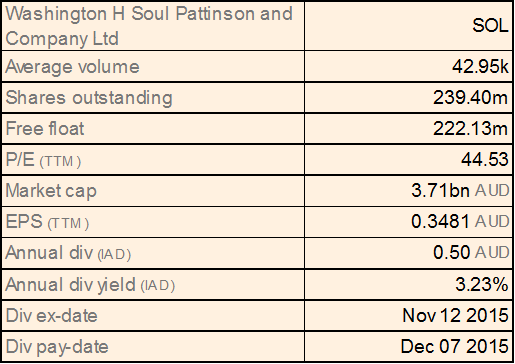

Washington H. Soul Pattinson and Co. Ltd

SOL Dividend Details

Improvement in profits but pressure continues: The shares of Washington H. Soul Pattinson and Co. Ltd (ASX: SOL) delivered a decent performance this year, generating over 13.22% (as of December 08, 2015) returns as the group reported a regular profit after tax attributable to shareholders increase by 27% year on year (yoy) to $156.4 million during fiscal year of 2015 as compared to $123.2 million in fiscal year of 2014. The group improved its fully franked final dividend by 3.4% to 30 cents per share for the full year of FY15. Meanwhile, the group’s regular profits from TPG Telecom, New Hope, Brickworks and Australian Pharmaceutical Industries improved by 30.5%, 19.8%, 15.2% and 24.3%, respectively, during the period. On the other hand, SOL reported a net loss from non-regular items of $73.1 million in FY15, as compared to a profit of $8.5 million, impacted by the group’s exposure in coal sector. New Hope twelve month movement (during FY15) fell by 36.3% while TPG Limited and API Limited twelve month movement rose by 72.3% and 165% respectively. We believe the group’s exposure in the resource sector might continue to hurt its bottom line given the volatile commodity market and challenging conditions.

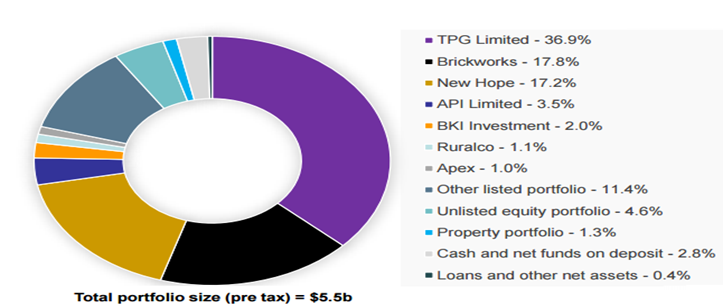

SOL’s Portfolio as of June 2015 (Source: Company Reports)

SOL is also trading at a very expensive valuation with a relatively higher P/E of about 44x.

The group’s stock declined over 2.64% (as of December 08, 2015) in the last four weeks and we believe the stock pressure might continue in the coming months. Accordingly, we place an Expensive recommendation on the stock at the current price.

SOL Daily Chart (Source: Thomson Reuters)

Magellan Financial Group Ltd

.png)

MFG Dividend Details

Ongoing funds under management performance: Magellan Financial Group Ltd (ASX: MFG) stock delivered outstanding performance this year and rallied over 50.42% (as of December 08, 2015) during this year to date boosted by its strong funds under management performance. During November 2015, the group delivered net inflows of $130 million, including net retail inflows into Global Equities strategies of $203 million, and net institutional outflows of $89 million. Meanwhile, the total funds under management slightly decreased to $39,949 million during November 2015 as compared to $40,488 million in October 2015. But, Magellan Global Fund generated returns of 29.5%, after fees, during the twelve months to 30 June 2015, which is above the MSCI World Net Total Return Index (AUD) by 4.9%. Magellan Financial Group also entered into new agreements with AMP and BT/Westpac to launch new funds in their respective platforms replicating the Magellan Global Fund, similar to the Colonial First State Magellan Global Fund Option (CFS) on the Colonial First State Platform (operated by Commonwealth Bank). Magellan Financial Group also reported a strong FY15 financial performance wherein revenues improved to $255.9 million as compared to $139.1 million in the last fiscal year.

