.png)

Stocks’ Details

Santos Limited

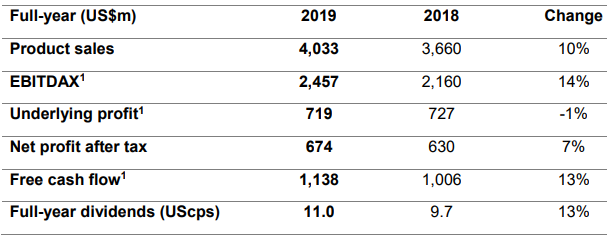

Robust Balance Sheet: Santos Limited (ASX: STO) is primarily involved in the exploration of gas and petroleum. The market capitalisation of the company stood at $7.1 Bn as on 30th March 2020. STO, recently announced that S&P Global Ratings (S&P) has reaffirmed Santos BBB- credit rating with a stable outlook, which is the result of disciplined low-cost operating model it implemented over the past four years. For the first two months of 2020, the company’s free cash flow stood at $186 million. The company possesses strong balance sheet with the cash in hand of $1.2 billion at the end of February 2020 and net debt amounting to $3.1 billion.

With respect to response to COVID-19, the company is committed for supporting the government and community efforts for restricting the spread of the virus.

FY19 Financial Overview (Source: Company Reports)

Focus on Lowering Cost: With respect to Cooper Basin, the company continues to focus on lowering unit development costs to unlock resources for generating future production growth.

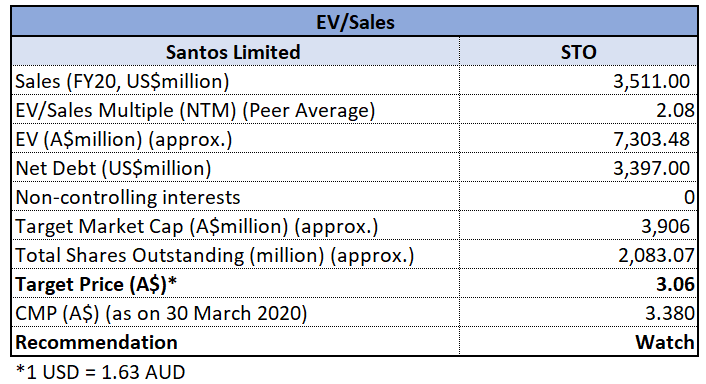

Valuation Methodology: EV/Sales Multiple Based Relative Valuation

EV/Sales Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures have been taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: The company has liquidity of $3.1 billion, which comprises of $1.2 billion in cash and $1.9 billion in committed undrawn debt facilities with maturities of two to five years. We have valued the stock using EV to Sales based relative valuation approach, and for the purpose, we have taken peers such as Woodside Petroleum Ltd (ASX: WPL), Beach Energy Ltd (ASX: BPT), Senex Energy Ltd (ASX: SXY), etc., and arrived at a target price, which is offering corrections of lower double-digit in percentage terms. Hence, considering the decent performance in the initial months of 2020, spreading COVID-19 and valuation, we have a watch stance on the stock at the current market price of $3.380 per share, down by 0.88% on 30th March 2020.

Senex Energy Limited

Strong Financial Position: Senex Energy Limited (ASX: SXY) is in the production, development and exploration of petroleum with a market capitalisation of $240.4 Mn as on 30th March 2020. In the recent response to Covid-19, the company assured that it is implementing important business continuity measures for SXY. The company possesses a robust financial position along with resilient cashflows from its low-cost oil and gas operation. Senex reported strong liquidity with cash reserves of $105 million and drawn debt of $125 million as at 29th February 2020. Moreover, it is anticipating completing its transformational Surat Basin work program in the upcoming months.

.png)

Sales Revenue (Source: Company Reports)

Guidance for FY20: For FY20, the company is expecting production of 1.8-2.0 mmboe and EBITDA in the range of $40 million-$50 million. The company is well-positioned to continue to deliver material operating cashflow in a lower oil price environment.

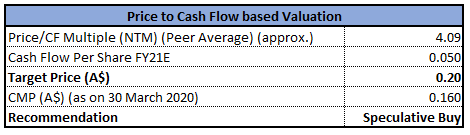

Valuation Methodology: P/CF Multiple Based Relative Valuation

P/CF Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures have been taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: Oil and gas portfolio of the company generates revenue from fixed price domestic gas contracts, oil-linked gas contracts as well as oil production with material downside hedging. We have valued the stock using P/CF-based relative valuation approach, and for the purpose, we have taken peers such as Cooper Energy Ltd (ASX: COE), Santos Ltd (ASX: STO) and Woodside Petroleum Ltd (ASX: WPL) and arrived at a target price, which is offering an upside of lower double-digit (in percentage terms). Thus, considering the strong liquidity position and guidance for FY20, we give a “Speculative Buy” recommendation on the stock at the current market price of $0.160 per share, down by 3.03% on 30th March 2020.

