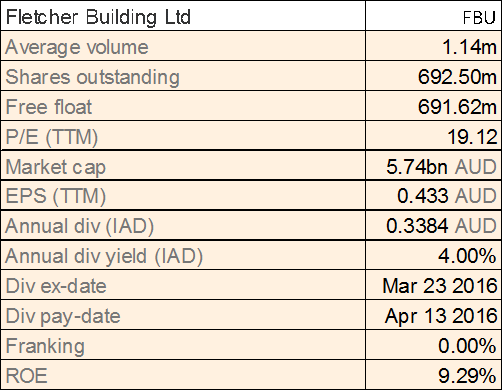

Fletcher Building Ltd

FBU Details

Change in ASX admission category: Fletcher Building Limited (Australia) (ASX: FBU) has changed its admission category on ASX to ASX Foreign Exempt Listing effective May 06, 2016 based on the dual-listed entity’s compliance requirements. The company set a target to generate revenue of $1.46bn and EBIT of 7% against the FY13 results. FBU has also been working to improve the supplier performance and reducing cost. Moreover, FBU has delivered a $4.9m of annualized cost during the first half 2016. FBU and NALCO were said to form the joint venture by June 2016. Moreover, FBU manufacturing site in Auckland would close and will be funding its share of the capital expenditure to expand NALCO’s Hamilton manufacturing facility.

Estimates (Source: Company reports)

Therefore, the new entity will have two key manufacturing sites with an extrusion and powder coating facility in Hamilton and a powder coating facility in Christchurch.

In addition, after full year operation of the joint venture, the revenue is expected to be about $190 million. As a result, FBU stock has risen 33.96% in the last six months (as of July 11, 2016), placing the stock at unreasonable level with the stock trading at a high P/E. Accordingly we give an “Expensive” recommendation on the stock at the current price of $8.58

FBU Daily Chart (Source: Thomson Reuters)

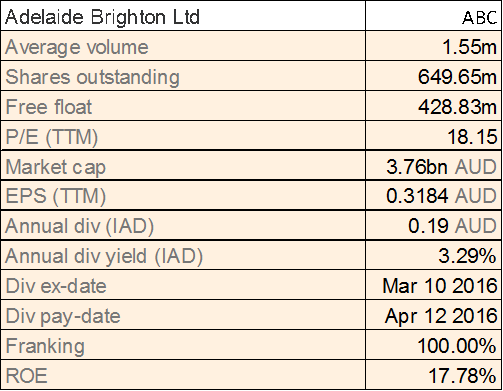

Adelaide Brighton Ltd

ABC Details

Threat from import costs: Adelaide Brighton Ltd (ASX: ABC) expects its 2016 sales volume of cement and clinker to be similar or slightly less than 2015 but the premixed concrete and aggregates sales volumes will be significantly higher than 2015 due to demand from east coast markets. Accordingly, the sales of concrete products are also expected to be better than 2015 and the lime sales volume is expected to be slightly higher as average realized prices are likely to increase. On the other hand, the threat of small scale lime imports in Western Australia and the Northern Territory is prevalent as the weaker Australian Dollar reduces the competitiveness of imports. Meanwhile, the price increased for all products due to strong demand, capacity utilization and a weaker Australian Dollar, which increases the cost of imports and has been implemented in 2016. But ABC has hedged the imports of cement, clinker and slag hedged through to December 2016 as in present scenario at current exchange rates it is estimated that import costs will increase by about $8 million in 2016.

The consensus expectations for FY17 and FY18 profits are said to be overly optimistic and there is a chance that cement volumes decline in FY17 while competition risks prevail within cement. Despite the efforts from the group, we believe that the stock would continue to remain under pressure in the coming months, and accordingly we give an “Expensive” recommendation on the stock at the current price of $5.80

ABC Daily Chart (Source: Thomson Reuters)

Boral Limited

.png)

BLD Details

Weak Demand: Boral Limited (ASX: BLD) expects its Boral Construction Materials & Cement segment to witness lower earnings in second half than 1H FY2016 due to continuing challenging conditions and fewer working days in the second half. Meanwhile, the demand of Boral Building Products would be affected by lower housing in WA & SA but the group reported that solid East coast housing market would offset this pressure.

However, BLD stock already has risen 18.83% in the last six months (as of July 12, 2016) and has already factored recent products’ price increase and increased housing activity. But we believe that the stock would be under pressure in the coming months given the ongoing challenging conditions impact on the stock and hence we give an “Expensive” recommendation on the stock at the current price of $6.52

.PNG)

BLD Daily Chart (Source: Thomson Reuters)

CSR Limited

.png)

CSR Details

Strong EBIT Growth: CSR Limited (ASX: CSR) has reported a decent full year performance ended on March 31, 2016. The group’s revenue and net profit after tax increased 14% and 13% respectively. The group segment’s Building Products and Viridian EBIT rallied over 40% and 161% as compared to the same period of last year.

