Crown Resorts Ltd

.png)

CWN Details

Responded to the enquiries regarding its international VIP program play business:Crown Resorts Ltd’s (ASX: CWN) stock fell over 20.2% in the last four weeks alone (as of October 24, 2016) following reports that 18 staff members were detained in China. On the other hand, the group has responded to the enquiries regarding its international VIP program play business. As per the latest updates from CWN, around a third of the group revenues are generated from overseas visitors but only some of these overseas visitors participate in international VIP gaming programs. The visitors are from a range of regions including South East Asia, North Asia (including mainland China), Europe and the Middle East. Moreover, in FY16, around a quarter of the CWN’s revenues were from the international VIP gaming programs. Less than half of the revenue of international VIP gaming programs is from the mainland China.

.png)

Financial Performance for FY16 (Source: Company Reports)

On the other hand, this segment of the business represents only 12% of the Crown Group revenues in FY16.

Additionally, CWN is continuing to enhance its Australia portfolio while Crown’s portfolio is well-recognized having premium branded assets. We give a “Hold” recommendation on the stock at the current price of $10.40

CWN Daily Chart (Source: Thomson Reuters)

Skycity Entertainment Group Limited

.png)

SKC Details

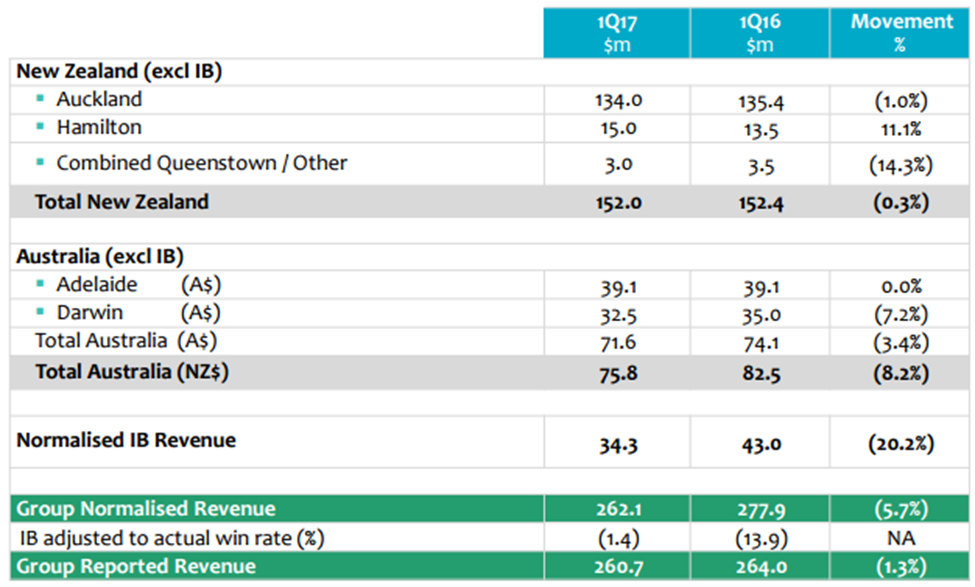

Weak first quarter Performance: Skycity Entertainment Group Limited (ASX: SKC) reported a 5.7% fall in the group normalized revenue in the 1Q FY 17 due to the below-trend Auckland gaming activity and IB turnover coupled with ongoing difficult trading conditions in Darwin as well as appreciation of the NZ$ versus A$. The group EBITDA margin is also down impacted by decrease in the revenue, especially in Darwin and IB. But, Auckland is expected to return to growth for the remainder of FY17 and Hamilton is expected to continue to trade strongly, due to the increased gaming activity.

Financial Performance for 1Q FY 17 (Source: Company Reports)

However, the challenging trading conditions are expected to continue in Darwin over the near-term and IB activity would weaken further after the recent developments in China.

