Stocks’ Details

Corporate Travel Management Limited

Market Update: Corporate Travel Management Limited (ASX: CTD) is a provider of travel management services to the corporate market. As on 14 May 2020, the market capitalization of the company stood at $1.2 billion. In a recent update, the company stated that it remains in a strong liquidity position amid COVID-19 outbreak. Further, its existing banking group has agreed to a waiver of all financial covenants for CY2020, which included the removal of COVID-19 from MAE definition. Total facility reduced from £125m to £100m, with facility term maturity to remains through August 2022. As on 7 May 2020, net cash amounted $30 million.

Other Recent Updates: Recently, the company stated that Invesco Australia Limited, a substantial holder of the company, has reduced its voting power from 11.99% to 10.84%. In another update,the companystated that it has suspended its FY20 outlook due to increased uncertainty for COVID-19 pandemic.

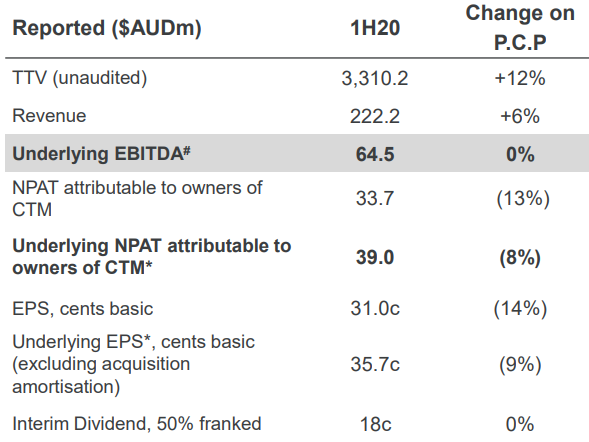

1H20 Financial Performance: During 1H20, the total transaction value of the company went up by 12% to $3,310.2 million and revenue witnessed an increase of 6% to $222.2 million. This reflects the strength and resilience of the business in the macro conditions. In the same time span, the company renewed its financed facility and reduced its total drawn debt.

1H20 Financial Performance (Source: Company Reports)

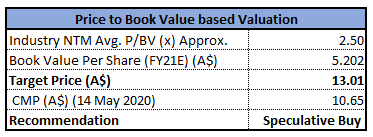

Valuation Methodology:P/BV Multiple Based Relative Valuation (Illustrative)

P/BV Multiple Based Approach (Source: Refinitiv, Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: The stock of the company gave negative returns of 44.56% over a period of six months and is currently trading below the average of its 52-week trading range of $4.355 - $25.8.The company has an annual dividend yield of 3.64%, with a P/E ratio of 14.88x.While the travel restrictions due to the virus might pose some short-term uncertainty in the business, the company expects to recover the current activity levels in due time. CTD rides on clients wins at consistently high levels. Considering the trading levels, decent financial performance, and strong liquidity position, we have valued the stock using P/B multiple based illustrative valuation method and arrived at a target price with an upside of lower double digit (in percentage terms). Hence, we recommend a ‘Speculative Buy’ rating on the stock at the current market price of $10.65, down by 3.182% on 14 May 2020.

iCar Asia Limited

Trading Update: iCar Asia Limited (ASX: ICQ) is involved in the development of internet-based automotive portals in South East Asia. On 14 May 2020, the company stated that its unaudited revenue on a year to date basis until April 2020 stood at $4.3 million. This represents a rise of 18% year over year despite COVID-19, driven by the company’s used car business and Thailand. The company witnessed net operating cash outflow of only $0.4 million in April 2020, as a result of effective cost control and successful implementation of cash collection initiatives.

Future Growth Impetus: With continuous improvement in performance across all countries, the company is set to attain a strong cashflow position, going forward. The outlook for the second quarter of 2020 remains strong and the company expects to begin improvement in its two largest markets, Malaysia and Thailand, with relaxation of movement and business restrictions.Further, the company expects to reopen its offices in both the countries with staff on a rotation system, while maintaining social distancing in the office. However, in Indonesia, the company expects movement and business restrictions to continue until 22 May 2020.

