Wattle Health Australia Ltd (ASX: WHA)

WHA Details

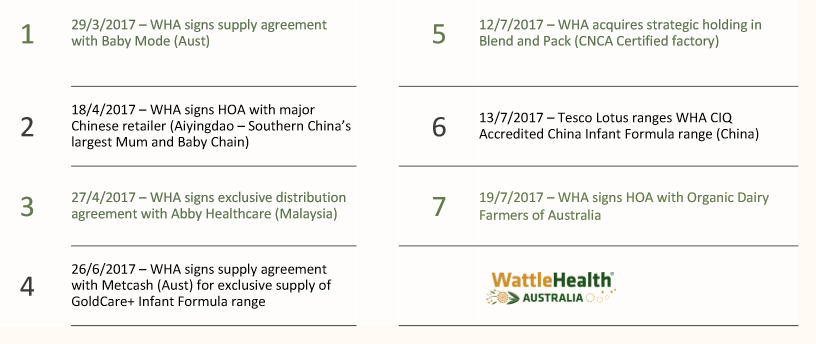

Targeting one of the largest consumer dairy markets in South East Asia: Wattle Health Australia, a consumer food product company, was listed on ASX in March this year. The group had successfully completed a placement of shares and raised $9.6 million, which was oversubscribed. Based on the response, WHA also offered an additional $3.3 million worth of shares subject to shareholder approval. WHA’s full year revenue was $928,426 with net loss of $4,150,944 (at the back of a one-off expense during IPO). Meanwhile, WHA acquired a 5% equity interest in Blend and Pack Pty Ltd together with Mason food.

WHA’s Key Milestones (Source: Company Reports)

On the other hand, the group has been granted a 10-year importation and wholesale license in Vietnam. The group has successfully incorporated its Vietnam subsidiary, and these moves collectively will help the group in selling its baby food and nutritional dairy products in the country post seeking appropriate registrations. This will enable WHA to get access to one of the largest consumer dairy markets in South East Asia. In last six months, the stock has moved up 370% (as at September 14, 2017), and is trading at slightly higher levels (surged 2.3% on September 15, 2017). Further, the industry landscape is quite competitive with players such as Bellamy’s Australia Ltd (ASX: BAL) and a2 Milk Company Ltd (ASX: A2M). We give an “Expensive” recommendation at the current price of $ 0.90

WHA Daily Chart (Source: Thomson Reuters)

Superloop Ltd (ASX: SLC)

SLC Details

Strategic move for expansion: Superloop recently announced about its move to snap up NuSkope (a fixed wireless internet services provider in South Australia) and associated entities RA-WIFI and RA-ADSL (together NuSkope). The strategic acquisition’s consideration includes $7.0 million in cash and $3.0 million in Superloop shares at an issue price of $2.457. This move has been expected to expand SLC’s reach in the Adelaide market. NuSkope had reported customer revenue of over $7.1 million for the 2017 financial year (up from $4.1 million for the 2016 financial year) and adjusted EBITDA of over $2.4 million against $1.6 million for 2016. SLC has also indicated about further investments for expanding into the SA network. Earlier, Superloop announced that it has acquired all the issued shares of SubPartners. In terms of financial performance, Superloop reported an encouraging FY17 result with 755% rise in revenue from ordinary activities and an improvement in net loss after tax by $6 million over FY16. SLC’s result has been driven by strong sales in Singapore and expansion moves on its Australian business. During FY17, the group had completed the acquisition of BigAir Group Limited, expansion of the Singapore network to strategic locations, rollout of Project Red Lion in Singapore, and construction and commissioning of Hong Kong’s TKO Express domestic submarine cable, among other developments. Both Hong Kong and Singapore have benefited from some non-recurring revenue in 2H17. At the back of the result, SLC declared its maiden dividend. However, the group has indicated for an increase in capital expenditure with the on-going development in Hong Kong, Singapore and Australia, and this needs to be watched out given the group being in its early stages of forming its Asian business. We give an “Expensive” recommendation at the current price of $ 2.57

.PNG)

SLC Daily Chart (Source: Thomson Reuters)

Navitas Ltd (ASX: NVT)

.JPG)

NVT Details

Extension of partnership with Swansea University:For FY17, Navitas had reported an NPAT slip of 10.8% to $80.3 million while revenue from ordinary activities of $955.2 million was down 5.5% against FY16. Net operating cash flow was reported to be $101.53 million compared to $125.81 million of FY16.

.png)

Group’s Repositioning Strategy (Source: Company Reports)

On the other hand, the group has expanded its agreement with Swansea University through the college, the International College Wales Swansea (ICWS). Under the new agreement, the college will shift from a traditional royalty based pathway model to a JV between the company and the University, to be known as the College, Swansea University. The operations of ICWS will be transferred to the JV entity and will be equally owned by the company and Swansea. In last six months, NVT stock has risen over 8% (as at September 14, 2017) while facing some pressure at the back of softness in FY17 results. NVT’s Careers & Industry earnings are still expected to get an impact from AMEP retender going forward. On the other hand, the new partnership with Swansea University is expected to be a profitable one for the group. The group is also expected to benefit from growing demand for education services and anticipates 18% group EBITDA margin as its 2020 growth target. Given the trading scenario in view of price to earnings ratio and the recent updates, we put a “Hold” at the current price of $ 4.36

.PNG)

NVT Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...