.png)

Magellan Financial Group’s Funds under Management (Source: Company Reports)

Meanwhile, MFG stock surged over 10% in the last four weeks (as of December 08, 2015), and we believe this positive momentum might continue in the coming months. Based on the foregoing, we place a BUY recommendation on the stock at the current price of $24.87

MFG Daily Chart (Source: Thomson Reuters)

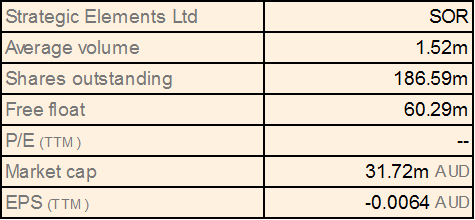

Strategic Elements Ltd

SOR Details

Focusing on Nanocube technology: Strategic Elements Ltd (ASX: SOR), the registered Pooled Development Fund designed to increase investment in Australian SMEs or the diversified financial company so to say, recently reported about its positioning at the forefront of establishing its Nanocube memory ink as one of the leading printable memory technologies. The company started testing on memory ink prototype, and results indicated data writing speed which is 1000 times faster than state of the art flash memory technology used in wearable devices and smart phones. Strategic Elements licensed the Nanocube memory ink technology from the University of New South Wales and intends to commercialize this high performance printed memory solution, which could be a major milestone for printed electronics. As a result, the shares of Strategic Elements bombarded by 466.67% (as of December 08, 2015) during this year to date. The group has been building a solid IP portfolio related to Nanocube memory technology via its 100% owned Australian Advanced Materials (AAM). SOR estimates to add four more patents to its Nanocube portfolio post which the group would have six patents. Earlier AAM also licensed the UVTM technology from UNSW. We believe that the stock would continue its positive momentum and accordingly, give a

BUY recommendation on the stock at the current price of $0.175

SOR Daily Chart (Source: Thomson Reuters)

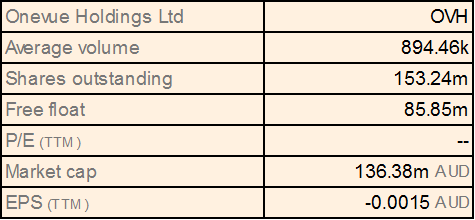

Onevue Holdings Ltd

OVH Details

Building Client Base: OneVue Holdings Ltd (ASX: OVH) shares exploded over 235.85% (as of December 07, 2015), boosted by its outstanding performance with group’s revenues surging over 92% in FY15. OVH has received commitments from institutional and sophisticated investors for $12.5 million through a share placement. The company would also be offering a share purchase plan to eligible shareholders to raise an additional $2.5 million. The group reported more than $1.1 billion growth of funds under management to >3 billion during FY15. OVH was recently selected by a major investment manager with over $1 trillion in assets under management globally, to offer a consolidated retail and institutional unit registry offering. The group would offer a branded retail and institutional unit registry site, with an entire automated service for their mFunds products.On the other hand, OneVue Holdings is also expanding its product range to target advised as well as non-advised investors. The group earlier won a five-year agreement from BNP Paribas Securities Services in Australia to offer unit registry services. Management intends to develop the Fund Services business to 80% by fiscal year of 2016 from the present 72%. OneVue Holdings also acquired Super Managers Australia Pty Ltd (SMA) for $5.2 million (including debt assumption), wherein all SMA Managers were to be rebranded to OneVue Superannuation Services by November 2015. Management estimates a better performance from its prospective LUMINOUS development releases. The company thus expects the transition pipeline to generate an incremental $5 million in additional annual run rate revenues while OVH announced that SMA revenues for FY16 are set to exceed $4 million.

Funds under Administration Performance (Source: Company Reports)

Meanwhile, OVH stock continued to rise and delivered over 71.15% in the last four weeks (as of December 07, 2015). However, we believe that this heavy stock rally placed the shares in overbought zone. Therefore, we give an Expensive recommendation on the stock at the current levels, and would review the stock at a later date.

OVH Daily Chart (Source: Thomson Reuters)

MyState Ltd

MYS Dividend Details

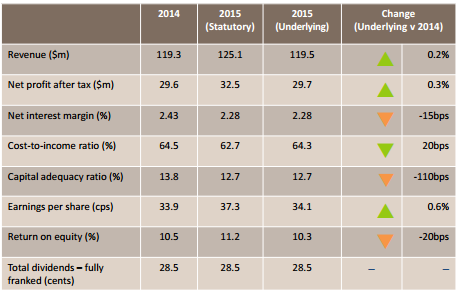

Improvement in revenue and lending book velocity underpinning growth: MyState Ltd (ASX: MYS) reported its result for FY 2015 with a growth of 0.2% in underlying revenues of $ 119.5 million, a 0.3% growth in underlying net profit after tax of $ 29.7 million, and a 15 basis point decline in net interest margin of 2.28%. MYS’s stable earnings are set to lay the foundation for FY16 growth. The company also reported a drop in cost to income ratio of 20 basis points at 64.3%, a 110 basis points drop in capital adequacy ratio to 12.7%, a growth of 0.6% in EPS to 34.1 cents per share and a 20 basis points drop in return on equity to 10.3% for FY15. Fully franked total dividends amounted to 28.5 cents per share. The statutory earnings include $ 39 million profit from sale of non-strategic assets, Cuscal shares, to support growth and reinvestment; less $ 1.1 million in restructuring and related costs.

