QBE Insurance Group Ltd

QBE Details

Declining NSW compulsory third party (CTP) insurance scheme: QBE Insurance Group Ltd (ASX: QBE) reported a rise in gross written premium from $13.7 billion to $14.1 billion in H1FY16. Net earned premium increased from $11.5 billion in 1H15 to $11.9 billion in 1H16 with rise in operating ratio to 95%. Insurance premium margin increased from 8.5% to 10%. QBE declared an interim dividend of 21 cents per share, which is an increase of 5% over H1FY15. Going forward, the group estimates to achieve $150 million in FY16 reduction in expenses.

On the other hand, the stock has corrected over 10.9% in the last three months (as at October 03, 2016) as the group’s first half of 2016 performance is lower than estimated.

.png)

First half of fiscal year 2016 (Source: Company Reports)

Moreover, the declining performance of its NSW compulsory third party (CTP) insurance scheme in its ANZ markets remains a concern.

Also trading at a relatively high P/E, we rate the stock “Expensive” at the current market price of $9.42

QBE Daily Chart (Source: Thomson Reuters)

Medibank Private Ltd

.JPG)

MPL Details

Concern over rising competition:Medibank Private Ltd (ASX: MPL) has a strong Return on Equity and has no debt in books. Medibank also enjoys tailwinds from ageing population and increase in demand for healthcare. For FY16, the company reported 4% rise in health insurance premium to 6.17 billion while operating profit grew 54.6% to $535.5 million. Net profit after tax was at $417.6 million, up 46.4%. The group declared dividend of 11 cents per share. The concern for the group is however the rising competition and low customer base.

The group’s customer numbers declined 2.6%, indicating that the group had lost market share. We rate the stock as “Expensive” at the current market price of $2.43

.png)

MPL Daily Chart (Source: Thomson Reuters)

ASX Ltd

ASX Details

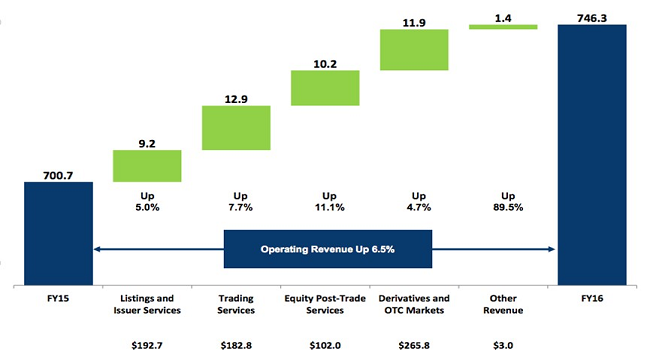

Acquisition of stake: ASX Ltd (ASX: ASX) is acquiring 1.4 million shares for $16.2 million at the placement price of $11.35 per share of IRESS Ltd. With this acquisition, ASX’s shareholding in IRESS is 19.1%. Meanwhile, the company reported a revenue rise of 6.5% to $746.3 million in FY16 and witnessed a similar increase in EBITDA to $575.7 million. Net profit grew 5.7% to $426.2 million. The company is maintaining a 90% payout ratio, while declared a dividend of 198.1 cents per share, which is up 5.1% as compared to previous year.

Going forward ASX would invest in development of future trading platforms, risk management and post trade in FY17. It would further focus on investment in digital asset holdings and opportunity for post trade innovation.

Revenue movement (Source: Company Reports)

Trading at a higher P/E, we give the stock an “Expensive” recommendation at the current price of $49.11

ASX Daily Chart (Source: Thomson Reuters)

Healthscope Ltd

HSO Details

Impressive bottom line growth:Healthscope Ltd (ASX: HSO) reported an impressive 18.9% bottom line growth to $182.8 million for FY16. HSO revenue was up 6.2% to $2.291 million while EBITDA was up by 7.1% to $407.9 million. Hospital operating EBITDA was up 8.3% to $354.9 million while New Zealand Pathology operating EBITDA was up 21.8%. The group declared a dividend of 7.4 cents per share, which includes final dividend of 3.9 cents per share.

FY16 witnessed continued organic growth and margin expansion across hospital operations. During the year, the group has renegotiated multi-year contracts with major health fund providers like Bupa, Medibank and HCF.

.png)

Construction pipeline (Source: Company Reports)

Capex was at $440 million in growth capital projects and the group has completed seven hospital expansion projects. There are total 17 hospital construction projects underway in FY16 which includes nine major hospital projects.

The group is set to conduct AGM on October 21, 2016. With the rising ageing population, we see potential going forward and recommend a “Hold” on the stock at the current market price of $3.11

.png)

HSODaily Chart (Source: Thomson Reuters)

Mcgrath Ltd

MEA Details

Acquired Smollen group:Mcgrath Ltd (ASX: MEA) reported 12% rise in revenues to $137 million on 11% rise in sales. Net profit dipped 7% to $14.6 million and the company declared a dividend of 3.5 cents per share. Company’s agent count increased by 77 to 642 number.

The company increased its market share by 3.4% to 8.5%. Mcgrath acquired the Smollen Group with 10 offices, which helped to increase the exposure to Sydney’s growth corridor.

.png)

Market share (Source: Company Reports)

The group will conduct its AGM in November 2016. Meanwhile, Mcgrath stock is trading at a reasonable P/E and we give a “Buy” on the stock at the current market price of $1.17

MEA Daily Chart (Source: Thomson Reuters)

Adairs Ltd

ADH Details

Outperformed prospectus forecast and guidance: Adairs Ltd (ASX: ADH) revenues grew 17.3% to $247.4 million while Like for like (LFL) sales were up by 21.6% to 11.7%. Net profit grew 18.9% to $26.1 million and company declared full year dividend of 11.5 cents per share. During the year, the company opened 13 new stores and has a rollout program of $8 crore and 5 emerging stores. Company’s international expansion commenced with the signings of 3 stores in New Zealand for FY17. For FY17, the management expects sale in the range of $275-285 million with sustainable gross margins of 60-62%. For FY17, capex is planned at ~15 million and year-end stores would be 160-165.

The group’s AGM will be held in November 2016. On the other hand, the stock already rose over 17.3% in the last six months (as of October 03, 2016) reaching a slightly higher level. We rate the stock as “Expensive” at the current market price of $2.65

ADH Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...