Stocks’ Details

The A2 Milk Company Limited

Annual Meeting is to be held on 19 November 2019:The A2 Milk Company Limited (ASX: A2M) sells branded products made with cow’s milk in the targeted markets. It has a market capitalisation of A$9.62 Bn as on 16th September 2019. The company recently announced that it would be conducting its Annual Meeting on 19th November 2019. It added that UBS Group AG and its related bodies corporate has become an initial substantial holder in the company with the voting power of 5.03%. In FY19, the marketing spends of the company stood at $135.3 Mn, representing 10.4% of sales and a rise of 83.7%. The company made a significant investment in building depth and breadth of organisational capability in order to support continued growth and resilience.

What to Expect:As per the Annual Report 2019, the company expects continued growth in revenue throughout its key regions supported by increasing brand and marketing investment in China and the US. It added that the full year FY20 EBITDA as a percentage of sales is anticipated to be broadly consistent with 2H FY19 EBITDA margin of 28.2% which primarily reflects (1) increased full-year marketing investment to around 12% of sales, (2) Continued investment in organisational capability to support future growth. It also added that gross margin percentage is anticipated to be broadly consistent with that of FY19. A2M added that, with a strong balance sheet and cash position, it retains the flexibility to support its growth strategy.

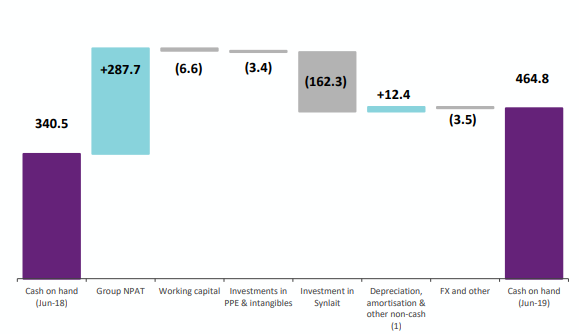

Cash Position (Source: Company Reports)

Stock Recommendation:The cash balance of the company stood at NZ$464.8 Mn in FY19, reflecting a rise of 61% as compared to the figure at the end of December 2018. This increase is because of strong NPAT contribution, partially offset by Synlait investment. The company increased its investment in Synlait to 17.4% shareholding in August 2018. On the stock’s performance front, it delivered negative returns of 13.83% and 5.70% in the time period of one month and three months, respectively. As per ASX, the stock of A2M is trading marginally higher than its 52-week low-high average range of $8.14-$17.30. Based on the foregoing, we advise investors to take a watch stance on the stock at the current market price of A$13.600 per share (up 3.976% on 16th September 2019 and for few more drivers that may drive the stock higher.

Wattle Health Australia Limited

Updates on Debt Funding Facility:Wattle Health Australia Limited (ASX: WHA) is primarily into developing, sourcing and marketing of high-quality Australian made nutritional dairy products. The market capitalisation of the company stood at A$71.97 Mn as on 16th September 2019. As per the release dated 2nd September 2019, the company announced that it is in final stages of finalisation of negotiations on a debt funding facility for its proposed acquisition of Blend & Pack. The company further stated that Blend & Pack is the leading independent (by volume) CNCA accredited dairy manufacturing facility in Australia. It mentioned that GL Foods Pte Ltd has agreed to an extension of the completion date for the proposed acquisition of Blend & Pack.

