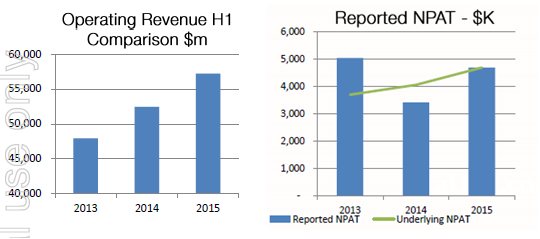

Sealink Travel Group Ltd (ASX: SLK) reported a strong first half of 2015 performance, with the revenues surging 9.1% yoy to $57.2 million. The growth was mainly contributed by the full year impact of Darwin as well as Captain Cook cruise contract with Harbour City Ferries (HCF). Moreover, the increase in its core kangaroo island business had also drove the revenues.

Operating expenses rose $2.9 million to $50.5 million in the first half of 2015, impacted by the Darwin and HCF full year trading and variable costs. EBITDA increased 13% to $9.3 million during the period, from $8.2 million in 1H14. Accordingly, the net profit after tax surged 37% yoy to $4.7 million, while the NPAT, excluding ASX listing costs in 2014, increased 15% on a year over year basis. Meanwhile, the group reported a fully franked interim dividend of 3.8 cents per share, resulting a payout ratio of 62%. Sealink Travel incurred $3.7 million of capital expenditure during the period. One new vessel was added to the captain cool cruises, and the group intends to buy more two ferries. The Twin island contract was prolonged for four years.

First half of 2015 financial performance (Source: Company Reports)

With regards to the group’s Kangaroo island highlights, revenues rose 6% yoy to $26.5 million, driven by the rising tourism traffic flow to Kangaroo Island. The group’s packaging area (that is into selling accommodation and other travel products like coach tours and air travel) rose 19% on a year over year basis, driven by its social media strategy. Captain cook cruises improved by $2 million to $22.2 million during the first half, on the back of better tourist numbers and contracted services. Sealink extended its hop on hop off service to Manly stop in December 2014. The group also acquired a two 300 passenger high speed vessels for $6 million in Sydney and these vessels operations have started since April. The Queensland and Northern territory surged 14% yoy to $8.1 million in the first half of 2015, on the back of contribution from improved ferry passenger services to Mandorah and Tiwi islands. At Sealink Queensland, MV Reef cat underwent a major upgrade for the vessels to palm island route services to continue for the next five years.

As per the balance sheet highlights, Sealink Travel acquired over $3.7 million of fixed assets during the first half of 2014-15. The group was able to improve its net interest bearing debt by $4.3 million to $4.8 million in 1H15, from $9.1 million in the period ending June 2014. Sealink Travel raised $3.7 million of capital through exercise of options. Cash and cash equivalents rose to $6.2 million in the first half of 2015, from $3.4 million as of the half year ended on December 2013. The gearing ratio improved to 13% for the period ending on December 2014, as compared to 17% as of June 2014.

Outlook

Sealink Travel Group delivered strong returns since its IPO on October 2013, posting a returns of 49.3% till date (as of July 23rd). The strong first half of 2015 performance drove the stock to touch its all-time high of $2.66 from $2 during the starting of the year. Meanwhile the stock has been correcting post its high levels, and witnessed a decrease of over 12% in the last three months.

Sealink Daily Chart (Source - Thomson Reuters)

The company is a major ferry services provider to the popular tourist destinations, especially in its core business of Kangaroo island route and offers services to the island for the local people as well. Although the firm faces competition for its Captain Cook Cruises in Sydney, Sealink Travel Group is making efforts to upgrade the cruises by adding new routes and facilities. Moreover, the Queensland and Northern territory posted solid growth during the first half of 2015, and is well positioned to further benefit from the ferry passenger services to Mandorah and Tiwi islands.

The lower Australian dollar is also expected to drive tourism in Australia and thus improve the group’s New South Wales and South Australian Business. The decreasing fuel prices coupled with the fuel hedging contract expiries (which would expire shortly) would further support the company’s profitability. The shares of Sealink Travel Group rose over 4.3% in the last four weeks, and we estimate the rally to continue in the coming months. We believe that the group is well positioned to deliver strong second half of 2015 results as well, on par with its first half highlights,

Based on the foregoing, we give a “BUY” recommendation to the stock at the current levels of $2.23

AU

AU

Please wait processing your request...

Please wait processing your request...