is making progress in the rebuilding of Woolworths with significant investment in price, service and customer experience in the Australian supermarkets, exit from the Home improvement business and appointment of a new Group and BIG W CEO.

With a strong dividend yield and the stock correcting around 7.56% in the past three months (as at April 08, 2016), the stock is expected to record gains in the upcoming months and thereby rate it a "BUY" at the current share price of $21.14

WOW Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2016 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

AU

AU

Please wait processing your request...

Please wait processing your request...