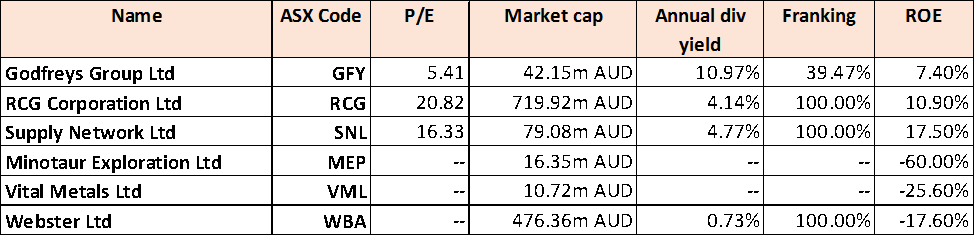

Godfreys Group Ltd

Efforts to revamp growth: Godfreys Group Ltd (ASX: GFY) is making revamping efforts to deliver growth post its weak FY16 performance. The group appointed Andrew Ford as its Chief Financial Officer. GFY is currently offering a stickvac product range whose performance is good. The group’s acquisition of The Service Company last year enhanced their commercial cleaning space penetration. GFY is rebalancing their store portfolio to hold a franchise-led model across half of their network, by enhancing their focus on smaller and regional locations. The group forecasts up to 60 corporate stores to be converted to franchise stores in the coming three years. The group recently appointed Andrew Ford as Chief Financial Officer. GFY stock rallied over 20.69% in the last three months (as of January 25, 2017). We give a “Speculative Buy” on the stock at the current price of – $ 1.05

RCG Corporation Ltd

Built a solid track record: RCG Corporation Ltd (ASX: RCG) had finished the acquisition of Hype DC in August 2016 enabling the group’s strengthen its position as a regional leader having over 380 stores and exclusive distribution rights to 11 iconic international brands. The group’s New Skechers distribution agreement has been extended for the term to 11 years. RCG expects to continue to deliver their solid performance and has issued a guidance of underlying annualized full-year Earnings before interest, tax, depreciation and amortisation (EBITDA) forecast of $90 million for FY17 while its FY16 underlying consolidated EBITDA was $60.4 million. The group generated an overall shareholder return of 665% for the last eight years till June 2016. Having a decent dividend yield and growth potential, we give a “Buy” recommendation on the stock at the current price of – $ 1.35

Supply Network Ltd

Rising dividends: Supply Network Ltd (ASX: SNL) reported an increase of fully franked interim dividend by 0.5 cents to 4.5 cents per share, which is payable in March 2017. The stock has a decent dividend yield. The group announced that based on unaudited management accounts, the group’s consolidated sales revenue is of the order of $47.7 million for the half year ended December 2016 while the Earnings before interest and tax (EBIT) for the half-year is forecasted to be over $4.4 million. Profit after income tax is forecasted to be over $3.0 million. For FY17, SNL forecasts a revenue of $95 million with EBIT expected to be around $8.5 million. The stock rose 2.57% on January 25, 2017. We give a “Speculative Buy” recommendation on the stock at the current price of – $ 1.99

Minotaur Exploration Ltd

Competitive exploration expenses against peers: Minotaur Exploration Ltd (ASX: MEP), a company in mineral sector, reported that they incurred an administration expense of only 15c for each $1 of exploration expense. MEP invested $5.6 million on total exploration investment and is aiming to maximize their exposure to exploration success. The group forecasts to incur $6 million to its projects through 2017 given its solid joint venture arrangements, which comprised 72% of the project activity in 2016. Among various exploration activities, the group is exploring along the Cloncurry mineral belt in Queensland and announced for first assays for Iris copper prospect. Then 2.7 km conducive trend at Eloise JV and copper-gold potential confirmation from Iris-Electra results, were other developments during the December quarter. Meanwhile, MEP stock fell over 36.67% in the last three months (as of January 25, 2017) placing them at attractive levels. We believe the stock is an “Ultra Speculative Buy” at the current price of – $ 0.076, in view of the existing prospects.

Vital Metals Ltd

High-grade gold zone at Kollo in Burkina Faso: Vital Metals Ltd (ASX: VML) encountered major intercepts of gold mineralization from the RC results at its Kollo Gold Project in Burkina Faso. The group intersected 17m @ 3.34 g/t Au from 145m while this zone promises a potential to generate high grades. As a result, VML intends to leverage their drill success and aims to proceed to find more targets. The group lately reported for finding more gold during RC drilling at Elephant Creek. VML stock rallied over 5.88% in the last four weeks (as of January 25, 2017) and we believe this momentum would continue in the coming months. We give a “Speculative Buy” recommendation on the stock at the current price of – $ 0.018

Webster Ltd

Improving conditions: Webster Ltd (ASX: WBA) reported that their area under annual summer crops might be 50% higher in aggregate during FY17 as compared to the last year. The group is currently forecasting decent normal plantings at Hay, Bourke and Garah. The Kooba aggregation was impacted by wet conditions while the planted area was cut from an expected 3,500 hectares to over 3,000 hectares. But Cotton prices were over 500 dollars per bale while the group sold over 50% of the expected production. As per the Kooba aggregation survey, the group is planning to double their irrigated area footprint in the coming three years through the conversion of previously water inefficient rice and pasture land into more productive row crop land. The group currently holds major core of water entitlements, which is estimated to be worth of over $320 million as of June 2016. WBA stock spiked up 14.2% in the last three months (as of January 25, 2017) while we give a “Hold” recommendation on the stock at the current price of - $ 1.36

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...