Village Roadshow Ltd

.png)

VRL Dividend Details

Acquired Opia to enhance its UK digital business: Village Roadshow Ltd (ASX: VRL) is focusing to expand its digital business apart from its core theme parks, cinema exhibition, film production and distribution business. As a result, the group’s UK subsidiary, Edge Loyalty Systems recently reported that they are acquiring 80% of the Opia business to expand their presence in UK digital business for GBP 24 million. Management estimates this acquisition to be earnings accretive from acquisition date as well as generate a positive cash-flow. Opia’s EBITDA is forecasted to be over GBP 6 million per annum during first full year of acquisition while net profit after tax contribution for the first full year is forecasted to be over GBP2.6 million (A$5.8 million), wherein VRL will have 80% share.

.png)

Edge performance in 2015 (Source: Company Reports)

VRL’s edge is also seeking to further penetrate in its current as well as new Asian markets to further strengthen the group’s digital business.

Meanwhile, VRL stock has been bullish over the past few months and delivered a rise of 7.05% in the last six months and 3.82% in the last four weeks (as of January 15, 2016). We believe VRL’s positive momentum in the stock to continue and accordingly put a “BUY” recommendation on this dividend yield stock at the current price of $6.54

VRL Daily Chart (Source: Thomson Reuters)

Wam Capital Ltd

.png)

WAM Dividend Details

Surpassed Index performance: WAM Capital Ltd (ASX: WAM) fund reported a 25.6% rise during 2015 year and generated an 18.3% returns from its inception to the year ended on December 2015. Moreover, WAM Capital had beaten the index by 21.8% during the 2015 year, and had an average cash holdings of 34.0%. This performance by WAM indicates the strong expertise of its team while the higher cash holdings shows that the team is not taking decisions in haste and could even hold cash if required. As a result the shares of WAM delivered a strong rally by 7.69% in the last six months (as of January 15, 2016).

.png)

WAM performance against the Index (Source: Company Reports)

WAM is also trading at a decent valuations with a reasonable P/E and has a strong dividend yield. We believe that the positive momentum in the stock would continue in the coming months and based on the foregoing we recommend a “BUY” on the stock at the current price of $2.10

WAM Daily Chart (Source: Thomson Reuters)

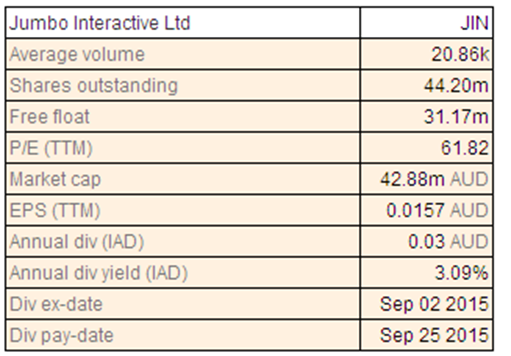

Jumbo Interactive Ltd

JIN Dividend Details

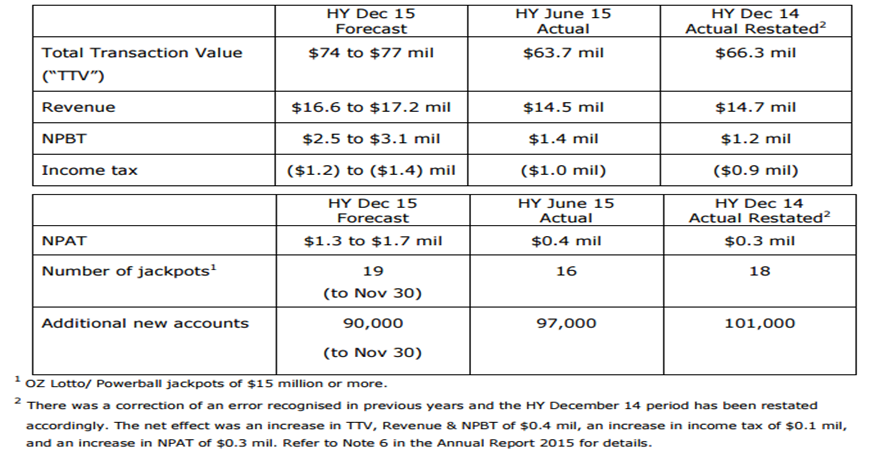

Focusing to control expenses while maintaining aggressive marketing efforts in Australia: Jumbo Interactive Ltd (ASX: JIN) management reported that the group is on track to deliver a sales increase in the range of 12% - 16% to $74 to $77 million during the half year ended on December 2015, driven by better customer account and strong run of jackpots. JIN is also focusing to enhance its costs management via Germany restructuring efforts and hence estimates a net profit after tax in the range $1.3 to $1.7 million. Meanwhile, Jumbo Interactive continues to focus on its online marketing in Australia and consequently the Mobile activity reached 50% while the number of Facebook likes reached 95,000 as at June 30, 2015. JIN reported a TTV increase of over 19% during the half year ended on December against the previous half year ended on June 2015. Customer account database rose by over 90,000 accounts in 5 months ended on November, 2015.