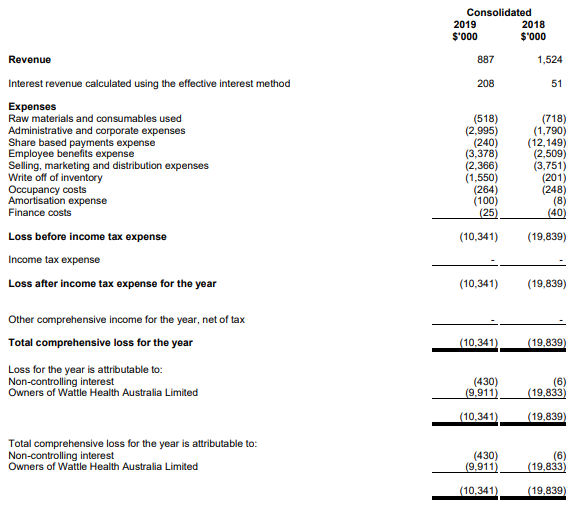

The company further stated that FY19 was a challenging year for the group but a transformative one with WHA to become one of the few vertically integrated organic nutritional dairy companies in the world.The following picture depicts an idea of profit and loss for FY19:

Profit & Loss Statement (Source: Company Reports)

Future Guidance:The company would be focusing on producing and selling a wide range of certified organic based and produced dairy products, this being one of the fastest-growing segment of the nutritional dairy products sector both domestically and internationally.

Stock Recommendation:Wattle Health Australia Limited possesses a strong balance sheet and cash balance with net assets of the group at around $51 Mn with cash at bank of circa $28 Mn. As per ASX, the stock of WHA is trading closer to its 52-week lower levels of $0.355, proffering a decent opportunity for accumulation. In light of above-stated facts and current trading levels, we give a “Speculative Buy” recommendation on the stock at the current market price of A$0.370 per share on 16th September 2019.

Blackmores Limited

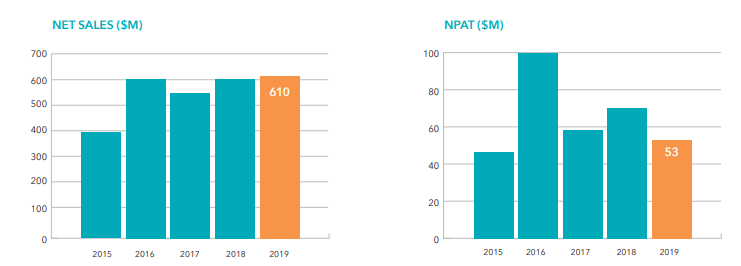

A Quick Look at Dividend Reinvestment Plan:Blackmores Limited (ASX: BKL) is involved in the development, sales and marketing of natural health products for humans and animals. It has a market capitalisation of A$1.33Bn as on 16th September 2019. Recently, the company announced that it has issued 33,077 fully paid ordinary shares at a price of $69.27. The objective behind this is a dividend reinvestment plan with respect to 2019 final dividend. In another update, the company announced that Christine Holman has made a change to the holdings in the company by acquiring 1,000 fully paid ordinary shares at the consideration of $64.90. Post-change, the total securities held with Christine Holman stood at 2,500 fully paid ordinary shares. The following picture depicts an overview of the key metrics of the company for FY19:

Key Metrics (Source: Company Reports)

Future Aspects:As per the Annual Report 2019, the challenging trading conditions in its channels to China are anticipated to continue during 1H FY20. The impact of changes to China’s e-commerce laws and costs associated with restructuring and the Braeside acquisition isanticipated to result in profit for the 1H being below the pcp.The 2H FY20 is anticipated to benefit from operational efficiencies because of the execution of business improvement initiatives.

Stock Recommendation:The Board of the company has declared final dividend amounting to 70 cps, which takes the total dividends for the year to 220 cps, fully franked. The final dividend was paid on 12th September 2019. Coming to the stock’s performance front, it produced negative returns of 3.90% and 16.43% in the time period of one month and three months, respectively. Currently, the stock is trading below the average of 52-week high and low levels of $63.64 and $149.64, respectively. On the valuation front, it reported a higher Price to Cash Flow multiple of 49.2x and P/E multiple of 24.83x on TTM basis as compared to the industry median of 6.2x and 6.9x, respectively showing that the stock is overvalued. Hence, in light of above-stated facts coupled with stretched valuations and current trading levels, we advise investors to closely watch the stock at the current market price of $84.0 (up 9.403% on 16 September 2019) and wait for better entry levels.

.PNG)

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...