Whitehaven Coal Limited

Decent Rise in Coal Production in September’19 Quarter:Whitehaven Coal Limited (ASX: WHC) is engaged in the business of development and operation of coal mines in New South Wales. Recently, UBS Group AG and its related bodies ceased to be a substantial holder in the company, effective from November 14, 2019. On November 13, 2019, Prudential plc and its subsidiary companies, became a substantial holder in the company with a stake of 5.10%. As per another update, George Raymond Zage III acquired 200,000 direct shares and 9,000,000 indirect shares at a value of $29,484,427.

September’19 Quarter Key highlights:The managed saleable coal production rose by 23% on pcp, to 4,909k tonnes, and the company’s managed total coal sales stood at 5,546k tonnes during the quarter, up by 14% against the previous corresponding quarter. Total equity coal sales for the quarter stood at 4.5 million tonnes, with equity own coal sales of 3.9 Mn tonnes, which remained in line with the previous quarter.

The Maules Creek (75% interest) open cut mine ROM coal production declined by 14% to stand at 1,962k tonnes during the quarter; however, the saleable coal production increased by 3% to 2,034k tonnes. Coal stock at the end of the period declined by 7% to stand at 441k tonnes. Narrabri Underground Longwall mine (70% interest) ROM coal production increased by 226% to stand at 1,793k tonnes during the quarter, and saleable coal production increased by 147% to stand at 1,800k tonnes. Coal stock at the end of the period increased by 268% to stand at 949k tonnes.

.png)

September’19 Quarter Key Metrics (Source: Company Reports)

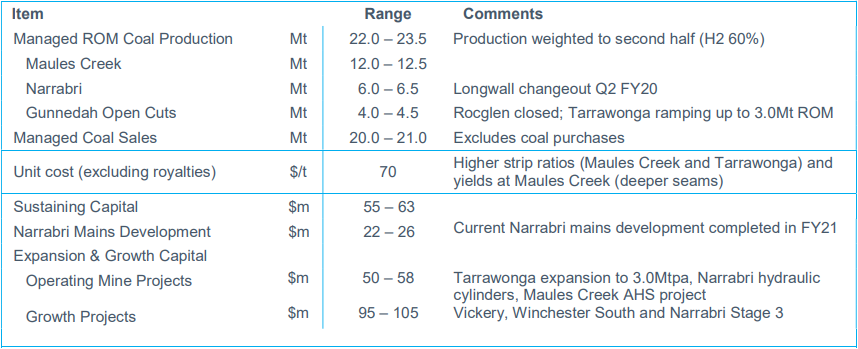

FY20 Guidance:FY20 managed ROM coal production guidance remains in the range of 22.0 to 23.5 million tonnes with managed coal sales of 20.0 to 21.0 million tonnes. The unit cost guidance (excluding royalties) stands at $70 per tonne.

FY20 Guidance (Source: Company Reports)

Stock Recommendation:WHC’s share generated a negative YTD return of 22.28%. Its gross margin, EBITDA margin and net margin for FY19 stood at 54.6%, 59.1% and 21.2%, better than the industry median of 44.3%, 32.2% and 15.3%, respectively, implying decent fundamentals of the company. ROE for FY19 stood at 15.1%, better than the industry median of 13.2%. Debt to equity ratio for FY19 stood at 0.12x, lower than the industry median of 0.24x. Moreover, its Price to Book Value multiple on TTM basis stands at 0.9x, lower than the industry median of 1.6x, indicating the undervalued position at the current juncture. Hence, considering the company’s September Quarter production data, FY20 production guidance and current trading levels, we recommend a “Buy” rating on the stock at the current market price of $3.020, down 2.894% on November 20, 2019.

New Hope Corporation Limited

Unaudited Q1FY20 Revenue Improved by 14% on PCP:New Hope Corporation Limited (ASX: NHC) is involved in the exploration, development, production and processing of coal, oil & gas. On November 19, 2019, the company highlighted its FY19 record profit before non-regular items that witnessed a3% rise over the previous year. Profit Before Tax and non-regular items for the full year period was reported at $384 Mn.Net Profit After Tax before non-regular items was reported at $268 Mn, whilst Net Profit After Tax after non-regular items was reported at $211 Mn. Full-year dividend totalled 17 cents per share, representing an increase of 21% on the previous year.

