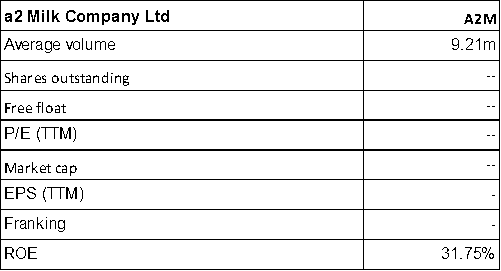

a2 Milk Company Ltd

A2M Details

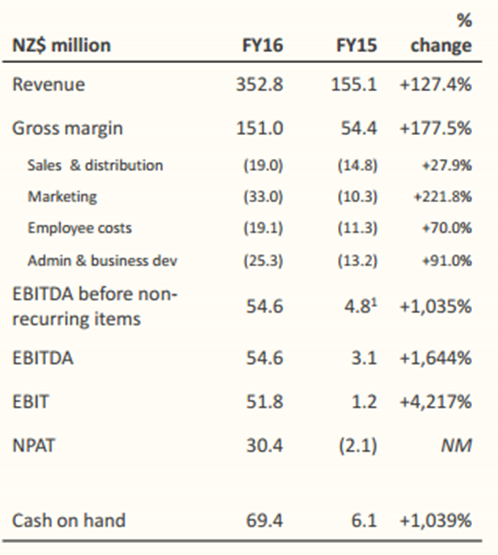

Turnaround to Profit from loss: a2 Milk Company Ltd (Australia) (ASX: A2M) reported the revenue growth of 127.4% to $352.8 million in FY 16 over the prior corresponding period (pcp). Consequently, the net profit after tax rose $30.4 million, as compared with a net loss after tax of $2.1 million in the pcp. Major driver for this outstanding performance is the exceptional growth in sales of a2 Platinum infant formula in Australia & New Zealand (ANZ) and China, with the total revenue of $214.4 million, up 414% on pcp. The gross margin reflects change in product mix, with infant formula now the largest component of group sales. The increased investment in marketing and brand development to 9.4% of net revenue reflects targeted increased spend in ANZ, China and USA.

FY 16 Financial Performance (Source: Company Reports)

Moreover, the group boosted cash via equity raising via private placement and share purchase plan combined with strong positive operating cash flow in the 2

nd half of FY 16. A2M continues to focus on growing the ANZ and China businesses and developing the market opportunities in the United Kingdom and United States.

The group is progressing plans for the New Zealand liquid milk market after the expiry of the last remaining nonexclusive license with Fresha Valley in May 2017. Meanwhile, A2M stock has risen 26.4% in the last three months (as of August 31, 2016), and we give a “Hold” recommendation on the stock at the current price of $1.825

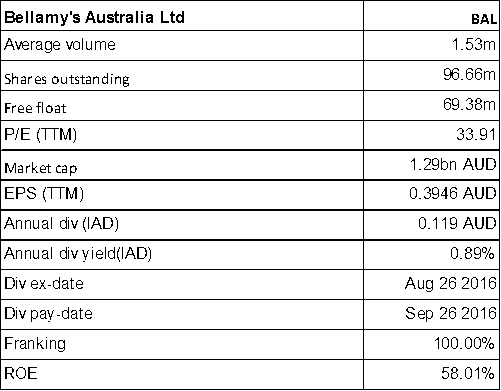

Bellamy’s Australia Ltd

BAL Details

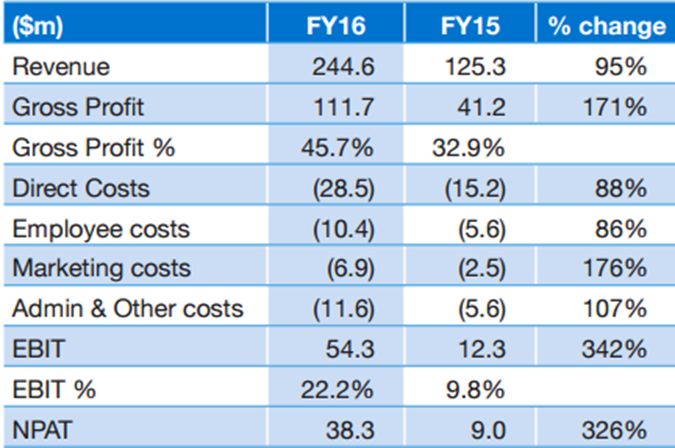

Delivered solid performance, ending China concerns: Bellamy's Australia Ltd (ASX: BAL) has reported an EBIT growth of 342% to $54.3m in FY 16, the revenue grew 95% to $245m in which China’s revenues rose 331% and the NPAT grew by 326% to $38.3m.

