Wellard Ltd

WLD Details

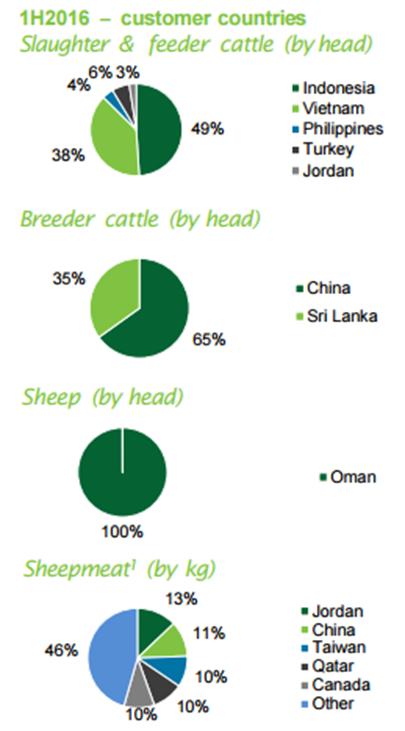

Positive growth prospects: Wellard Ltd (ASX: WLD) has signed a joint venture shareholder agreement with Fulida Group Holdings Co. Ltd and Zhejiang Aurora Agriculture Co. Ltd. as part of its China cattle investment. This marks a significant step in its China expansion and the company expects to break ground on the abattoir building in Q4 FY2016. In another positive development, the WLD’s vessels, MV Ocean Outback and MV Ocean Swagman which were out for repairs are fully operational now, thus making the full fleet of WLD operational before the upcoming high period of livestock demand.

International presence provides flexible business model (Source: Company reports)

In fact the M/V Ocean Shearer has concluded three days of sea trials. WLD recently reported half year results for the period ended December 31, 2015 with revenues of $275.5 million, an increase of 15.5% from the prior corresponding period. WLD reported a statutory net loss after tax of $23.9 million, primarily due to restructuring and IPO related costs.

The stock is currently down 29.09% (as of April 12, 2016) in the past three months but considering its growth prospects and addition to All Ordinaries Index and S&P/ASX 300 Index as per S&P Dow Jones Indices’ March quarter review, we recommend a “Speculative Buy” at the current price levels of $0.80

WLD Daily Chart (Source: Thomson Reuters)

3P Learning Ltd

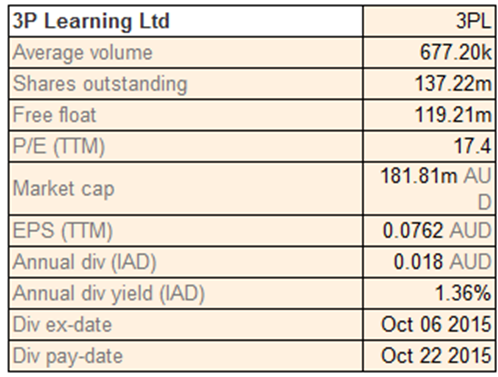

3PL Dividend Details

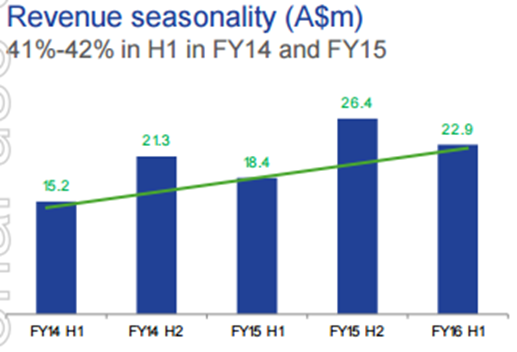

Unattractive opportunity: 3P Learning Limited (ASX: 3PL) announced results for the half year ended December 31, 2015 with a strong revenue growth 24% to $22.9 million compared to the prior corresponding period. 3PL saw revenue growth in all its global regions. The underlying earnings before interest, tax depreciation and amortization (EBITDA) was up 11% at $7 million while the reported net profit after tax (NPAT) decreased by a significant 22% to $3.2 million. There was a 31% increase in expense growth due to increased headcount, higher technology costs and World Education Games costs. The company faces seasonality issues that affects revenues.

Seasonality affects revenues (Source: Company reports)

3PL does not expect the EBITDA margin to grow in second half of FY2016 due to its ongoing investment in expanding sales channels and improving operating systems.

