Stocks’ Details

Bank of Queensland Limited

Improved Guidance to Aid Better Business Prospects:Bank of Queensland Limited (ASX: BOQ) operates in banking, financial and related services. Recently, BOQ announced a change in the interest of one of its Directors, named Warwick Martin Negus, purchased 5,000 shares on 3 December 2019 and 5 December 2019 each at a price consideration of $7.55 and $7.50 per ordinary share, respectively. As per a recent announcement, BOQ announced that it will hold its 2019 Annual General Meeting (AGM) on Tuesday, 10 December 2019.On 26 November 2019, BOQ announced its successful completion of the fully underwritten $250 million institutional share placement.

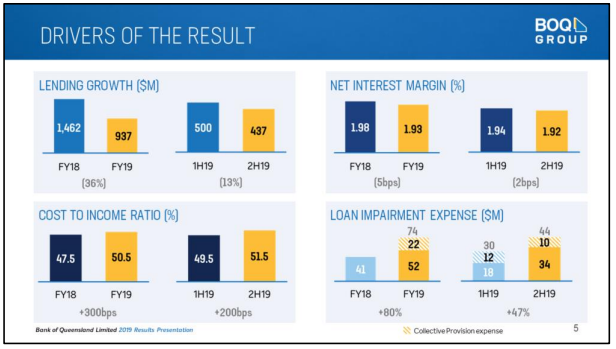

FY19 Operational Highlights for the period ending 31 August 2019: BOQ declared its FY19 financial results, wherein the company reported net interest income of $961 million as compared to $965 million in FY18. The bank reported a profit for the year at $298 million in FY19, lower than $336 million in FY18. Cash earnings after tax were reported at $320 million, down 14% on y-o-y basis. Common Equity Tier 1 ratio came at 9.04%, down 27bps on y-o-y basis. Cash earnings per share decreased 16% on y-o-y basis at 79.6c. Total capital adequacy ratio, during the year, stood at 12.4%. The bank reported a net interest margin of 1.93% in FY19 as compared to 1.98% in FY18.

FY19 Operating Highlights (Source: Company Reports)

Guidance:The bank is well-positioned for ‘unquestionably strong’ in 2020 and awaits clarification from the regulator on the revised risk weighting framework, which is due to be implemented in 2022. The Board has set the target for Common Equity Tier 1 Capital between 8.25% and 9.5%, and Total Capital target is set to be in the range of 11.75% and 13.5%.

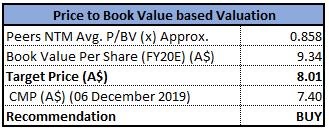

Valuation Methodology: P/BV Multiple Approach

P/BV Based Valuation (Source: Thomson Reuters), *NTM: Next Twelve Months

Stock Recommendation: The stock of BOQ is quoting at $7.40, with a market capitalization of ~$3.3 billion. The stock is trading at the lower band of its 52-week trading range of $7.380 and $10.770. The stock has generated negative returns of 17.93% and 20.21% in the last three months and six months, respectively. The bank is well-positioned to face the clarification from the regulator on the revised risk weighting framework. The business is targeting Common Equity Tier 1 Capital between 8.25% and 9.5% and Total Capital target between 11.75% and 13.5%. Considering the aforesaid facts, we have valued the stock using one relative valuation method, i.e., price to book value multiple and arrived at a target price of higher single digit (in % terms). Looking at the price movements, current trading levels, completion of institutional placement, business prospects and valuation, we recommend a ‘Buy’ rating on the stock at the current market price of $7.40 as on 06 December 2019.

Australia and New Zealand Banking Group Limited

Improvement in Housing Segment:Australia and New Zealand Banking Group Limited (ASX: ANZ) offers diversified financial products to the retail and corporate clients. Recently, the company reported a change in Director’s interest, where Shayne Cary Elliott has acquired 30,012 shares.

