G8 Education Ltd

.png)

GEM Details

Acquisition driven growth: G8 Education Ltd (ASX: GEM) confirmed that Series 001 Notes have been redeemed and replaced by Series 003 Notes. The company also reported that its net debt to EBITDA is now expected to be about 2.1x as at 31 December 2016. GEM had earlier stated about its intention to continue to grow by pursuing acquisitions in the range of $50m and $150m while maintaining the net debt to EBITDA at or under 2x. Moreover, G8 is building and operating a portfolio of outstanding early childhood education brands (currently 24 brands) in Australia & Singapore.

.png)

Group Centre Portfolio (Source: Company Reports)

GEM has 35,221 licenses and had increased the direct capital investment to the centers by 40% in 2015. Meanwhile, the group also declared a distribution amount of $0.06 and has a solid dividend yield. GEM stock has risen 15.6% in the last six months (as of July 20, 2016), and we maintain a “Buy” recommendation on the stock at the current price of $3.99

.PNG)

GEM Daily Chart (Source: Thomson Reuters)

Nine Entertainment Co Holdings Ltd

.png)

NEC Details

Agreement with Southern Cross Austereo: Nine Entertainment Co Holdings Ltd (ASX: NEC) corrected over 40.4% during this year to date (as of July 20, 2016) on the back of declining FTA market. On the other hand, the group had signed a new regional television affiliation agreement with Southern Cross Austereo (SCA) for which SCA would pay Nine an affiliation fee of 50% of its television revenue. This is a five-year agreement in which SCA is broadcasting Nine’s metropolitan free-to-air television content into regional Queensland, Southern NSW and regional Victoria from 1

st July 2016.

As part of the deal, Nine and SCA would work together on a number of opportunities to mutually grow their businesses. Meanwhile, NEC undertook a $150 million buy-back program. NEC will release its final FY16 results in August 2016. The stock has an outstanding dividend yield. Based on the foregoing, we give a “Hold” recommendation on the stock at the current price of $1.125

NEC Daily Chart (Source: Thomson Reuters)

FlexiGroup Limited

.png)

FXL Details

Investment in Kikka: FlexiGroup Limited (ASX: FXL) expects 8% growth of Cash NPAT in FY 16 to $97 million and expects greater than 10% growth by FY 18. FXL is focusing on the core business units of consumer and business finance. For this it has made equity investment and a funding line into Kikka to enter new markets at speed compared to competitors. Moreover, FXL has acquired Fisher & Paykel Finance from Fisher & Paykel Appliances. This would increase its FY16 Cash NPAT guidance with FY16 dividend expected within 50-60% of Cash NPAT.

However, as per FXL’s securitization under the Flexi ABS program, the company has announced the pricing of AUD260m asset-backed securities, supported by a pool of Australian unsecured, retail, “no interest ever” payment plans, originated by Certegy Ezi-Pay Pty Ltd (“Certegy”), a wholly owned subsidiary of FlexiGroup Limited. FXL recovered over 6.43% in the last one month (as of July 20, 2016) and the stock has a good dividend yield. We maintain our “Speculative Buy” recommendation on the stock at the current price of $2.05

FXL Daily Chart (Source: Thomson Reuters)

National Australia Bank Ltd

.png)

NAB Details

Enhancing balance sheet metrics: National Australia Bank Ltd (ASX: NAB) has advised that its third quarter trading update will be released in August 2016. Meanwhile, the bank has been enhancing its fundamental position and lowered its loan-to-valuation ratio (LVR) to 70% from the more usual 80%. With the recent Brexit outcome, the group reported that they would evaluate lending to foreign buyers on a case by case basis.

.png)

Strong Capital Position (Source: Company Reports)

On the other hand, NAB has merged five of its pension funds into one, to create Australia's largest retail superannuation fund, that has about A$70 billion under management. NAB has made an agreement with Japan's Nippon Life by selling 80% of its life insurance business which would be completed by second half of 2016.

NAB has redeemed US$600 million perpetual capital notes. We give a “Buy” recommendation on the stock at the current price of $26.24

NAB Daily Chart (Source: Thomson Reuters)

Australia and New Zealand Banking Group Ltd

.png)

ANZ Details

Expecting improved financial performance: Australia and New Zealand Banking Group Ltd (ASX: ANZ) recently reported that they would issue JPY 10 billion of fixed rate subordinated notes due 11

th July 2028 pursuant to its US$60 billion Euro Medium Term Note Program. On the other side, Standard & Poor’s reaffirmed ANZ’s ‘AA-’ long-term and ‘A-1+’ short term issuer credit ratings and stated that the standalone credit profile of ANZ remains unchanged.