.png)

Aluminum EBIT movement (Source: Company Reports)

Accordingly, CSR rallied over 43.89% in the last six months (as of July 11, 2016). The company has also undertaken $150 million of on-market share buy-back plan. On the other hand, Australian dollar has been strengthening against the US dollar which is expected to impact the group’s performance. Based on the foregoing, we give an “Expensive” recommendation on the stock at the current price of $3.87

CSR Daily Chart (Source: Thomson Reuters)

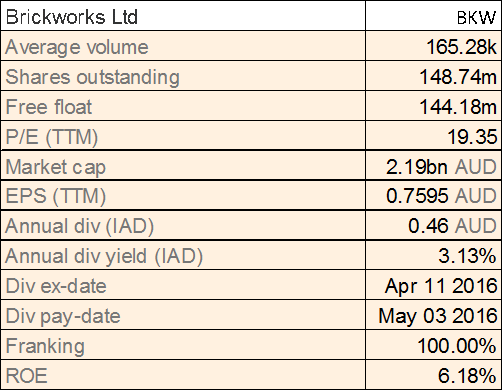

Brickworks Limited

BKW Details

New pre-commitments secured: Brickworks Limited (ASX: BKW) secured new pre-commitments within the JV Property Trust at Oakdale Central in which the multinational consumer goods company has committed to 36,870 m

2 warehouse and office facility on a ten-year lease term and DSV Air & Sea has committed to 8,275 m

2 warehouse and office facility on a five-year lease term. Moreover, the Property Trust will also develop a speculative 6,400 m

2 warehouse and office facility at Oakdale Central, with completion expected in early 2017. Meanwhile, at Oakdale South, the progress has been made on the sale of 27.9 hectares of land including agreements to sell 6.4 hectares to Toyota Motor Corporation Australia and 7.0 hectares to Sigma Pharmaceuticals, subject to DA approval and conditions. The sale of the total 27.9 hectares is expected to generate cash proceeds for the Property Trust of about $90 million late in 2017. In addition to these sales, work at Oakdale South would focus on developing the remaining 43 hectares of land to meet the pre-commitment market.

Overall the EBIT from the Property Group in 2016 is forecast to be slightly higher than the prior year. On the other hand, BKW stock has fallen 4.71% in the last three months (as of July 12, 2016), due to weak investor’s sentiments on the stock given the volatile market conditions. We still believe that the stock is “Expensive” at the current price of $14.94

BKW Daily Chart (Source: Thomson Reuters)

GWA Group Ltd

.png)

GWA Details

Dispute settlement: GWA Group Ltd (ASX: GWA) had appointed Mr. Tim Salt as the Chief Executive Officer of the Group at the start of the calendar year. Meanwhile, GWA has resolved the dispute with Carrier Air Conditioning with an immediate net payment of $2.8 million to GWA.

This payment will be treated as a part of discontinued operations in GWA’s FY16 accounts. The dispute arose from the liabilities of the Carrier companies to GWA for losses with regard to Brivis business acquired by GWA in March 2010. GWA stock has fallen over 7.62% (as of July 12, 2016) in the last three months and we believe the negative momentum in the stock would continue in the coming months. Hence, we give an “Expensive” recommendation on the stock at the current price of $2.10

GWA Daily Chart (Source: Thomson Reuters)

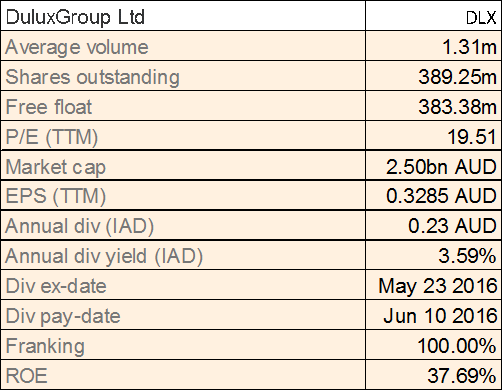

DuluxGroup Ltd

DLX Details

Moderate result but tough market conditions: DuluxGroup Ltd (ASX: DLX) recently announced the appointment of Graeme Liebelt as the non-executive director effective June 14, 2016. The group reported revenue growth of 1.7% to $851.1 million while underlying profit grew 3.7% to $63.7 million for the six months to March 31, 2016. DLX’s cash flows were low at the back of higher inventory and tax costs.

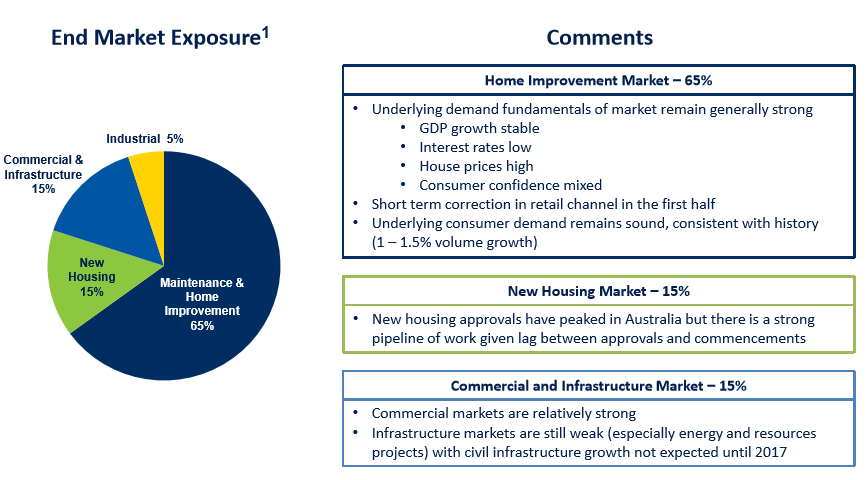

Market Exposure (Source: Company Reports)

The stock is trading close to its 52-week high price. Given the mature market and level of competition, we believe it to be “Expensive” at the current price of $6.49

DLX Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

AU

AU

Please wait processing your request...

Please wait processing your request...