SKYCITY Entertainment Group Ltd

.PNG)

SKC Details

Weak first quarter FY17 update: SKYCITY Entertainment Group Ltd (ASX: SKC) disappointed the investors with their first quarter of 2017 update wherein revenues were reported to be falling by 5.7% compared to the same period of last year. Declining trend in Auckland gaming activity and IB turnover, coupled with ongoing weakness in Darwin led to the weak performance. In New Zealand, Auckland revenue fell 1.0% impacted by declining gaming visitation as well activity from premium players. Australia Revenue (excluding IB) fell over 8.2% during the quarter with Adelaide revenue being flat. Darwin revenue lost 7.2% impacted by difficult local economic conditions. SKC had monitored events concerning Crown employees being detained in China, and stated that it does not have any office in China and its contractors have not been questioned or detained. However, the group expects an adverse impact from the situation over short-to-medium term. The group lately revealed about many changes with regards to its management and also announced for changes in Senior Manager’s relevant interests. Graeme Stephens has been appointed as Group CEO and Luke Walker as GM Adelaide Casino. For FY14-16, the group followed a policy of distributing at least 80% of normalized NPAT in dividends to shareholders per annum.

.png)

First quarter of 2017 (Source: Company Reports)

The group plans to have its interim results teleconference call on February 09, 2017. SKC stock fell over 20.7% in the last six months (as of January 27, 2017) while we maintain our “Expensive” recommendation on the stock at the current price of – $ 3.72

SKC Daily Chart (Source: Thomson Reuters)

Tatts Group Ltd

.PNG)

TTS Details

Not in favor of the Pacific Consortium’s proposal: Tatts Group Ltd (ASX: TTS) reported that the group did not really find the Pacific Consortium’s acquisition proposal (led by Macquarie Group) superior to Tabcorp’s merger proposal. The group believed that the acquisition proposal from Tabcorp Holdings was better than Pacific Consortium’s offer of $4.40 to $5.00 of cash and shares per TTS share. Tabcorp tabled an offer of $4.34 per share with an intention to acquiring all of Tatts’ businesses and creating a gaming giant worth $11.3bn. TTS stock fell over 3.9% in the last four weeks (as at January 27, 2017) and we believe this pressure might continue. In fact, the group expects a 13.8% fall in their Lotteries EBITDA for the first half of 2017 against the prior corresponding period. Further, TTS net debt has been said to be about $1.2 billion. This in fact was not considered appropriately in Pacific Consortium’s acquisition proposal. Trading at a higher P/E, we give an “Expensive” recommendation on the stock at the current price of - $ 4.33

.png)

TTS Daily Chart (Source: Thomson Reuters)

News Corp

.PNG)

NWS Details

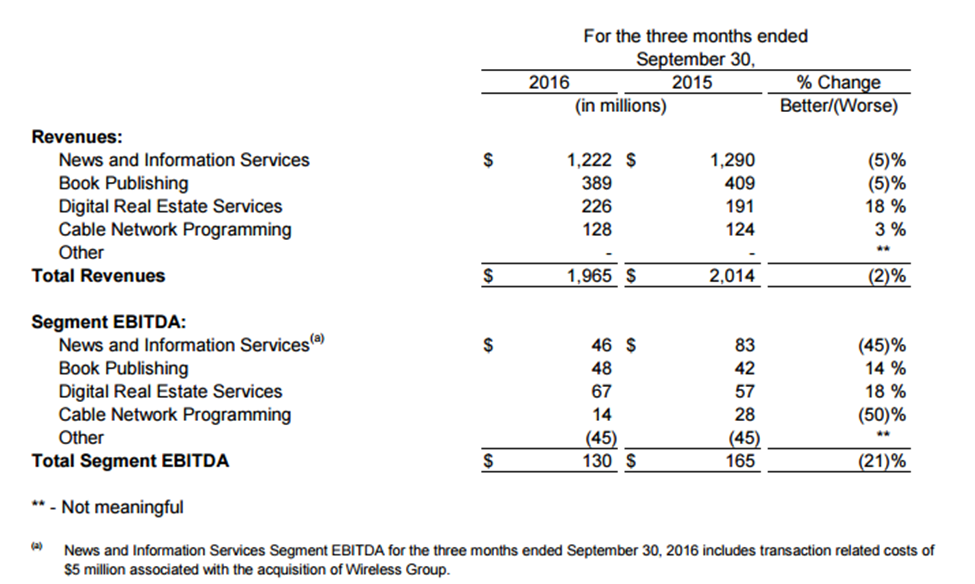

Core performance pressure despite growing digital revenues: News Corp (ASX: NWS) reported a solid Digital Real Estate Services segment revenue rise by 18% during the September quarter of 2016 (first quarter of FY17) against the prior corresponding period. Digital revenues enhanced to 24% of News and Information Services segment revenues, against 20% in the same period of last year. On the other hand, the group’s overall revenue performance continued to face pressure, with the revenues falling to $1.97 billion in the September quarter of 2016 against the $2.01 billion in the prior year.

Segment performance during the September quarter (Source: Company Reports)

The group’s income from continuing operations was nil during the quarter from $143 million in the prior year. Moreover, advertisers and readers are now preferring digital opportunities which would continue to hurt the print industry. NWS stock corrected over 6.5% in the last six months (as of January 27, 2017) and we believe this pressure would continue. It was also noted that ACCC did not oppose NWS proposed acquisition of APN’s Australian Regional Media Division (ARM) unit. Given the performance pressure, we give an “Expensive” recommendation on the stock at the current price of – $ 16.64

.png)

NWS Daily Chart (Source: Thomson Reuters)

Myer Holdings Ltd

.PNG)

MYR Details

Improvements under new strategy: Myer Holdings Ltd (ASX: MYR) recently reported that legal proceedings have been served against it by a former shareholder, TPT Patrol Pty Ltd, wherein TPT Patrol alleged loss and damage resulted from statements made in the Company’s full year FY2014 results. This is said to be identical to the group action against MYR by Melbourne City Investments Pty Ltd (MCI), as per the group. In December 2016, the Supreme Court of Victoria held that the MCI proceedings were an abuse of process; and in view of the same, MYR denies any liability and aims to defend against TPT Patrol’s allegations. Meanwhile, the group reported for having more than 850 new or upgraded wanted brand destinations under its new strategy. Further, there has been a 7.2% improvement in Net Promoter Score in Flagship and Premium stores driven by service investment while there is 74% growth in omni-channel sales. MYR’s FY16 NPAT was also said to be in line with guidance. The group’s Q1 FY17 sales were up 0.6% and 1.6% on a comparable stores basis. Given the competitiveness in the sector and other developments while benefits are yet to be seen fully from new strategy, we believe that the stock is still ‘Expensive’ at the current price of $ 1.25

.png)

MYR Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...