A2M Details

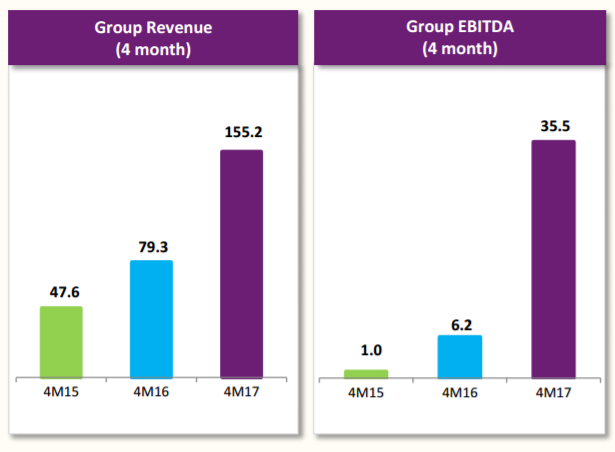

Overall weak sentiment in the sector: a2 Milk Company Ltd (Australia) (ASX: A2M) stock recovered over 1.3% on December 16, 2016 while falling about 6.9% in the last five days (as of December 16, 2016). Infant formula makers have been under pressure since the time Bellamy's Australia Ltd (ASX: BAL), the group’s major competitor, released a weak update regarding their China’s business. Bellamy’s reported that they would witness temporary volume dislocation until regulatory registrations are completed in China. Therefore, the Brands that are not expecting to get registration are offloading their inventory at discounted prices, which seem to hurt the performance of imported brands of infant formula providers. Therefore, BAL stock lost about 38.6% in the last four weeks alone (as of December 09, 2016). This update has been hurting the infant formula maker’s sentiment in Australia. On the other hand, A2M had issued a decent trading update regarding its performance in China a few days ahead of Bellamy’s update. The group’s year to date revenue for FY17 indicated a seasonal build for their major China sales event 11/11 Singles Day. A2M reported an EBITDA/Sales rise to 22.9%, for four months to FY17 indicating the group’s ongoing positive performance in infant formula sales. A2M reported that they would continue to invest in their brand to enhance their business growth. The China CFDA infant formula registration process progress is on track while a2MC and Synlait Milk is progressing with documentation. Registration is needed by January 01, 2018. A2M continues to develop multi-product, multi-channel strategy (Mother Baby stores, e-commerce channels) for China’s market.

a2 Milk Company performance (Source: Company Reports)

Strong FY16 Performance: The group reported 127.4% revenue growth for FY16 while net profit after tax saw a turnaround to profit from FY15 loss. The gross margin growth of 177.5% reflected change in product mix, with infant formula being the largest component of sales.

Stock Performance: Although there is no major update from a2 Milk Company, updates from its competitor Bellamy's Australia have been constantly hurting the infant formula maker’s stock in Australia. Moreover, Bellamy's Australia is under trading suspension now and is expected to resume trading on December 21, 2016. BAL will be releasing another major update and market is forecasting a weak update from the group. Given these sentiments and rising competition from brands who are trying to clear their stock, demand for A2M products in China might come under pressure. A2M also invested heavily on business development in China adding to its costs. On the other side, A2M stock has rallied about 96.1% in last one year (as of December 16, 2016). The stock is currently trading at higher valuations and we believe investors can book profits in the stock given the uncertainty ahead. We give a “Sell” recommendation on A2M at the current price of – $ 2.01

A2M Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...