Kathmandu Holdings

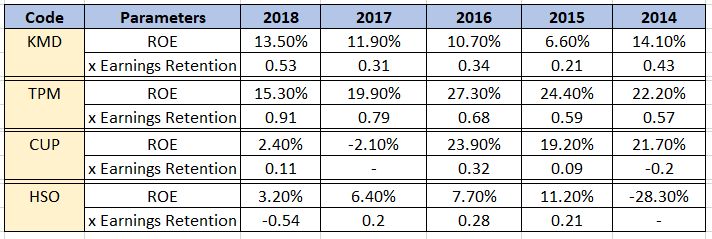

Robust Performance in FY 18: Kathmandu Holdings Ltd.’s (ASX: KMD) stock has risen 25.22% in three months to A$2.89 as on September 18, 2018 after the company for FY 18 delivered 32.9% rise in NPAT to record NZ$50.5m. This is on the back of 30.9% increase in EBIT to NZ$74.6m and 11.7% growth in Sales to NZ$497.4m. The company reported 9.6% growth in sales in Australia, which is the company’s largest market. KMD has enhanced its gross margin by 1.4% points to 63.4% in FY 18, which is above the long-term target range of 61% to 63%. Moreover, in 2018 KMD has generated record operating cash flow of NZ$75.6m, and had invested NZ$16.7m in capital projects, mainly for the expansion and updating the store network. Additionally, in FY 18, KMD had acquired Ob?z, which is a premium US based outdoor footwear brand. The acquisition will enhance the international growth and transform the company from an Australian retailer to a global outdoor apparel and equipment brand. Meanwhile, KMD stock is trading at a reasonable P/E of 13.11x. The company’s stock has support at level of $2.52 and resistance at $3.02. Based on the foregoing, we give a “Hold” recommendation on the stock at the current price of $ 2.89.

TPG Telecom

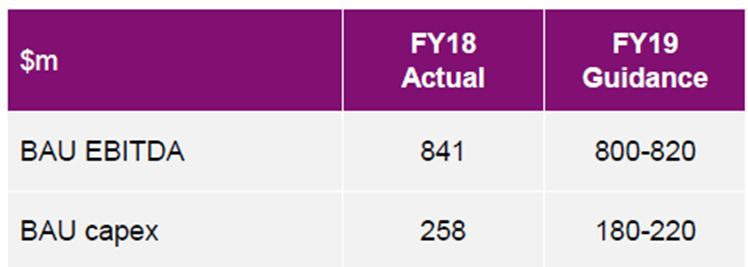

Subdued outlook for FY 19: TPG Telecom Ltd.’s (ASX: TPM) stock fell 5.39% to A$8.25 on September 19, 2018 after the company for FY 18 has reported 0.5% growth in revenue to $2.5 billion, which is about $31 million below consensus and flagged subdued outlook for FY 19. However, in FY 18 there is a 0.7% increase in underlying earnings before interest, tax, depreciation and amortisation (EBITDA) to $841.1 million, which is ahead of the company’s guidance of $825 million to $830 million. The EBITDA rose despite DSL customers migrating to lower margin NBN services, loss of gross profit from home phone services as the customers migrated to NBN bundled services and increase in the electricity price. Moreover, for FY 19, TPM expects gross profit margin will be further affected as the customers of DSL and home phone services continue to migrate to the NBN, and also by a one-time step reduction in EBITDA caused due to adoption of the new AASB15 revenue accounting standard. Additionally, TPM has planned merger with Vodafone Hutchison Australia, which is subject to satisfaction of certain conditions precedent to it. Now, the prospects are tethered on the merger with Vodafone that can generate significant synergies. Meanwhile, TPM stock has risen 56.83% in three months as on September 18, 2018 and is trading at a P/E of 20.37x. The stock has support at level of $6.70 and resistance at $9.30. Based on the foregoing, we give a “Hold” recommendation on the stock at the current price of $ 8.25.

FY 19 Guidance (Source: Company Reports)

Countplus

Undergoing Restructuring:Countplus Ltd.’s (ASX: CUP) stock has fallen 2.90% to A$0.67 in one month as on September 18, 2018 after the company for FY 18 has reported 10% fall in the revenue to A$74,386,000 and 66% fall in the net profit after tax to (A$176,000). The company is undergoing transformation and there is significant restructuring of the group over the past 18 months. EBITA results in 2018 is of $4,522,000 (includes the restructuring costs of $684,000 at a firm level compared to $6,366,000 in 2017). Meanwhile, CUP has support at level of $0.62 and resistance at $0.765. Based on the foregoing, we give a “Hold” recommendation on the stock at the current price of $ 0.67.

Healthscope

Resilient Performance in FY 18: Healthscope Ltd.’s (ASX: HSO) stock has fallen 11.26% in three months as on September 18, 2018 after the company for FY 18 has reported 19.4% decline in the statutory NPAT (after Non-Operating Expenses) to $89.4m, impacted by Non-Operating Expenses of $75.4m (net of tax). However, in FY 18, the group’s revenue grew by 3.7% to $2,340.8m. The Hospitals Revenue rose 4.3% to $2,100.6m. HSO’s Group Operating EBITDA fell by 4.4% to $375.9m and the Hospital Operating EBITDA fell by 4.1% to $344.7m, which was at the top end of revised guidance to be in the range of $340m-$345m. Meanwhile, HSO has improved operating efficiency with Group Hospitals Best Practice Program to deliver $6m in cost savings ($10m annualised). Additionally, HSO is expecting FY19 Hospital Operating EBITDA growth to be at least 10% compared with FY18. On the other hand, HSO has support at level of $2.03 and resistance at $2.57. As of now, we give a “Hold” recommendation on the stock at the current price of $ 2.06.

Comparative Analysis (Source: Company Reports and Thomson Reuters)

Earnings Retention* is indicative of percentage of net income retained to grow the business and is opposite of dividend payout ratio

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...