Half Year ended on December 2015 performance (Source: Company Reports)

Jumbo Interactive is also maintaining a strong balance sheet having Net Assets of $24.0 million as at 30 November 2015 while cash reached $24.7 million with $17.8 million of net cash plus $6.9 million of players’ funds. On the other hand, JIN stock fell over 6.73% in the last three months (as at January 15, 2016) as the management warned for a cautious trading performance for the second half year ending June 2016 depending on the jackpot levels.

But, we view this as short term correction as the group’s Germany restructuring benefits would contribute to JIN’s overall bottom line performance. We give a “BUY” on this dividend yield stock at the current price of $0.965

.png)

JIN Daily Chart (Source: Thomson Reuters)

Retail Food Group Ltd

.png)

RFG Dividend Details

Entered FY16 on a positive note: Retail Food Group Ltd.’s (ASX: RFG) management reported that their FY16 year to date performance (as of Nov 26 report) had been positively driven by its core as well as international performance. Management reported that the new domestic outlet growth during FY16 year-to-date (YTD) already comprised over 70% of its total FY15 organic outlet commissioning while International outlet growth accounted over 50% of 1H16 commissioning driven by increasing Malaysian, Turkish and Chinese penetration. The group is on track to reach its new outlet organic growth of 250 during FY16. QSR Division Average Transaction Value improved by 5.5% during FY16 YTD driven by the group’s stress on service, quality products and retail pricing structure. RFG expects a better second half of 2016 performance for its Commercial operations which comprise coffee and allied beverage pursuits. The group forecasts a 25% rise of underlying NPAT during first half of 2016 while underlying NPAT is forecast to deliver a 35% increase on 1H16 as compared to the prior corresponding period.

.png)

FY 16 YTD highlights (Source: Company Reports)

RFG reiterated its FY16 forecasts of an increase by 20% of underlying NPAT as compared to fiscal year of 2015. On the other hand, RFG shares plunged over 20.97% in the last six months (as of January 15, 2016) impacted by the weak consumer sentiment.

However, with the group’s positive FY16 opening, we believe the stock has the potential to rally further in the coming months. We maintain our “BUY” recommendation on this dividend yield stock at the current price of $4.19

.png)

RFG Daily Chart (Source: Thomson Reuters)

Clean Seas Tuna Ltd

.png)

CSS Details

Ongoing sales volume growth: Clean Seas Tuna Ltd (ASX: CSS) expects a solid sales volume growth to over 2,000 tonnes for FY16, driven by its ongoing Australian and European markets performance as compared to a sales volume of 1,098 tonnes in FY15. The group’s Sales as of November 2015 surged over 45% year on year to 594 tonnes. Meanwhile, CSS is also launching new fresh and frozen products for its food service and retail markets business to leverage its strong production performance. On the other hand, management forecasts a pre-tax loss of $7 million during first half of 2016 against a loss of $0.7 million in H1FY15, due to Strategic Sales & Marketing initiatives which would incur over $4 million of further costs. As a result, the shares of CSS fell over 20.34% in the last six months (as of January 15, 2016). On the other side, the group expects a better second half of 2016 driven by the seasonality of the group’s earnings, as most of annual fish growth is generated in second half on the back of higher average seawater temperatures. Moreover, the group reported that David Head would be its Managing Director and Chief Executive Officer who comes with more than 25 years’ experience in several roles, bringing more clarity over its management. CSS is trading at a decent valuation against its peers. We put a “BUY” recommendation on the stock at the current price of $0.046

CSS Daily Chart (Source: Thomson Reuters)

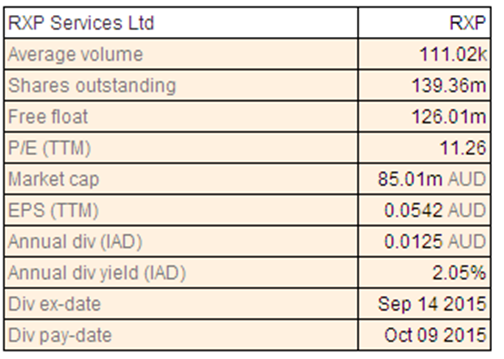

RXP Services Ltd

RXP Dividend Details

Delivering performance in line with estimates: RXP Services Ltd (ASX: RXP) management reported for strong performance and the company is on track to reach a revenue of more than $108 million revenue while PBT is forecasted to be in the range of 13% to 14% during fiscal year of 2016. The group intends to integrate EV as well as 10collective going forward, while its investments would continue in the RXP Solutions and As a Service offerings.

