Stocks’ Details

REA Group Limited (ASX: REA)

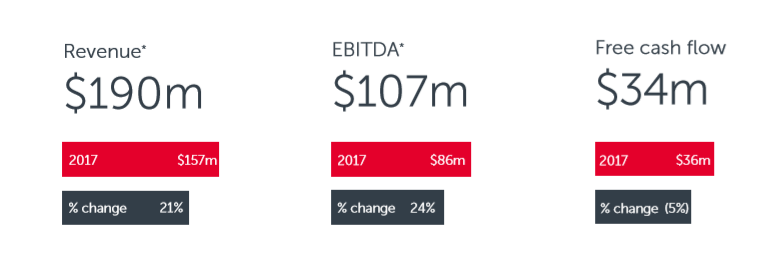

Strength from 2017 to continue in 2018: 2017 was a strong year from the financial point of view for digital advertising company, REA. During FY17, revenue from its core operations increased by 16% and it reached to $671 million and also its group EBITDA rose by 16% and accounted to $381 million. It also achieved a 12% increase in net profit by finishing FY17 at $228 million and earnings per share increased by 12% and reached to 173.3 cents. The group expects the momentum to continue in FY18 while it remains focussed on creating value and on delivering returns to its shareholders. The revenue after broker commission for Q1 FY 2018 was AUD $190 and whereas it was just AUD $157 for Q1 FY17. The excellent revenue growth was driven by the Australian residential business and by the inclusion of financial services which was not included in the prior comparative period. It is expected that the market conditions in developer and in media will continue to grow in the remaining part of the year. Moreover, its return on capital employed has increased by almost 1,600% over the past 12 months. The stock prices increased by 13.5% in the past six months. Looking at the overall scenario, the stock has more potential to grow, and we recommend to “Hold” the stock at the current price of $73.99

Q1 FY18 Results (Source: Company Reports)

Carsales.com Limited (ASX: CAR)

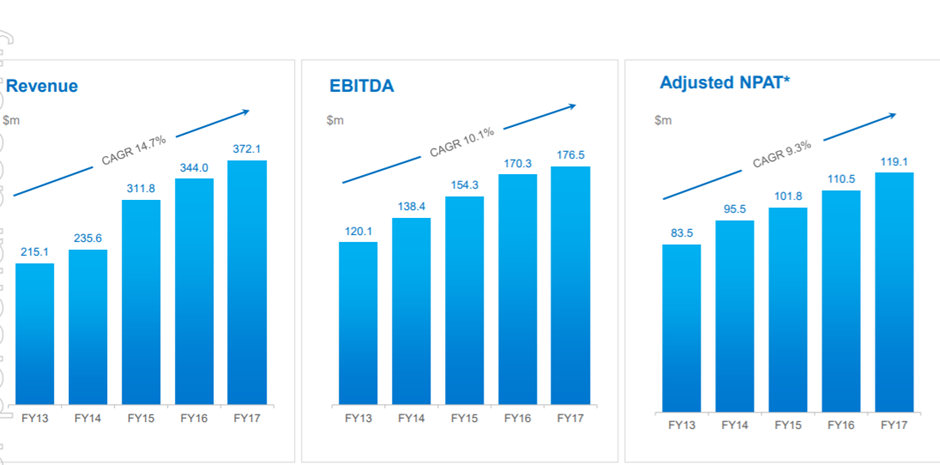

Mixed Performance: Recently, Carsales announced that it acquired the remaining 50.1% interest in South Korea’s SK ENCARSALES.COM and by this Carsales got 100% of control and ownership of South Korea’s number one online auto classifieds business. On the other hand, Vinva Investment Management had become the substantial holder of CAR by holding 12,450,606 shares with 5.13% of voting power. CAR had reported a revenue growth of 8% and EBIDTA growth of 4% for FY17. It declared a final dividend of 21.5 cents per share which was up by 10% on prior corresponding period. Costs were also in control and operating leverage was achieved. As far as its performance in International market is concerned, there was a strong growth in SK Encar because of which the underlying revenue and EBIDTA was up by 29% and 32%, respectively as compared to prior year. Moreover, the group’s first quarter FY18 results have been tracking well and the return on equity has been better than average industry level. It’s Finance and Related Service business continued to show signs of stabilisation which are anticipated to be continued throughout the remainder of FY18. Integration of IP and technology in Chilean, Mexican, Argentinian businesses are anticipated to help in earnings uplift. The group performance in Latin America, however, shows an impact on EBITDA Margins owing to investments in personnel costs. Competition in the market with better offerings is also a threat; and as far as the share price is concerned, it is already on a higher side and the stock looks “Expensive” at the current price of $14.55

x

Financial Performance Trend (Source: Company Reports)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...