ANZ would consolidate dividend payout ratio within the range of 60-65 percent of annual cash profit, from prior 65-70 percent and is expecting improved financial outcomes from institutional in future periods. ANZ is focusing on its consumer and small business franchises and is expanding at New South Wales in Australia, while focusing on long term growth in Asia despite short term Brexit impact. We give a “Buy” recommendation on the stock at the current price of $25.42

.PNG)

ANZ Daily Chart (Source: Thomson Reuters)

Seven West Media Ltd

.png)

SWM Details

Acquiring Perth Now and The Sunday Times: Seven West Media Ltd (ASX: SWM) lately announced about negotiations to acquire Perth Now and The Sunday Times from News Australia after getting regulatory approval including approval from the ACCC. As part of the agreement, Seven West Media and News Corporation would implement a news content sharing agreement for The West Australian with News’ daily brands in Adelaide, Brisbane, Melbourne and Sydney and they are also joint venture partners in the Community Newspaper Group in Western Australia.

.png)

FY16 Half Year Highlights (Source: Company Reports)

The acquisition would allow the company to explore expansion of its printing operations which could deliver improvements in scale benefits and print synergies.

Meanwhile, Newzulu Limited has successfully raised $5 million through a placement with the support of strategic investor Seven West Media and financial cornerstone Thorney Investment Group and its associates. A fully underwritten entitlement issue would be offered to all shareholders to raise an additional $2 million. We maintain a “Hold” recommendation on the stock at the current price of $1.145

SWM Daily Chart (Source: Thomson Reuters)

Cromwell Property Group

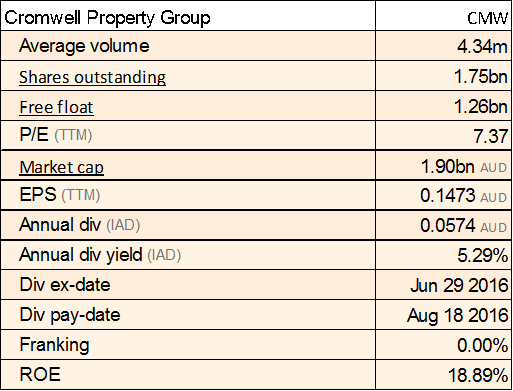

CMW Details

Acquired interest in Investa Office Fund: Cromwell Property Group (ASX: CMW) has successfully renegotiated the terms of its $861 million secured debt platform which has extended Cromwell’s weighted average debt expiry (WADE) from 3.22 years as at 31

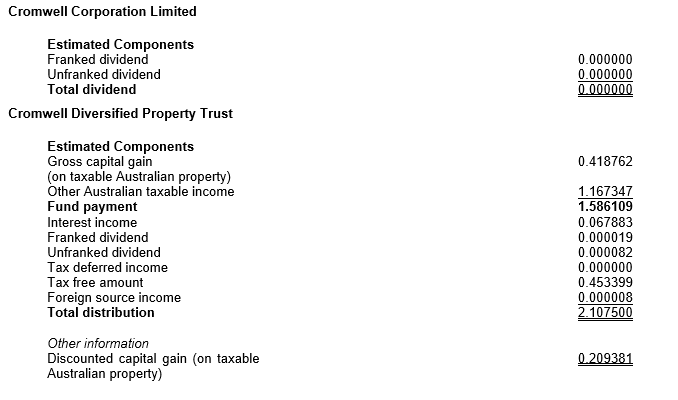

st December 2015 to 4.38 years. It would also reduce the weighted average margin across all facilities by about 5 basis points. Meanwhile, Cromwell Property Securities Limited as responsible entity for Cromwell Diversified Property Trust has acquired a relevant interest in 9.83% of Investa Office Fund units. The group issued FY16 operating earnings forecast at 9.0 cps while FY16 estimated distributions would increase 0.1 cps to 8.2 cps. CMW is paying dividend of AUD 0.02107500 in August 2016.

Distribution components for the quarter ended 31 March 2016 (Source: Company Reports)

On the other hand, we believe that CMW stock could face pressure in the coming months given the challenging global market conditions. The consumer confidence and housing performance in Australia are also having an impact. We give an “Expensive” recommendation on the stock at the current price of $1.105, and would review the stock at a later date.

CMW Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...