The company did not announce any interim dividend either. Although the stock has been added to S&P/ASX 300 Index as per S&P Dow Jones Indices’ March quarter review, 3PL is currently trading at unreasonably high price to earnings ratio (P/E) and we believe it is “Expensive” at the current price of $1.335

3PL Daily Chart (Source: Thomson Reuters)

Capilano Honey Ltd

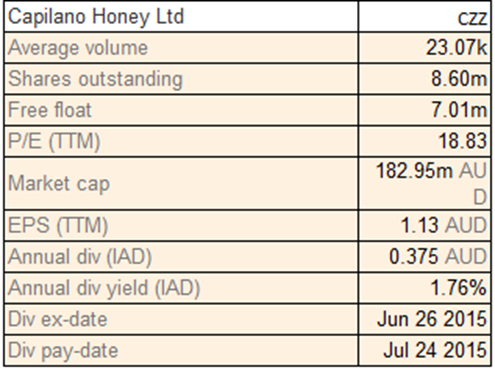

CZZ Dividend Details

Increased competition and supply pressure: Capilano Honey Limited (ASX: CZZ) has announced the forming of a joint apiary business with global natural health products company Comvita (NZX: CVT). This will help the company expand its operations and grow its supply base for premium quality honey while expanding its involvement in the international value chain. The company has previously announced 15% increase in revenue to $67.1 million for the half year ended December 31, 2015 and a significant 51% increase in net profit after tax (NPAT) to $7.77 million. However, CZZ is facing little supply side pressure due to sustained lower primary production and intense competition in the market. The average cost of supplier honey has increased by 22.34% to $5.64 per kilogram from the prior corresponding period.

CZZ stock is currently up 9.04% in the past one month (as of April 12, 2016) and has been added to All Ordinaries Index as per S&P Dow Jones Indices’ March quarter review. However, the stock is trading at a high price to earnings ratio (P/E) and hence we believe it is “Expensive” at the current price levels of $20.60

CZZ Daily Chart (Source: Thomson Reuters)

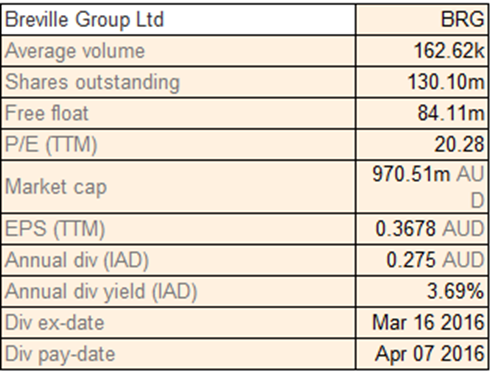

Breville Group Ltd

BRG Dividend Details

Global economic pressure: Breville Group Ltd (ASX: BRG) reported strong half year performance for the period ending December 31, 2015 with a 12.7% increase in revenue to $331.2 million and earnings before interest and tax (EBIT) growth of 5.7% to $46.1 million. BRG also announced an increased interim dividend of 14.5 cents per share.

.png)

Mixed global performance (Source: Company reports)

The North America business continued its strong growth with reported revenue increasing by 30.8% to $151.8 million compared to the prior corresponding period. This was a result of sustained growth in core categories of beverage and cooking, both for new and existing products of the company. Most of the other global regions faced pressure due to a strengthening US dollar.

Despite the overall strong performance, BRG’s future potential seems to be affected by the continued sporadic business conditions at a global level. Thus, we put a “Hold” recommendation for the stock at the current price levels of $7.58

BRG Daily Chart (Source: Thomson Reuters)