FY 16 Financial Performance (Source: Company Reports)

The EBIT margin has more than doubled from 10% in FY15 to 22% in FY16. Moreover, BAL has a strong cost management driven by the growth in the business infrastructure as the head count has increased by 50%. BAL’s total dividend is up 316% to 11.9cps fully franked and the dividend represents payout ratio of 30% of FY NPAT.

BAL would continue to utilize the growing earnings and cash flows to invest in its supply chain in FY 17 as well as undertaking other initiatives to drive sustainable growth and further optimize long term returns. Meanwhile, BAL stock has risen 20.11% in the last three months (as of August 31, 2016) and we maintain our “Hold” recommendation on the stock at the current price of $13.40

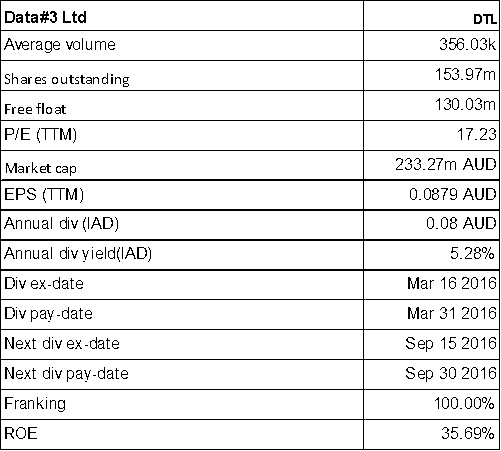

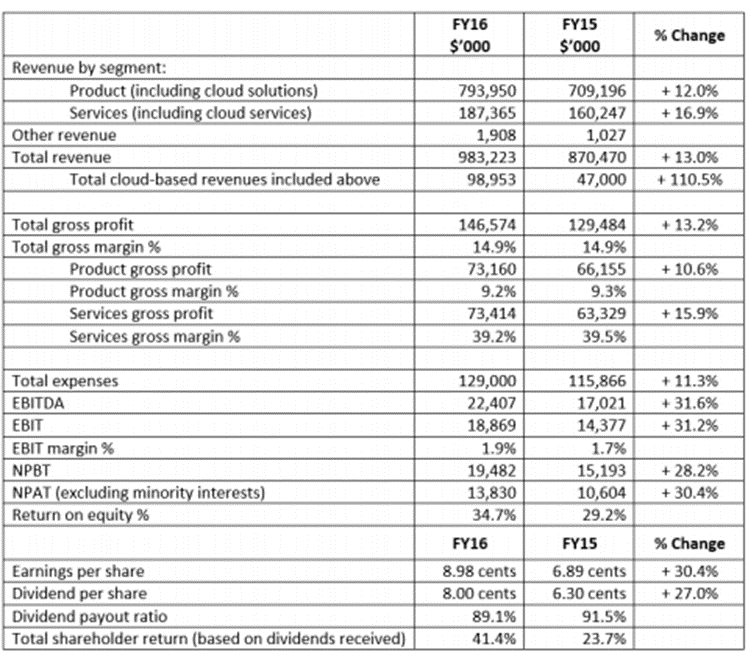

Data#3 Limited

DTL Details

Change in business mix: Data#3 Limited (ASX: DTL) reported a 13% increase in the total revenue in FY 16 to $983.2m. The group is making a strategic shift in the business mix. The product gross margin decreased fractionally from 9.3% to 9.2%. There was a 10.6% increase in product gross profit and the services gross profit reported 15.9%. Net profit after tax (excluding minority interests) was up 30.4% to $13.8m.

FY 16 Financial Performance (Source: Company Reports)

The company has also revealed its board succession planning with Ian Johnston, the non-executive director’s retirement and appointment of Leanne Muller as the Chairman of audit and risk committee. Meanwhile, DTL stock has risen 41.6% in the six months (as of August 31, 2016) and the stock has a decent dividend yield. Based on the foregoing, we give a “Hold” recommendation on the stock at the current price of $1.585

