Australia and New Zealand Banking Group Limited

Announcement of Dividend: Australia and New Zealand Banking Group Limited (ASX: ANZ) has recently disclosed its distribution payment of AUD 1.9130 with the total dividend distribution rate of 3.7743% per annum for ANZPD - CAP NOTE 6-BBSW+3.40% PERP NON-CUM RED T-09-21 and it will be paid on September 2, 2019 with the record date of August 23, 2019.Moreover, the bank had made an announcement about new management structure for its Australia business. As a result, the current group executives Mark Hand and Maile Carnegie would be sharing responsibility for the financial performance of ANZ’s business in Australia. Mark Hand is placed as Group Executive Australia Retail and Commercial Banking while Maile Carnegie would be taking on an expanded role as Group Executive Digital and Australia Transformation. These changes would take effect from March 1, 2019.

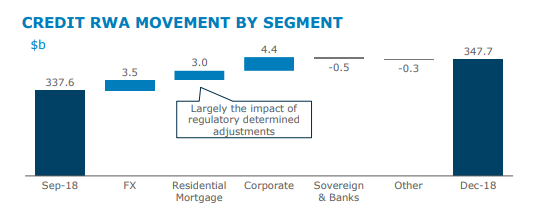

The bank had earlier released its APRA APS330 report covering quarter ended December 31, 2018. Its credit quality was stable with provision charge amounting to $156 million which is below the FY2018 quarterly average. The bank’s loss rate stood at 10 bps while in 1Q FY 2018 it was 14 bps. The common equity tier 1 (CET1) of ANZ stood at 11.3% at December quarter end. Also, in 1Q FY 2019, with respect to credit RWAs, the bank witnessed an increase of $10 billion which includes more than $4 billion in lending primarily in the corporate asset class. However, other movements consist of foreign exchange impacts, regulatory determined adjustments with respect to mortgages as well as improvement in portfolio risk profile.

Credit RWA Movement by Segment (Source: Company Reports)

Analysing Strategic Priorities of ANZ: The bank’s priorities are to reduce the operating costs and risks by removing the complexity and exiting low return and non-core businesses as well as focusing on the areas where ANZ can win. The other strategic priorities are driving the purpose and values led transformation as well as building more convenient and engaging banking solutions.

Stock Recommendation: On the monthly chart of ANZ, Exponential Moving Average or EMA has been used and default values were used for the purposes. It was observed that the stock price has crossed the EMA and moved upwards after the crossover which suggests that the stock price might witness a rise moving forward.

On the other hand, bank’s annual dividend yield stood at 5.76% which is higher than the industry median (financials) of 5.4%.Also, from the valuation perspective, the ANZ seems to be little undervalued as its EV/Sales ratio stood at 4.1x as compared to the industry median of 4.9x.

Considering the above-mentioned factors, we maintain our “Buy” rating on the stock at the current market price of A$27.750 per share.

Commonwealth Bank of Australia

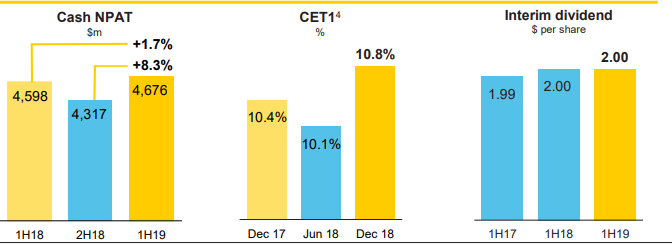

A Look at Recent Update: Commonwealth Bank of Australia (ASX: CBA) Equity Products Group happens to be an issuer of instalment warrants over ordinary shares in Rio Tinto Limited (RIO) having the ASX Codes RIOIYE. On February 27, 2019, RIO made an announcement about fully franked special dividend amounting to $3.387 per ordinary share. The record date happensto be March 8, 2019. CBA Structured Investments would be applying cash proceeds of special dividend amounting to $3.387, 100% franked dividend together with the interest refund, where applicable, towards the reduction of the loan amount with respect to RIO instalment warrants. With respect to 1H FY 2019 results, the bank had delivered robust core business outcomes amidst the challenging period. The bank ended 1H FY 2019 with operating income amounting to $12,408 million reflecting a fall of 1.9% as growth in volumes got offset by lesser NIMs, lower markets and fee income as well as the impact of weather events. The bank declared interim dividend per share of $2.00.

Key Outcomes (Source: Company Reports)

What to Expect From CBA: The bank’s transformation to become a simpler, better bank is ongoing. The bank would be taking action to address the issues, earn trust and become a better bank for the customers. They are also strengthening risk management, deploying towards core business growth and working to deliver long-term sustainable returns for the shareholders.

Stock Recommendation: On the daily chart of CBA, Exponential Moving Average or EMA has been applied by using the default values. After observation, it was noticed that the stock price has crossed the EMA and moved upwards after the crossover demonstrating that the bank’s stock might witness a rise moving forward.

From the valuation perspective, the bank is having an EV/EBITDA of 7.0x as compared to the industry median (financials) of 10.7x reflecting that bank is slightly undervalued. Therefore, it seems to be a decent buy opportunity.

On the back of above factors coupled with a decent outlook, we maintain our “Buy” rating on the stock at the current market price of A$74.680 per share.

Bank of Queensland Limited

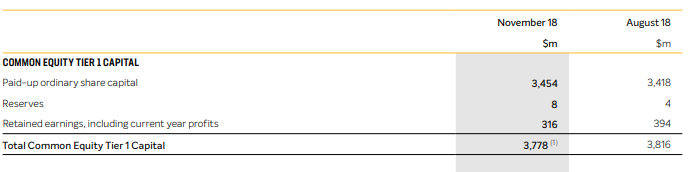

APRA Basel III Disclosures: The capital management strategy of Bank of Queensland (ASX: BOQ) focuses on ensuring the maintenance of adequate capital levels to protect deposit holders. As at November 30, 2018, common equity tier 1 capital ratio stood at 9.1% while, as at 31 August 2018, it was 9.3%. However, as at November 30, 2018, the total capital ratio stood at 12.6% while, as at 31 August 2018, it was 12.8%. For the quarter ended November 2018, the bank’s total common equity tier 1 capital amounted to $3.77 billion as compared to August 2018 quarter end of $3.81 billion. The fall was primarily due to reduction in retained earnings (including current year profits).

Common Equity Tier 1 Capital (Source: Company Reports)

Guidance Related to Key Metrics: The bank had provided an update with respect to trading conditions for the half year ending February 28, 2019 (or 1H 2019). The bank would be declaring the results for 1H FY 2019 results on April 11, 2019. Considering the January year-to-date performance, cash earnings after tax for 1H FY 2019 is expected to be between $165 million-170 million as compared to $182m generated in 1H FY 2018. The decline in income from 1H FY 2018 is mainly because of non-interest income which is expected to be $8 million-10 million lower than the 1H FY 2018 level of $75 million. However, in 2H, there are expectations that the market conditions would remain challenging.

Stock Recommendation: On the daily chart of BOQ, Exponential Moving Average or EMA has been used and default values were used for the purposes. After observation, it was noted that the bank’s stock price had crossed the EMA and had moved upwards after the crossover which reflects that the stock price might witness a rise moving forward.

Also, the bank’s capital position remains robust with 1H common equity tier 1 ratio expected to be more than 9.1% reported in the November 2018 quarter Pillar 3 disclosure.

Considering the above factors, we maintain our “Buy” rating on the stock at the current market price of A$9.190 per share.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...