Cooper Energy Limited

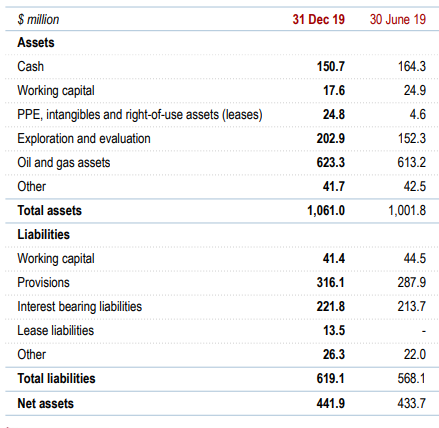

Increased Cash Generation: Cooper Energy Limited (ASX: COE) is involved in oil and gas exploration and production. The market capitalisation of the company stood at $658.79 Mn as on 30th March 2020. The company recently announced that Greencape Capital Pty Ltd has made a change to substantial holdings on 11th March 2020 and the current voting power remains at 7.06% as compared to the previous voting power of 6.02%. During 1H FY20, the company reported Underlying EBITDAX amounting to $16.3 million, up 11% on pcp. It reported increased cash generation with cash from operating activities of $31.4 million as compared to the cash outflow of $0.9 million of 1H FY19.

Balance Sheet (Source: Company Reports)

Expected Rise in Production at Sole: The company is expecting a transformational rise in its production and cash flow from Sole gas project. For FY20, it anticipates capital expenditure of $86 million – $93 million.

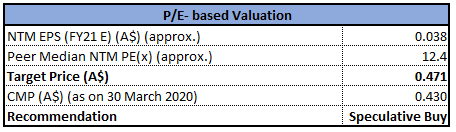

Valuation Methodology: P/E Multiple Based Relative Valuation

P/E Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures have been taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: Net margin of the company stood at 15.2% in 1H FY20 as compared to the industry median of 8.0%. This reflects that Cooper has decent capabilities to convert its topline into the bottom line against the broader industry. We have valued the stock using P/E based relative valuation approach, and for the purpose, we have taken peers such as Senex Energy Ltd (ASX: SXY), Origin Energy Ltd (ASX: ORG), Woodside Petroleum Ltd (ASX: WPL), etc., and arrived at a target price, which is offering an upside of high single digit (in percentage terms). Thus, considering the decent capabilities to convert its topline into the bottom line, increased cash generation and decent outlook, we give a “Speculative Buy” recommendation on the stock at the current market price of $0.430 per share, up by 6.173% on 30th March 2020.

Carnarvon Petroleum Limited

Challenging Business Conditions: Carnarvon Petroleum Limited (ASX: CVN) is in the exploration and production of oil and gas. The market capitalisation of the company stood at $226.84 Mn as on 30th March 2020. The company is currently experiencing challenging business conditions due to COVID-19 virus and lower oil price environment. With respect to the Dorado project, the company stated that the development work is continuing as per plan with engineering and pre-FEED work streams being advanced, broadly to plan timing wise. As at 31st December 2019, the company possessed a strong cash balance of A$119 million with nil debt. This was mainly due to lower than planned Dorado drilling costs in 2019. CVN is well positioned to progress and support the operator of Dorado development.

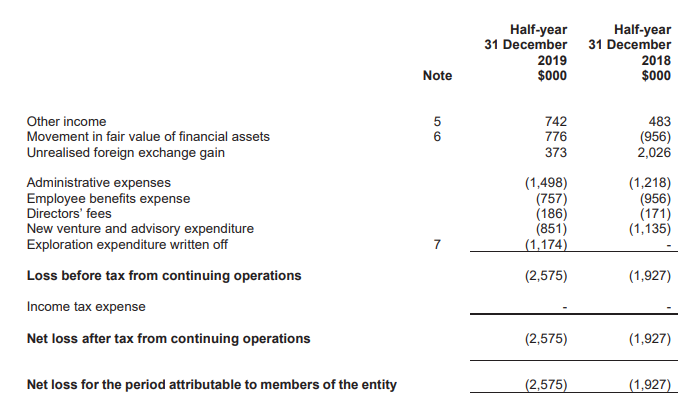

Consolidated Income Statement 1H FY20 (Source: Company Reports)

Future Aspects: During Q2 FY20, the company has maintained a strong and prudent financial position, resultantly, CVN is now able to cover all its planned 2020 expenditure.

Stock Recommendation: Asset to equity of the company stood at 1.01x in 1H FY20 against the industry median of 2.13x. The Business has grown to around $530 million in value during the last five years which has delivered a compound annual growth rate of around 18% per annum. As per ASX, the stock of CVN is trading closer to its 52-weeks lower levels, which could be undertaken as decent levels to entry. Therefore, strong cash flow position, nil debt and growth in business, we give a “Speculative Buy” recommendation on the stock at the current market price of $0.140 per share, down by 3.448% on 30th March 2020.

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

AU

AU

Please wait processing your request...

Please wait processing your request...