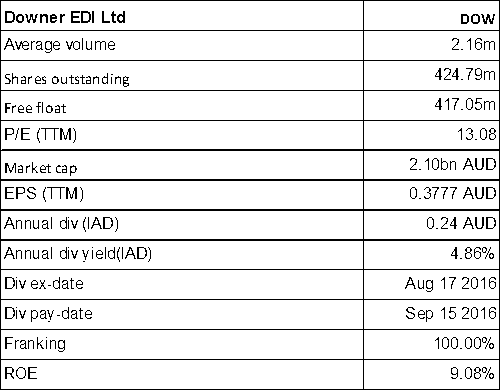

Downer EDI Limited

DOW Details

Results have beaten the expectation:Downer EDI Limited (ASX: DOW) has reported a net profit of $180.6m in FY 16, which is a 14.1% fall from the FY 15 but beat the expectation of the company’s own forecasts. The company’s cash conversion at 93% of EBITDA has been outstanding. DOW also signed a four-year contract extension with Karara Mining Ltd. Moreover, DOW was awarded one of the first construction contracts for the City Rail Link project, an underground rail line linking Britomart and the Auckland city center with the current western line near Mt Eden. DOW has also extended two-years’ contract to offer mining services at Stanwell Corporation’s Meandu Mine in South East Queensland. DOW has been awarded contracts by Western Australia’s Public Transport Authority (PTA) for the supply of an additional 10 x 3 car B Series units and for maintenance services on all “A” and “B” series commuter fleets at approximately $512 million. On the other hand, the Constellation Rail consortium (Downer and CRRC Changchun Railway Vehicles Co Ltd) did not succeed in its bid to deliver and maintain the New Intercity Fleet for Transport for NSW. Due to expensing the bid costs associated with the New Intercity Fleet, Downer’s NPAT target for the 2017 financial year is now lowered to $163 million from $170 million as announced on August 04, 2016. Meanwhile, DOW stock has risen 44.5% in the last six months (as of August 31, 2016). Despite this rise, the stock has a decent dividend yield and is trading at a lower P/E.

We give a “Hold” recommendation on the stock at the current price of $4.85

Ardent Leisure Group

.png)

AAD Details

Continued Expansion of Main Event & Turnaround for Bowling:Ardent Leisure Group (ASX: AAD) reported a core earnings growth of 11% to $62.4 million in FY16 while the revenue increased 15.6% to $687.6 million driven by growth across every division. The Main Event revenue increased by 21.6% and EBITDA is up 18.7% driven by expansion efforts and seven new centers in the year. The Bowling revenue grew 12.0% while EBITDA grew 30.3% as the group’s strategy to transition from solely bowling to a multi?attraction entertainment business gained momentum. The Theme Parks revenue is up 8.0% and EBITDA up 8.5% on the back of unique experiences and improved customer service. Moreover, AAD’s key driver is Main Event and the company has planned to open 11 centers in FY 17. The company would continue to implement the turnaround strategy for Bowling.

Financial Performance for FY 16 (Source: Company Reports)

Meanwhile, AAD stock has risen 23.4% in the six months (as of August 31, 2016), and we believe there is more upside left. The stock has a decent dividend yield and, we give a “Hold” recommendation on the stock at the current price of $2.55

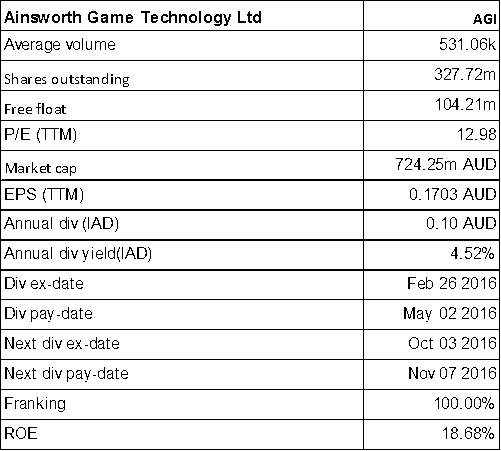

Ainsworth Game Technology Limited

AGI Details

Solid international markets growth: Ainsworth Game Technology Limited (ASX: AGI) has reported a profit after tax of $52.4 million in FY 16 on the same basis and in line with guidance provided as compared to the $52.5 million achieved in the previous corresponding period. The domestic revenue was $81.5 million (which is 29% of total revenue) and is 12% lower as compared to $93.0 million in the prior corresponding period. But, the overall sales revenue has increased by 19% to $285.5m for FY16 against prior corresponding period.

FY 16 Financial Performance (Source: Company Reports)

This reflects the strong underlying growth in international markets, which represented 71.5% of total revenue as compared to 61% in FY15. Moreover, AGI’s acquisition of Nova and a Class II product offering has enabled the company to leverage the technology for a better access to new markets in the Americas.

AGI has reported a 68% of segment profits from the Americas. AGI has made a good progress to date in delivering the expected synergies with Novomatic and would continue to focus on this through FY17. Trading at a reasonable dividend yield and a cheap P/E, we give a “Buy” recommendation on the stock at the current price of $2.17

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...