FY15 Results (Source: Company Reports)

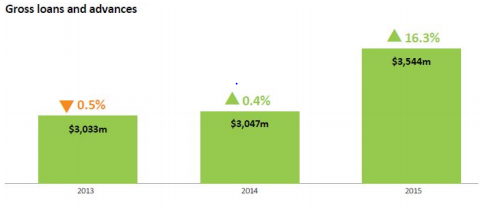

The company continues to focus on strategic priorities. These include growth in revenue drivers with record settlements at 75% over the previous year and restored loan book growth of 16.3% at 2.3x system. Another is simplifying processes with third parties and direct channels with the successful deployment of the new loan origination system LendFast and continuing on further product simplification and digital technology upgrades. The already sound capital ratio of 12.7% has been further enhanced through the issue of $ 25 million Tier 2 notes after the year end. Credit quality continues to be a cornerstone with bad and doubtful debts and arrears at continuing low levels. Under the transforming capabilities, the first mobile app for IOS and Android has been launched. Improvement has been reported for the Tasmanian economy and business confidence is high with private investment spending showing solid gains during the financial year after a period of weakness. The labour market also continues to improve. On the other hand, Australian economic growth remains subdued but confidence is returning as the economy is adjusting to the decline in resources investment and the weaknesses in commodity prices. Business confidence has proved to be more robust and housing outlook remains positive with some contraction in credit growth expected in the coming years.

Gross Loans and Advances (Source: Company Reports)

We note that the capture position of the company remains well above the industry average and that the competitive landscape between major banks and smaller financial services companies has become a more level playing field. The stock has fallen about 4.86% this year to date (as at December 08, 2015) and we think that the prospects of this company are bright and rate the stock as a Speculative Buy at the current price of $4.49

MYS Daily Chart (Source: Thomson Reuters)

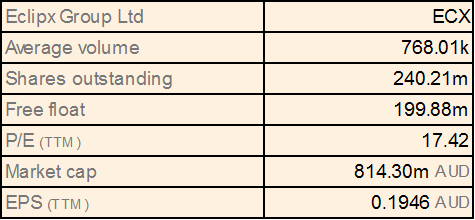

Eclipx Group Ltd

ECX Details

FY15 Profit Exceeding Prospectus Forecast: For FY 2015, Eclipx Group Ltd (ASX: ECX) reported cash net profit after tax and amortisation of $ 48.6 million which is a growth of 33% over the same period of the previous year and exceeding the prospectus forecast of $ 47 million. New Business Writings during the year was $ 841 million indicating an increase of 35% since 30 September 2014, while representing a robust pipeline for future revenue. Assets under Management or Financed amounted to $ 1.77 billion, which is an increase of 12% since 30 September 2014. Acquisition synergies and the use of technology helped to support a reduction in cost to income ratio to 50% down from 61% in the previous year. Further, growth initiatives include establishing a Commercial Equipment Finance division and a funding partnership with the Clean Energy Finance Corporation. The board has announced a maiden fully franked final dividend of 6.5 cents per share for the second half of FY 2015 which on an annualised basis is within the payout ratio range of 60% to 70% presented in the IPO prospectus.

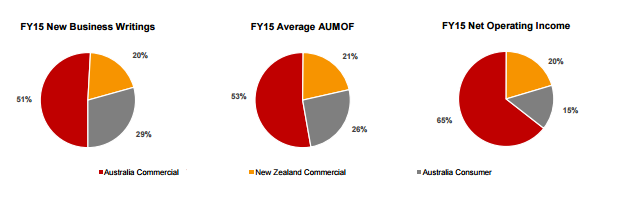

Segment-wise Performance (Source: Company Reports)

The Australian commercial fleet and equipment finance business continued to generate positive momentum with a 55% increase in new business writings to $ 428 million and total assets under management or financed closed the year at $ 920 million because of new customers and the expansion of existing relationships. In December 2014, the company started its Commercial Equipment Finance business to leverage its core competency and the business contributed $ 44 million in new business starting from scratch. The New Zealand Commercial Fleet segment showed new business writings growth of 22% finishing with $ 166 million in new business and fleet assets under management or financed grew by 11% to $ 374 million.

However, despite the good results and the stock rising 10.42% in the last three months (as at December 08, 2015), we believe that the stock is overvalued at its current price and therefore expensive.

ECX Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

AU

AU

Please wait processing your request...

Please wait processing your request...