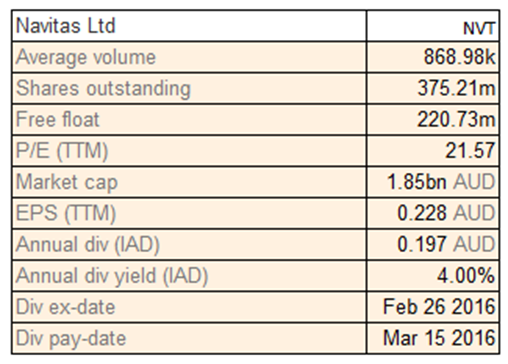

Navitas Ltd

NVT Dividend Details

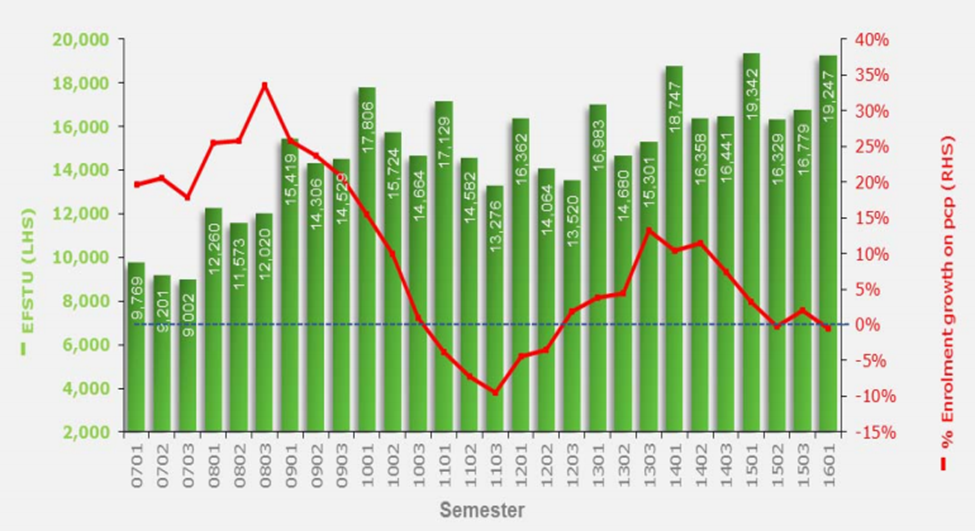

Mixed Enrolment Results: Navitas Ltd (ASX: NVT) has announced flat growth in its student enrolments in its University Programs division for the first semester of 2016. Enrolments in Australia and New Zealand colleges decreased by 6% mainly due to closure of two colleges and transition issues in another. NVT reported 12% increase in student enrolments for its university program colleges in US, UK and Canada. Enrolments in the UK faced some pressure due to demanding student visa policies and grew by just 3%, but the regulatory environment is now stabilizing.

Continued growth in enrolments (Source: Company Reports)

The company’s most recent partnership, with Florida Atlantic University witnessed a significant 27% growth in terms of enrolment over previous semester. NVT stock surged by 19.23% in the past six months (as of April 12, 2016). The company is expected to continue strong growth in most global areas. We recommend a “Hold” on this stock at the current price of $4.95

NVT Daily Chart (Source: Thomson Reuters)

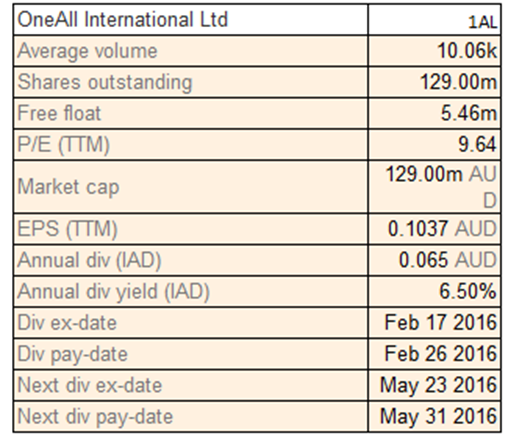

OneAll International Ltd

1AL Dividend Details

Weak financial performance given the challenging market conditions: OneAll International Ltd (ASX: 1AL) announced its FY2016 first half results with a net profit after tax (NPAT) of $4.106 million, down 12% from the previous corresponding period NPAT of $4.655 million. This decrease was despite an increase in revenue by 6% to $17.832 million from $16.834 million. 1AL faced significant administrative costs for the initial public offering (IPO) and increase in employee costs. The company declared an interim dividend of 4 cents per share. The recent first half dividend announcement of 2.5 cents now takes total dividend since listing to 6.5 cents unfranked. However, the company witnessed tough conditions in some of its key markets due to changing economic conditions and weakening of consumer sentiments. Sales were also affected because of depreciating currencies in Turkey and Brazil.

1AL is looking to focus on the US market, but its performance will continue to be affected by the weak market conditions in many regions. The stock has been added to All Ordinaries Index as per S&P Dow Jones Indices’ March quarter review but we believe that it is “Expensive” at the current price levels of $1.00

1AL Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2016 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

AU

AU

Please wait processing your request...

Please wait processing your request...