Western Midstream Partners, LP

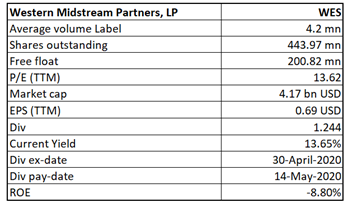

WES Details

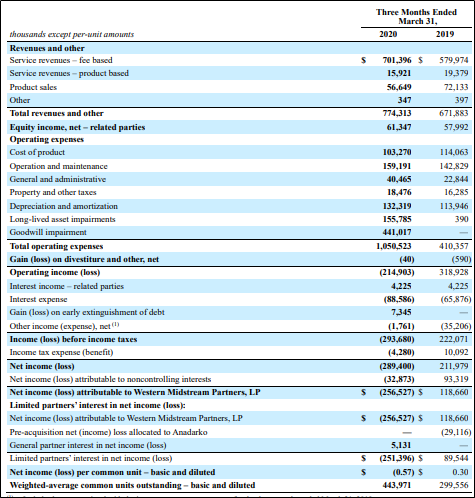

1QFY20 Financial Highlights for the Period Ended 31 March 2020: Western Midstream Partners, LP (NYSE: WES) formerly known as Western Equity Partners, LP was established to own, operate, acquire, and develop midstream energy assets. WES recently declared its 1QFY20 results, wherein the company reported total revenue and other income of $774.3 million, up from $671.9 million reported in the year-ago period. In 1QFY20, the company’s adjusted EBITDA stood at $513.6 million, up from $428.3 million reported in the year-ago period. Adjusted gross margin during the quarter came in at $701.3 million, up from $587.7 million reported in 1QFY19. Loss per share during the quarter stood at 57 cents as compared to earnings of 30 cents per share reported in the year-ago period. Net loss for the period incorporated non-cash impairments of goodwill and long-lived assets of $596.8 million.

Key Financial Highlights (Source: Company Reports)

Cost Reduction Initiatives: The company declared a quarterly cash distribution of $0.311 per unit for 1QFY20, which depicts a decline of 50% from the prior quarter’s per-unit distribution, payable on 14 May 2020. The lower cash distribution during the period was on the back of WES’s initiatives to protect and fortify its balance sheet during the COVID-19 pandemic, along with reducing economic activity and energy demand, along with reduced commodity prices.

Balance Sheet & Cash Flow Details: The company exited the period with cash and cash equivalents of $152.3 million and total assets amounting to $11.9 billion. The company has a long-term debt of $8.1 billion as of 31st March 2020. Cash from operating activities came in at $393.3 million in 1QFY20, with free cash flow amounting to $214.6 million.

FY2020 Outlook Update: WES remains well equipped to take necessary steps to protect the health and safety of the customers, employees, and their families. Adjusted EBITDA for FY20 is expected to be in the range of $1.725 billion and $1.825 billion, which incorporates previously stated cost reductions of ~$75 million pertaining to operating and maintenance and general and administrative expense. The company except its capital expenditure to be in the range of $450-$550 million, suggesting a decline of 45% from prior guidance.

Risk Analysis: The company is exposed to increased credit risk to the extent any of its customers, including Occidental, financial institutions, customers, and other parties. Further, due to global uncertainties and resulting precipitous decline in commodity prices have formed noteworthy near-to-medium-term uncertainty.

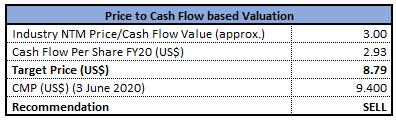

Valuation Methodology: Price/Cash Flow Multiple Based Relative Valuation (Illustrative)

Price to Cashflow Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation: The stock of the company gave positive returns of 17.06% in the last one month. The stock has a market capitalization of $4.17 billion and made a 52-week low and high of $2.90 and $31.99. At the closing price of $9.4, current yield for the stock stands at 13.65%. The stock has corrected ~29.22% and 68.08% in the last three months and one year, respectively. We have valued the stock using the Price to Cashflow multiple based illustrative relative valuation method and arrived at a price correction of single-digit (in percentage terms). Considering the price movements and valuations, we suggest investors to book profit at current levels and recommend a “Sell” rating on the stock at the closing price of $9.40, up 3.18% on 3rd June 2020.

WES Daily Technical Chart (Source: Refinitiv, Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

AU

AU

Please wait processing your request...

Please wait processing your request...