Spark Infrastructure Group

.png)

SKI Dividend Details

Regulatory outcomes expected to drive growth: Spark Infrastructure Group (ASX: SKI) recorded moderate full year 2015 financial results with standalone operating cash flow at $207.4 million, a marginal growth of 0.2% from previous levels. But, its underlying net profit after tax was down 6.6% to $119.7 million although they declared a final distribution of 6 cents per share in line with the full year guidance of 12 cents per share.

.png)

Distributions and guidance (Source: Company reports)

On the other hand, SKI management recently reported that theirStandalone OCF per security would improve for fiscal year of 2016 driven by the positive regulatory outcomes from Australian Competition Tribunal. VPN Final Determinations are forecasted by April 2016. We believe that there is further scope of a stock rally based on positive outlook, and therefore we recommend a "HOLD" rating on the stock at the current share price of $2.07

.PNG)

SKI Daily Chart (Source: Thomson Reuters)

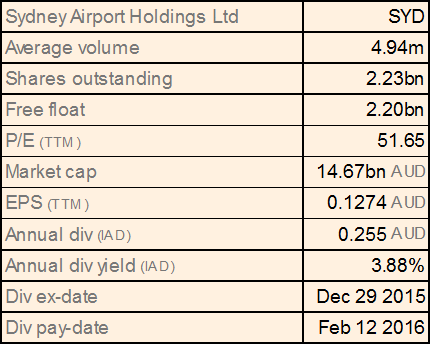

Sydney Airport Holdings Ltd

SYD Dividend Details

Improving traffic: Sydney Airport Holdings Ltd (ASX: SYD) recently released its traffic performance for the month of February 2016 with a total of 3.3 million passengers, which is an increase of 10% from same month a year ago. International and domestic markets recorded a growth of 12.7% and 8.5%, respectively.

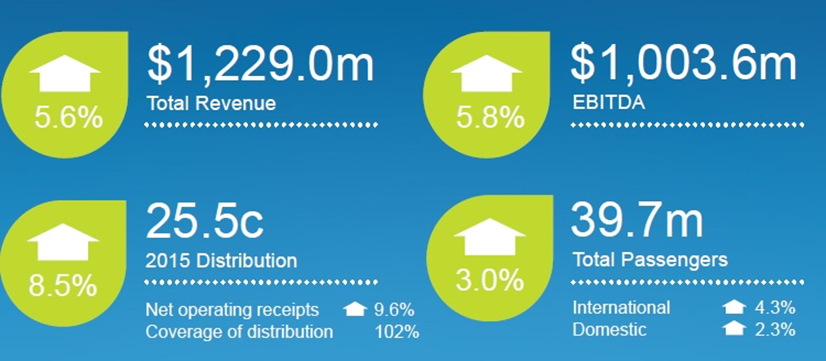

Strong 2015 performance (Source: Company reports)

Meanwhile, China Airlines expanded frequencies on their Taipei-Sydney route with the addition of a fifth weekly service operating from July 7 to October 28 on A330 - 300 with 306 seats, which would contribute to the group’s performance. Accordingly, the stock rallied over 7.26% during this year to date (as of March 30, 2016)placing them at very expensive valuations with a high P/E ratio. Hence, we recommend an "Expensive" rating to the stock at the current share price of $6.69

SYD Daily Chart (Source: Thomson Reuters)

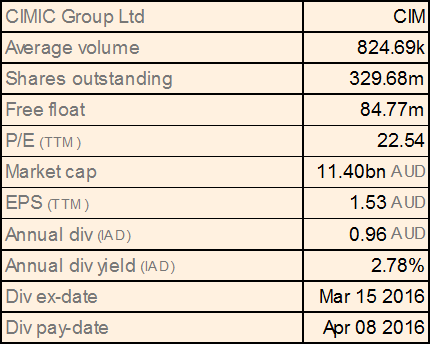

CIMIC Group Limited

CIM Dividend Details

Growing via acquisitions and new contracts: Cimic Group Ltd (ASX: CIM)recently reported that its CPB Contractors, got selected by GoldLinQ Pty Ltd as the preferred contractor to deliver stage two of the Gold Coast light rail project. The Queensland government has announced $420 million funding for Stage 2 which incorporates design and construction, and operations and maintenance through to 2029.

FY16 NPAT guidance (Source: Company reports)

Moreover, recently the company announced its compulsory acquisition of remaining shares in Sedgman Limited in which it already owns 90.08% relevant interest. As a result, the shares of CIM surged over 43.6% (as of March 30, 2016) in the last three months alone. However, we believe that this rally in the stock placed them at a high P/E ratio. Therefore, we suggest that the stock is "Expensive" at the current share price of $34.76

CIM Daily Chart (Source: Thomson Reuters)

Macquarie Atlas Roads Group

.png)

MQA Dividend Details

Rising distribution: For full year 2015, Macquarie Atlas Roads Group (ASX: MQA) reported a 3.5% increase in its revenue and 4.4% rise in EBITDA. Total traffic was higher by 2.9% led by growth across all portfolio assets. This strong performance of the group drove the group’s stock higher, which generated 17.11% in the last three months alone (as of March 30, 2016).

.png)

Growing distributions and guidance (Source: Company reports)

MQA recently declared a distribution of 9 cents per stapled security for the first half of 2016 compared to 6 cents in the same period earlier. We remain bullish on MQA and recommend a "HOLD" rating on this dividend yield stock at the current share price of $4.80

MQA Daily Chart (Source: Thomson Reuters)

Lend Lease Group

.png)

LLC Dividend Details

Generated double digit growth and issued a positive outlook: Lend Lease Group (ASX: LLC) recorded profit after tax of $353.8 million and earnings per stapled security of 60.9 cents, higher by 12% for the first half year ended December 31, 2015. LLC also registered a record pre sold revenues of $5.4 billion across residential apartments and communities, an increase of 49%. This indicates strong prospects for the firm which estimates a development pipeline end value of $46.6 billion, an increase of 15%. Construction backlog revenue rose 19% to $18.6 billion.

.png)

Earnings growth drivers (Source: Company reports)

Delivering a rise of almost 3.25% (as of March 30, 2016)in the past one month trading session but down 2.78% in the last five days, we believe that the stock is still trading at attractive P/E against its peers. Trading at a good dividend yield, we rate the stock a "HOLD" at the current share price of $13.87

.PNG)

LLC Daily Chart (Source: Thomson Reuters)

Transurban Group

.png)

TCL Dividend Details

Good performance but in oversold zone: Transurban Group (ASX: TCL) recorded a toll revenue growth of 19.3% while EBITDA growth stood at 14.6% for the first half of 2016 results. The company swung to net profit of $62 million compared to a net loss of $354 million in year ago period. Looking ahead, the company upgraded its distribution guidance to 45.5 cents per share for full year 2016, an increase of 13.8% from year ago period. Consequently, TCL stock has recorded gains of 7.25% this year to date (as at March 30, 2016) leading the stock at unreasonable P/E ratio.

Although the stock has been added in S&P /ASX 20 Index as per the S&P Dow Jones Indices’ March quarter updates, we believe that the stock is currently "Expensive" at the current share price of $11.35

TCL Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2016 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

AU

AU

Please wait processing your request...

Please wait processing your request...