On November 1, 2019, the company welcomed the decision from the Queensland Court of Appeal, dismissing Oakey Coal Action Alliance’s appeal and granting orders requested by New Acland Coal Pty Ltd. The Court stated the Land Court orders from President Kingham were valid and binding and the Environmental Authority stands. There is no further barrier to the Queensland Government and has now given final approvals for the New Acland Coal Mine Stage 3 Project.

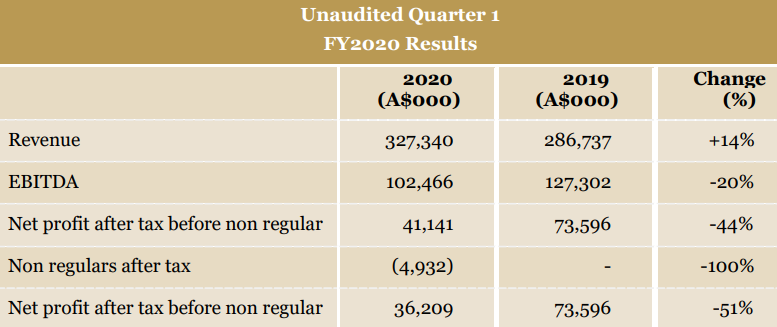

Key Highlights of October’19 Quarter:Unaudited revenue for the quarter increased by 14% to $327,340,000. Net profit after tax before non-regular items for the quarter decreased by 51% to $36,209,000, mainly due to a drop in the thermal coal price of 40% over the past year. During the quarter, total saleable coal production was 66% higher and total coal sales 62% higher than the prior corresponding period, mainly due to the increased ownership in the Bengalla mine.

Q1FY20 Key Financial Metrics (Source: Company Reports)

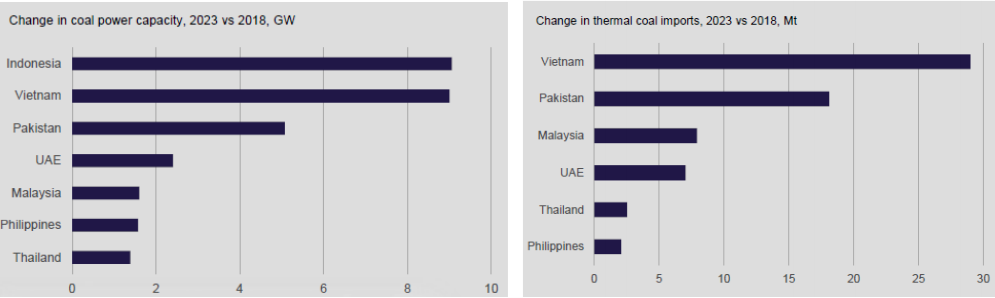

Outlook:Traditionally, Japan has demanded the highest quality coal in the world due to ash disposal costs. Taiwan is now seeking lower ash, higher energy coals for environmental reasons. Korea is seeking lower sulphur and considering tighter controls on ash. The scenario is positive for Australian coals in general. The company believes in a positive outlook for coals of Surat Basin quality which have low ash and sulphur, comparatively high energy and low emissions.

Growth Forecast in South East Asia (Source: Company Reports)

Stock Recommendation:NHC’s share generated a negative YTD return of 33.43%. The company’s profitability margins, including gross margin, EBITDA margin and net margin for FY19 stood at 45.2%, 39.6% and 16.1%, better than the industry median of 44.3%, 32.2% and 15.3%, respectively. It posted positive revenue growth for the October quarter. However, due to decrease in coal prices, net income reduced by around 51% as compared to pcp. Given the effective coal operations with growing production and safety levels along with the projects in pipeline, the company seems well-positioned to meet the growing energy demands of its Asian customers.Its Price to Book Value multiple on TTM basis stands at 0.9x, lower than the industry median of 1.6x, indicating the undervalued position at the current juncture. Hence, considering above factors and current trading level, we recommend a “Buy” rating on the stock at the current market price of $2.140, down 2.283% on November 20, 2019.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...