Costa Group Holdings Ltd

CGC Details

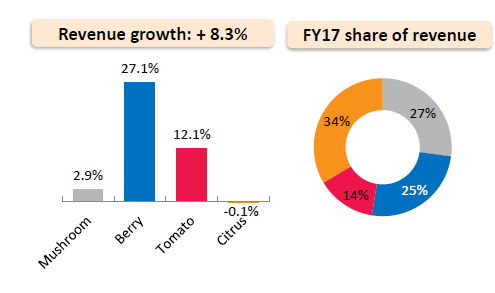

Strong trading conditions: Costa Group Holdings Ltd (ASX: CGC) reported for a robust first half result with strong cash flow generation, balance sheet position and growth capacity. Although the unseasonal weather led to delay in cropping, there has been no major negative weather impact. There has been 9% growth in revenue over 1H FY16 while EBITDA before SGARA and material items (EBITDA-S) reflected a growth of 26.6% to $49.0m. The NPAT before SGARA and material items (NPAT-S) was $24.0m reflecting a 35.7% growth while statutory NPAT of $15.0m was reported against $0.0m in 1H FY16. Mushroom segment performance was robust driven by consistent production and a favourable sales mix with increased retail sales.

Financial result for Produce (Source: Company Reports)

Further, Blueberry performance witnessed a 75% production increase over 1H FY16. 2016 calendar year citrus crop was lighter than expected, but fruit was of exceptional quality. For tomato, 1H outcome was good with the category trading in line with expectations. CGC also reported that final royalty income from the US 2016 season has been above expectations. The group has been witnessing solid trading over January-February period with all portfolio units contributing well. The stock has risen 5% at the back of the strong result and is trading close to its 52-week high price. We give a “Hold” recommendation at the current price of $ 3.77

.png)

CGC Daily Chart (Source: Thomson Reuters)

Mayne Pharma Group Ltd

MYX Details

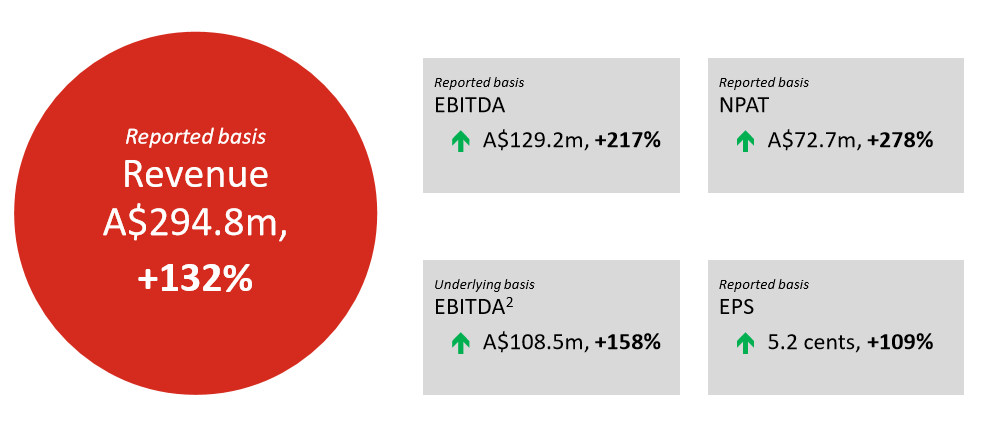

Spectacular half year 2017 result: Mayne Pharma Group Ltd (ASX: MYX) has reported its 1HFY17 revenue of $294.8m indicative of an increase of 132% over 1HFY16. The reported EBITDA of $129.2m has been up 217% on 1HFY16 while the underlying EBITDA of $108.5m is up 158% on 1HFY16. There has been a solid 278% rise in the reported net profit after tax of $72.7m while earnings per share of 5.2c have been up 109% on 1HFY16. The strong result came at the back of Teva product acquisition contributing significantly to growth with sales and margins performing ahead of guidance. MYX has reported that Dofetilide capsules have exceeded Pfizer’s Tikosyn® brand volume within 10 weeks of launch. Although the Specialty Brands Division encountered headwinds in the first quarter from the loss of exclusivity on Doryx 50mg and 200mg, the division managed to have a strong second quarter. The group has been said to be positioned appropriately for growth driven by acquisitions and product launches, and has thus, commented for a strong outlook.

Financial Performance (Source: Company Reports)

Despite the above update, the stock fell 2% on February 24, 2017. Given some sector-driven economic uncertainty and stock trading levels, we believe that the stock is still “Expensive” at the current price of $ 1.47

.png)

MYX Daily Chart (Source: Thomson Reuters)

Graincorp Ltd

GNC Details

Expects rise in full year earnings: Graincorp Ltd (ASX: GNC) recently announced that the group Chairman, Don Taylor has indicated his intention to retire and thus the group is putting transition arrangements in place. The role will be taken up by director Graham Bradley AM. Further, GNC aims to release its half yearly results in May 2017. The group expects to report FY17 underlying EBITDA in the range of $385 million to $425 million which is above the FY16 figure of $256 million. FY17 underlying NPAT is expected to be of the order of $130 million to $160 million over FY16 figure of $53 million. These are said to be driven by record eastern Australian crop and continued solid performance from GrainCorp Malt. However, factors such as 2H17 volumes, timing of grain export program and freight bookings, global crush margins, and foreign exchange movements may have an impact on the result. The stock is trading at a high level. We maintain our “Expensive” recommendation at the current price of $ 9.06

GNC Daily Chart (Source: Thomson Reuters)

RCG Corporation Ltd

RCG Details

Robust half year result but downgrade in guidance: RCG Corporation Ltd (ASX: RCG) reported a strong half year results entailing a rise of 42% in underlying consolidated EBITDA of $42.9m on the prior year. The underlying NPAT of $23.3m surged 34% on the prior year. The underlying diluted EPS of 4.3 cents per share surged 17% on the prior year. The group has increased the fully franked interim dividend of 3.0 cents per share, on the prior year. In fact, there has been a 116% increase in cash generated from operations of $36.8m. The result has been supported by the acquisitions of Hype DC and the Accent Group. However, the stock fell 17.26% on February 24, 2017 as RCG downgraded the underlying annualised full year EBITDA guidance to $85m-$88m from $90m. This came at the back of challenging trading conditions that the group has witnessed since Boxing Day. On the other hand, continuous boost from the Accent Group’s performance, Skechers brand, and strong product pipeline are expected to bring a balance. Further, RCG reported for improved conditions for February trading while business is targeting full-year LFL sales growth of 6%. We maintain a “Buy” recommendation at the current price of $ 1.15

RCG Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...