Meanwhile, SKC stock has fallen 21.67% in the last three months (as of October 25, 2016), and still, we give an “Expensive” recommendation on the stock at the current price of $3.55

SKC Daily Chart (Source: Thomson Reuters)

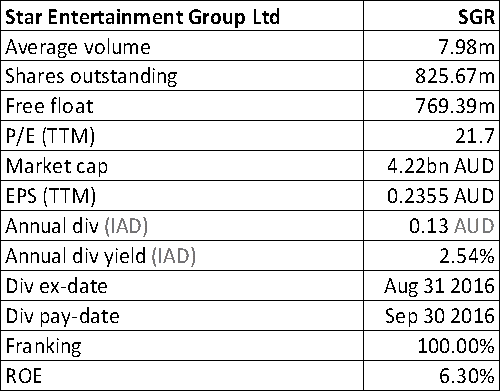

Star Entertainment Group Ltd

SGR Details

Granted the new casino license: Star Entertainment Group Ltd (ASX: SGR) has been granted the new casino license by the Queensland Government, under which the casino operations are permitted to start after the completion of the Integrated Resort at Queen’s Wharf Brisbane. The casino license will be issued to a joint venture entity (Destination Brisbane Consortium) of which The Star Entertainment Group has a 50% interest, by making a payment of $213 million to the Queensland Government.

On the other hand, concerns on declining tourism from China led the SGR stock fall by 15.78% in the last one month (as of October 25, 2016). We believe that the stock is “Expensive” at the current price of $4.97

SGR Daily Chart (Source: Thomson Reuters)

Donaco International Ltd

.png)

DNA Details

Turnaround from Loss to Profit in FY 16: Donaco International Ltd (ASX: DNA) is set to hold its AGM on November 24, 2016. The group recently announced for the purchase of shares by Thai Partner. The last 12 months ended 30 June 2016 (FY16) have witnessed a good transformation phase and significant growth in scale with the addition of DNA Star Vegas.

.png)

Transformation of Donaco’s Operations (Source: Company Reports)

DNA has reported 602.6% growth in revenue to 143,385,778 in FY 16 which reflects the contribution from Star Vegas and the profit grew 2736.8% to $77,208,54. The earnings per share (diluted) reported 9.29 cents in FY 16 from the loss per share of 0.52 cents in FY 15. In addition, Star Paradise expansion to introduce new Thai junkets and players would offer further recurring revenue from FY17.

DNA has given the maiden dividend of 1 cents per share in FY 16. DNA also has a strong balance sheet with $78.2 million cash. Trading at a cheap P/E, we give a “Buy” recommendation on the stock at the current price of $0.435

DNA Daily Chart (Source: Thomson Reuters)

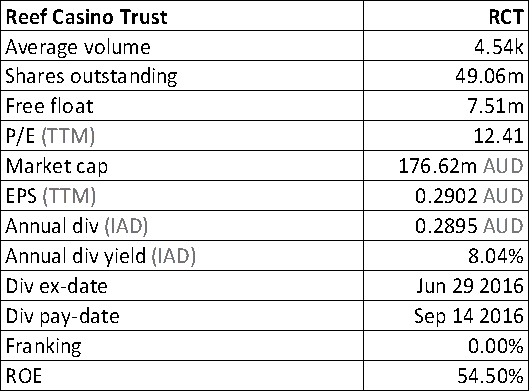

Reef Casino Trust

RCT Details

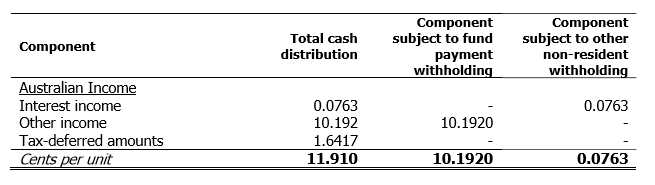

Project L1 approved and to be completed in December 2016:Reef Casino Trust (ASX: RCT) reported for 3.5% drop in revenue from ordinary activities for six months ended June 30, 2016 to $11.15 million while the distributable profit dipped 7.9% to $5.9 million. The group earlier announced for a record distributable profit growth of 24% in 2015 over the respective previous year. The group has now increased its interest only loan facility of $11.5 million to $13.5 million extending to 31 January 2019. For the first four months of this year, the group had reported for lower electronic gaming revenues compared to 2015 while premium revenue also slipped compared to the same period last year due to a lower premium play win rate. Project L1, which is said to be an exciting investment and renovation project, is aimed at driving growth partly in 2016 but mainly beyond 2016. The project has now been approved and will be completed in December 2016, and is said to cost $6.5 million. Accordingly, the group has enhanced its banking facility. The stock has surged only 2.86% in last six months (as at October 24, 2016).

Components for distribution for six months ended June 30, 2016 (Source: Company Reports)

Given the current market scenario, group’s growth potential and stock trading at a slightly high P/E, we believe that the stock is “Expensive” at the current price of –

RCT Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...