Sezzle Inc.

.png)

SZL Details

Healthy Capital Position: Sezzle Inc. (ASX: SZL) provides a technology-driven payment platform that facilitates fast payments between end-customers and retailers through its interest-free installment plans, delivering both budgeting and financing value proposition. As on 2 July 2020, the market capitalization of the company stood at ~$761.41 million. During Q1FY20 ended 31st March 2020, the company’s (Underlying Merchant Sales) UMS surged 321% on a YoY basis to a record US$119.4 million, and active customers rose by ~326%. In the same time span, repeat usage improved by 190bps on QoQ basis to 85.6% and active merchants jumped by 27%. During the quarter, the company retained a healthy capital position with a funding facility of US$100 million and a cash balance of US$36.6 million. In the same time span, operating cash outflows stood at ~US$1.8 million, as compared to the cash outflows of US$6.4 million in 4Q19.

.png)

Growth in Monthly UMS (Source: Company Reports)

Leading Loss Indicators Trending Favorably: The company tracked the indicators and reported better collection rates on YoY and MoM basis. The rescheduled payments are improving, and dispute rates are declining. It has a broad range of monetary and fiscal stimulus to combat the disruption caused by COVID-19 and exhibited growth with high user experience.

What to Expect: The growth momentum from the first quarter continued into April and SZL saw an increased online retail spending. The shift to online shopping has positioned Sezzle as a key partner for merchants. SZL is leveraging its network and has a large market opportunity with the US retail market of over US$5.4 trillion. It is building momentum in all key verticals.

Key Risks: While conducting its business operations, SZL is exposed to a variety of risks. The company depends on continued relationships with its current significant retail merchant clients with no guarantee that these relationships will continue. The contracts can be terminated for convenience and can impact the company’s operations. Also, the profitability of the company is dependent on its ability to put in place and optimize its systems and processes to make predominantly accurate decisions. The end-customer bad debts can adversely impact the company’s profitability.

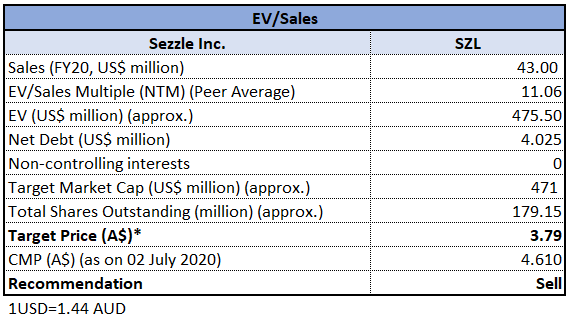

Valuation Methodology: EV/Sales Multiple Based Relative Valuation (Illustrative)

EV/Sales Multiple Based Relative Valuation (Source: Refinitiv, Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: The company has quickly responded to the global pandemic. However, the company has been experiencing an increase in ticket volumes due to the supply chain impacts. As per ASX, the stock of SZL gave a return of 91.44% in the past one month and has limited potential, going forward. The stock is trading close to its 52-week high of $4.450. We have valued the stock using an EV/Sales multiple based illustrative relative valuation method which suggest a correction of lower double-digit (in percentage terms). For the said purpose, we have considered Zip Co Ltd (ASX: Z1P), FlexiGroup Ltd (ASX: FXL), etc. as peers. Considering the aforesaid facts, current trading levels, and attractive returns in the past one month, we suggest investors to book profit and recommend a ‘Sell’ rating on the stock at the current market price of $4.16, down by 2.118% on 2 July 2020.

SZL Daily Technical Chart (Source: Refinitiv, Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

AU

AU

Please wait processing your request...

Please wait processing your request...