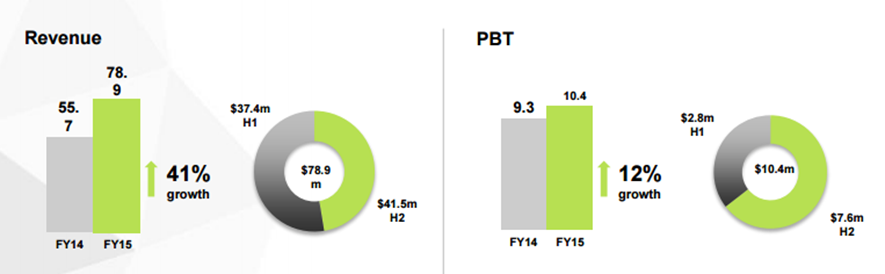

FY15 performance (Source: Company Reports)

RXP delivered an outstanding FY15 revenue increase of 41.5% to $78.9 million while its second half witnessed even better performance generating 26% increase in revenue as well as the profit.

As a result, RXP stock surged over 48.78% in the last six months (as of January 15, 2016), and still trading at reasonable valuations with a cheaper P/E. We maintain our “BUY” recommendation on this dividend yield stock at the current price of $0.59

.png)

RXP Daily Chart (Source: Thomson Reuters)

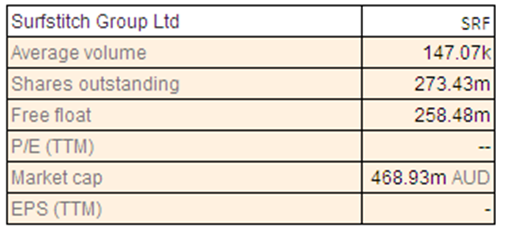

Surfstitch Group Ltd

SRF Details

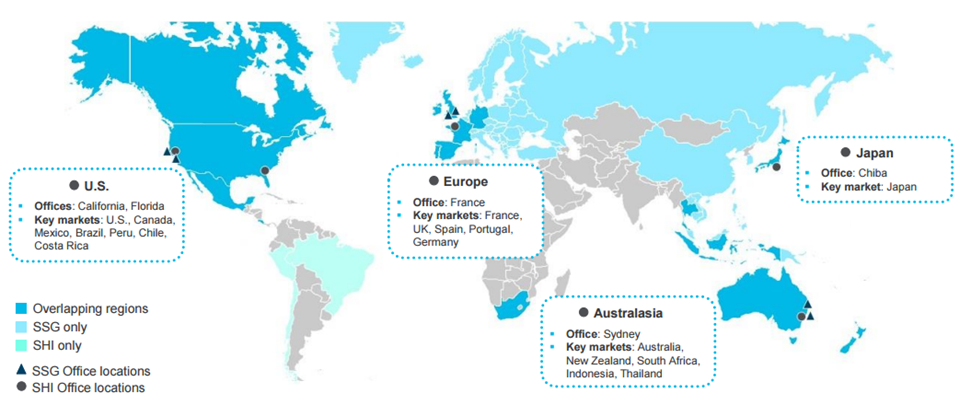

Strengthening e-commerce capabilities via SHI acquisition: Surfstitch Group Ltd (ASX: SRF) finished the acquisition of SHI Holdings for $23.7 million to leverage SHI’s e?commerce capabilities as well as its high performance water board sports products and accessories. SRF is also targeting to boost its South America and Asia penetration via SHI’s strong presence across these markets. Meanwhile, SRF reiterated its full year pro forma FY16E EBITDA guidance in the range of $18 million to $22 million which would even comprise SHI contribution on a full year pro forma basis. The group is also enhancing its capital position by raising over $50 million institutional placement via the issue of 25 million ordinary shares at $2.00 per share accounting to a 2.9% discount to the closing price of A$2.06 (based on November 26 report) and a 0.2% premium to the 5-day VWAP of $1.996.

Overlapping presence of SHI and Surfstitch (Source: Company Reports)

With the stock delivering a raise of 2.39% in the last three months (as at January 15, 2016), we believe the positive momentum would be seen in the coming months and based on the foregoing, we give a “BUY” on the stock at the current price of $1.67

SRF Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2016 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

AU

AU

Please wait processing your request...

Please wait processing your request...