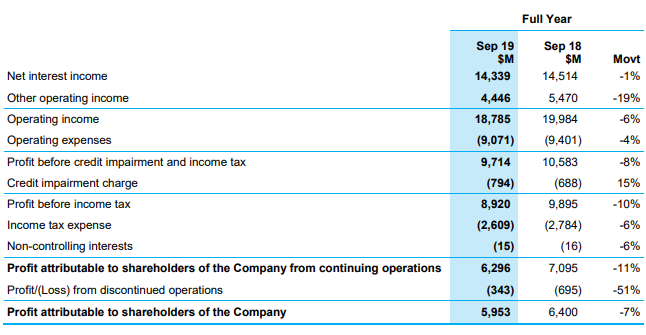

FY19 Financial Results for the period ended 30 September 2019:ANZ declared its full-year results for FY19, wherein the company reported statutory operating income from continuing operations at $18,785 million, down 6% on y-o-y basis. The business reported cash profit at $6,161 million, up 6% on y-o-y basis. Net interest income of the bank came in at $14,339 million, down 1% from FY18. Net interest margin of the business stood at 1.75%, down from 1.87% in FY18. Operating expenses to average assets improved to 0.97% from 1.05% in FY18. During the year, the company reported migration of more than 60,000 users onto a new Institutional customer self-service platform, providing access to all transaction accounts, payments and foreign exchange in one place.

FY19 Operating Highlights (Source: Company Reports)

Guidance:Management is focusing on improving its capital efficiency, primarily for the New Zealand segment. The company expects that the housing market across Australia is on the verge of slow recovery and expects operational improvement from the segment. Geopolitical tensions are likely to put pressure on earnings on the backdrop of global trade exposure of the business, while BOQ is planning to manage through the diversification of business.

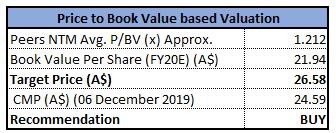

Valuation Methodology: P/BV Based Multiple Approach

P/BV Based Valuation (Source: Thomson Reuters), *NTM: Next Twelve Months

Stock Recommendation:The stock of ANZ is quoting at $24.590 with a market capitalization of ~$70.01 billion. The stock has delivered a negative return of 8.11% and 11.82% in the last three-months and six-months, respectively. During FY19, operating expenses to average assets stood at 0.97%, up from 1.05% in FY18. Considering the aforesaid facts, we have valued the stock using one relative valuation, i.e., price to book value multiple and reached a target price of higher single-digit (in % terms).Looking at the current price movement, trading levels, valuation and improving housing scenario Across Australia, we recommend a ‘Buy’ rating on the stock at the current market price of $24.59, down 0.486% as on 06 December 2019.

Commonwealth Bank of Australia

Q1FY20 Reported Cash NPAT up 5%:Commonwealth Bank of Australia (ASX: CBA) operates in banking activities and provides financial services. Recently, the bank informed that it has become a substantial holder with 5.11% voting power in Inghams Group Limited.

Q1FY20 Operating Highlights for the period ended 30 September 2019: CBA announced its first-quarter results for FY20, wherein the company reported a statutory net profit of approximately $3.8 billion, which included a $1.5 billion gain on sale of CFSGAM (Colonial First State Global Asset Management). The business reported cash net profit from continuing operations of ~$2.3 billion. The business reported 2% higher operating expenses on y-o-y basis on account of higher staff costs and IT amortisation. The business reported Loan Impairment Expense of $299 million during the quarter. The business reported a decent CET1 ratio of 10.6% after 2019 final dividend payments. The business reported a decent funding position with deposit funding at 69% and the Net Stable Funding Ratio at 112%.

Q1FY20 Operating Highlights (Source: Company Reports)

Valuation Methodology: P/BV Based Multiple Approach

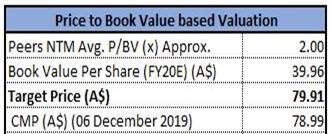

P/BV Based Valuation (Source: Thomson Reuters), *NTM: Next Twelve Months

Stock Recommendation: The stock of CBA is quoting at ~$78.99 with a market capitalization of $139.18 billion. The stock has generated a negative return of 0.79% and 0.97% in the last three-months and six-months, respectively. At the current market price, the stock is quoting at the upper band of its 52-week trading range. The stock is available at a price to book multiple of 1.9x on NTM (Next Twelve Months) basis as compared to the industry average of 2.0x.Looking at the current trading levels and valuation, and other aforesaid facts, we have a wait and watch view on the stock at the current market price of $78.990, up 0.471% as on 06 December 2019.

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...