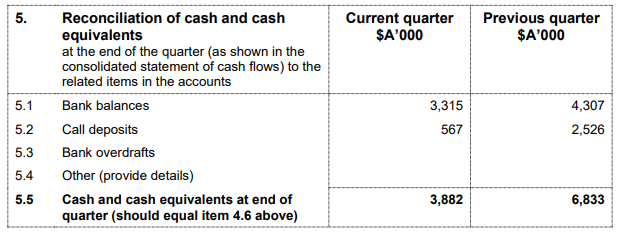

Quarterly Results for the Period ended 31 March 2020: The company exited the period with cash balance of $3.882 million. Net cash used in operating activities stood at $2.698 million, whereas cash used in investing activities came in at $253K.

Cash Highlight (Source: Company Reports)

Stock Recommendation: The stock of the company corrected by 34.21% in the last three months and is currently trading below the average of its 52-week trading range of $0.125 - $0.480. The stock of ICQ closed at $0.265 with a market capitalization of ~$106.78 million. On the valuation front, the stock is trading at an EV/Sales multiple of 6.5x as compared to the industry average of 11.5x on TTM (Trailing Twelve Months) basis. Considering the above factors along with future growth momentum, and progress across all areas of operations, we give a “Speculative Buy” recommendation on the stock at the current market price of $0.265, up 6% on 14 May 2020.

Flight Centre Travel Group Limited

FLT Agrees to Sell St Kilda Road Property: Flight Centre Travel Group Limited (ASX: FLT) is mainly involved in travel retailing in the leisure and corporate travel sectors. On 7 May 2020, the company agreed to sell its Melbourne head office property to Shakespeare Property Group for a consideration of $62.15 million. The divestment is expected to complete in July 2020. The company had bought the property at 436 St Kilda Road for $32 million in 2008.

FLT Completes Retail Entitlement Offer: On 6 May 2020, the company announced the successful completion of its retail component of its 1 for 1.74 accelerated pro rata non-renounceable retail entitlement offer of new fully paid ordinary shares. The offer raised $138 million at $7.20 per share. Proceeds from the offering will be utilised to strengthen the company’s balance sheet and liquidity position.

Cost Reduction Initiatives: In another update, the company stated it is making steady progress towards the cost cutting strategies and is reducing its global cost base towards the $65million per month target by the end of July 2020. Despite COVID-19 outbreak, which has resulted in heavy travel restrictions worldwide, the company continues to generate some sales, with TTV tracking at ~5-10% of normal levels in April 2020.

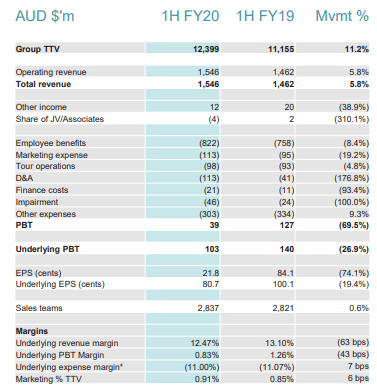

1HFY20 Key Highlights for the Period Ended 31 December 2019: During the period, the company’s revenue went up by 5.8% year over year and came in at $1,546 million. Group TTV stood at $12,399 million, up 11.2% year over year, due to solid growth across all regions. Underlying PBT, however, dropped 26.9% on a year over year basis.

Key Highlights (Source: Company Reports)

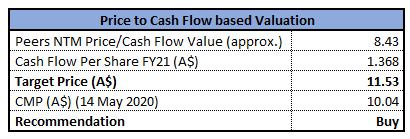

Valuation Methodology:P/CF Multiple Based Relative Valuation (Illustrative)

P/CF Multiple Based Relative Valuation Approach (Source: Refinitiv, Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: As per ASX, the stock of FLT is inclined towards its 52-weeks’ low level of $8.56, proffering a decent opportunity for accumulation. The stock has corrected ~70.19% and ~71.76% in the last three months and six months, respectively. The company has an annual dividend yield of 13.33%. Despite the current challenges put forward by COVID-19, the company aims for both operational and financial stability in the long-term. Considering the trading levels and decent financial performance, we have valued the stock using P/CF based illustrative relative valuation method and have arrived at an indicative target price with an upside of lower double digit (in percentage terms). For the purpose, we have taken peers such as Corporate Travel Management Ltd (ASX: CTD), Helloworld Travel Ltd (ASX: HLO), Qantas Airways Ltd (ASX: QAN), to name few. Considering, the above factors and current trading levels, we recommend a ‘Buy’ rating on the stock at the current market price of $10.04, down by 2.995% on 14 May 2020.

Comparative Price Chart (Source: Refinitiv,Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

AU

AU

Please wait processing your request...

Please wait processing your request...